The ASX 200 rallied another 35 points to 8657 (0.4%) ahead of a US long weekend. Up 27 pts for the week. Banks pushed ahead, led by CBA up 0.9 %, and the Big Bank Basket to $275.57 (0.8%). Insurers slid as yields fell, NWL off 1.0% and GQG falling 2.2% as tech boomed. Industrials were mixed, TLS fell 1.5% as a broker downgraded the stock, REA continued lower, off 4.1%, as did CAR off 2.8%, with tech stocks also continuing to be pressured. XRO down 0.9% and WTC falling 1.4%, with the All-Tech Index up 0.4% Utilities were also weaker, ORG off 1.8% and APA falling 0.3%.

Resources were generally better, BHP rose 1.1% and RIO up another 1.7%, with S32 doing well, up 5.1% and lithium stocks rising, PLS up 2.9% as gold miners found some bargain hunters. NEM up 0.8% and EVN gaining 3.1%. NST continued to suffer, down 0.6%. Oil and gas mixed. In corporate news, uranium stocks were better, PDN up 5.9% and DYL rising on broker upgrades.

In corporate news, ARU entered a trading halt to raise another $350m at 26c. GYG jumped 9.6% as it announced plans to close the US business. APX jumped 9.4% on a trading update. TUA steady as the M1 deal was pronounced DOA. MYX won a small settlement against Cosette for the failed bid.

In economic news, the Japanese CPI came in below expectations.

Asian markets were better, with Japan up 2.6%, Hong Kong up 1.1%, China up 1.2%, and the Kospi up modestly. US futures were better, with the Dow up 155 and the Nasdaq up 150. European futures are opening around 0.5% lower. Oil up 2.0%. The US and UK are closed Monday.

HIGHLIGHTS

- Winners: SRL, ELV, EOS, 4DX, GYG, MLX, WBT

- Losers: SEK, TLX, LLC, CAT, CMW, REA, IAG

- Positive Sectors: Banks. Lithium. Iron ore. Gold. Uranium.

- Negative Sectors: Tech. ‘Old Skool’ platforms. REITs. Insurers.

- ASX 200 Hi 8675 Lo 8644 – Up 27 pts for the week.

- Big Bank Basket: Rallies to $275.57 (+0.8%)

- All-Tech Index: up 0.4%

- Gold: Steady at $6340

- Brent Crude up 2.0%

- Bitcoin: Steady at US$77592

- 10-year yields: Drops to 4.92%

- AUD: Better at 71.45c.

MARKET MOVERS

- GYG +9.6% closes US operations.

- EOS +10.7% nice bounce.

- 4DX +10.4% good to see.

- WBT +7.7% do you want chips with that?

- SRL +15.1% initial director’s interest.

- ELV +12.4% ceasing to be a substantial holder.

- EQR +2.1% bounces back.

- APX +9.4% trading update.

- NVX +11.1% looks ok.

- LOT +10.7% new COO

- LLC -5.7% downgraded.

- CAT -5.1% end of week profit taking.

- CXO -3.3% slips again.

- SEK -5.9% heads lower.

- ARR -13.3% Cleansing

- ONE -8.1% director’s interest.

- Yesterday’s Hero: ADO +5.9%

- Speculative Stock of the Day: IMU +32% Azer-cel data from CAR-T naïve cohort.

ECONOMIC AND OTHER NEWS

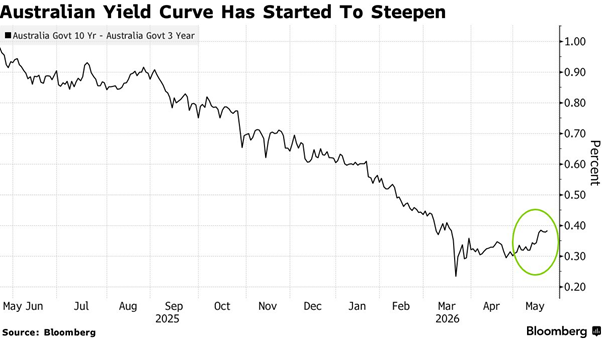

- The local yield curve is steepening as traders bet the RBA has done its dash.

- The swaps markets continue to price in one additional quarter-point increase by year-end, underscoring lingering inflation concerns.

- Japan’s core inflation eased more than expected in April to its lowest level since March 2022, potentially weakening the case for an early rate hike by the Bank of Japan.

- Headline inflation was at 1.4%, down from March’s 1.5% and the fourth straight month below the central bank’s 2% target.

- Kevin Warsh to be sworn in today as head of the Federal Reserve.

- US set to deploy 5000 troops to Poland. Make up your mind!

- SoftBank Group extends scorching rally with shares in OpenAI, Arm-backer surging over 11%.

- Lenovo shares were on track to close at their highest on Friday after the company reported strong growth in AI-related earnings that offset difficulties from rising component prices.

- SpaceX fails to launch latest rocket.

- Rubio sees ‘good signs’ US could reach deal with Iran.

- JPMorgan looks to offload exposure to $4bn in private equity-linked loans.

- DNC autopsy says Biden White House to blame for Harris loss.

- UK and US markets closed Monday.

And finally…..

Clarence

XXXXX