ASX 200 tries and fails at 5500 to close only modestly higher at 5476 up 10 points. Materials and energy the stars, with banks stable despite government reforms. Asian markets continued mixed with Japan bouncing back 1.04% though China slipped 0.03%. AUD 76.04c and US futures up 17.

STOCKS AND SECTORS

- Banks shrugged off moves by the Turnbull government to make them more accountable with the big four basket slipping a little to $157. National Bank (NAB) +0.23% was the best of the bunch. Insurers recovered after yesterday, taking their cue from Suncorp (SUN) +0.68% results. QBE Insurance (QBE) +1.12% and AMP +1.56% the standouts.

- Big miners were mixed with BHP +1.15% enjoying an oil kick whilst RIO -1.62% gave a little away after the results. Fortescue Metals (FMG) -2.05% fresh from their win at Kalgoorlie for Digger of the Year slid a little.

- Energy stocks resilient in the downturn exploded out of the blocks with Santos (STO) +6.74%, Beach Energy (BPT) +4.76% and Worley Parsons (WOR) +4.05%.

- Gold stocks took a break as Diggers and Dealers wound up with sore heads all round. Beadell Resources (BDR) -5.77%, Perseus (PRU) -3.91% and Gold Road (GOR) -3.6%. Metals Ex (MLX) +1.76% bucked the trend after announced a gold demerger and a capital raising for $100m although well off its highs.

- Mining services were buoyed by the Downer (DOW) +7.69% numbers, Decmil (DCG) +13.22% and Monadelphous (MND) +4.3%. Seven Group (SVW) +1.39% and Reece Limited (REH) +6.24% joined the fun too.

- A takeover bid in the vitamin sector was enough to help Bellamy’s (BAL) +7.88% rally hard. A2Milk (A2M) +2.95% also firmed as did Capilano Honey (CZZ) +3.24%.

- Healthcare stock a little weaker led by CSL -1.76%, Regis Healthcare (REG) -0.79% and Japara (JHC) -2.31%

- Speculative stock of the day: Emeco Holdings (EHL) +86.84% after reporting the company’s fourth quarter results. EBITDA of $54.2m up from $11m and within guidance of $53-57m. Looks promising and may get broker upgrades.

CORPORATE NEWS

- Vitaco (VIT) +19.89% has been bid for by two Chinese giants in a $314 million agreed takeover. The company which listed September 2015 after raising $232 million in a public float, will be acquired by Chinese firm Shanghai Pharmaceuticals and Chinese private equity group Primavera.

- Suncorp Group (SUN) +0.68% has reported an 8% drop in annual profit. For the full year ended June 30, 2016 Suncorp Group showed an 8.3% decline in group net profit after tax to $1.04 bn from $1.13 bn in the previous financial year.

- Downer EDI (DOW) +7.69% posted an annual net profit falling 14% to $180.6m. Net profit was in line with expectation with EBIT down 10.6%. A final dividend of 12c was announced unchanged from a year earlier. The company faces ‘continued pressure’ in its resource based business but the worse could be over.

- Kathmandu (KMD) +3.57% the company has tightened the range of its FY16 earnings guidance to NZ$33-34m, from $32-35m in June, up from $20.4m the previous year.

- Metals Ex (MLX) +1.76% has tapped the market for $100m and has also announced a demerger of its gold business leaving a tin/nickel/copper play and a gold company.

ECONOMIC NEWS

- The government has announced a banking sector reform which will have the CEOs quaking in their boots as they will have to front a government committee once a year.

- Retail spending growth is at its slowest annual pace in three years. Spending rose by just 0.1% in June, figures from the Australian Bureau of Statistics show, below market expectations of growth of 0.3%. That took retail trade growth in the year to June to 2.8% the slowest annual pace of growth since mid-2013.

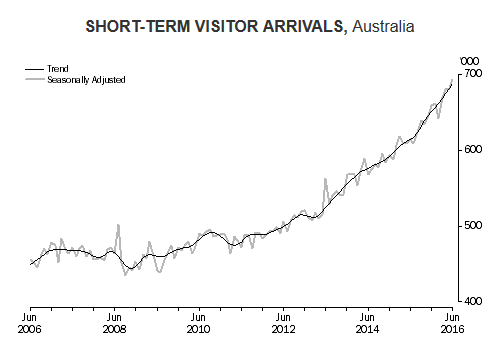

In trend terms, short-term visitor arrivals to Australia during June 2016 increased 0.9% compared with May 2016. Currently, short-term visitor arrivals are 12.0% higher than in June 2015.

ASIAN NEWS

- Noble Group rebounded in Singapore as the company’s new rights shares began trading on the exchange. The shares rallied as much as 12% to 14.8c in the preceding two days, the stock lost 19%.

- Japanese policy maverick, Kozo Yamamoto, recently promoted to the cabinet, has repeated calls for the BOJ to strive for its CPI goal. He also pushed him plan to target specific increases in wages.

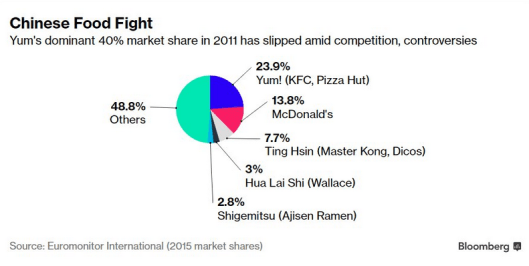

- Seems the Chines are losing interest in KFC and Maccas

EUROPE AND THE US

Markets slightly positive bias waiting for BOE decision

- Bank of England decides. First interest rate since 2009? Most economists predict reduction in key rate to 0.25%.

- Quarterly inflation report too in UK.

- UK business activity suffered its biggest fall ever. The Business Activity Index fell to 47.4 in July, from 52.3 in June, signalling a fall in UK services output.

- Dutch inflation rate falls to -0.3%, its first negative rate in over 30 years.

- Siemens raised its earnings outlook for the year after posting higher-than-expected third-quarter profit and a jump in large orders for power-generating equipment. Profit from industrial operations rose 20% to 2.19 bn euros (US$2.44 bn) in the three months to June.

And finally……………………..apologies in advance!!!

What is the difference between Michael Jackson and a grocery bag? One is white, plastic, and dangerous to children. You put groceries in the other.

sorry..couldn’t resist!!

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com