ASX 200 stops short of 5500 with a 22-point rise to 5497 as caution creeps in pre NFP tonight. Materials and energy stocks the standouts as banks steady. Asian market again mixed with Japan up China down. AUD firmer again after SOMP at 76.54 and US futures up 25 points.

STOCKS AND SECTORS

- Materials stocks stood out today as Dalian iron ore futures rose in China, BHP +3.73%, RIO +1.85% and Fortescue Metals (FMG) +5.56%.

- Energy stocks kept pace with the crude rises led by Origin Energy (ORG) +3.11% and Senex (SXY) +3.92%

- Base metal stocks also very solid today with Independence Group (IGO) +4.35%, CI Resources (CII) +1.52% and Orocobre (ORE) +4.24%.

- Mining services have continued their stellar run gaining confidence after upgrades on Downer EDI (DOW) +6.03%, Seven Group (SVW) +4.95%, GR Engineering (GNG) +6.3% and RCR Tomlinson (RCR) +7.11%.

- Banks once again posted modest gains as we wait for results next week. Commonwealth Bank (CBA) +0.65% the best performer. Insurers positive though with QBE Holdings (QBE) +1.84% and Suncorp (SUN) +1.43% drawing fans after he numbers yesterday.

- Food and health stocks also doing well today with Costa Group (CGC) +2.84%, Blackmores (BKL) +2.54% and one of our favourites BWX +1.84% all doing well. Murray Goulburn (MGC) -1.7% bucked the trend. Telcos eased as the ACCC has launched an inquiry into a broad range of telco issues from streaming to NBN Telstra (TLS) -0.7%

- Speculative stock of the day: Gulf Manganese Corp (GMC) +150.00% after securing a US$10m cornerstone investment to fast track its Kupang Smelting hub project in Indonesia. $10m gets 10% with an option for another $7m for a further 5% equity stake.

CORPORATE NEWS

- Virgin Australia (VAH) +2.08% has posted a full year net loss of $224.7m, after taking charges related to fleet simplification and other efficiency activities. Underlying profit before tax rose to $41m, an improvement on the previous year’s $49 million loss. Importantly the outlook was positive with momentum to continue and it reaffirmed it was on track for FY17 targets.

- Capilano Honey (CZZ) -4.87% after reporting (briefly) its results showing a 20.9% rise in net profit to $9.483 in the middle of expectations. Not a huge amount of commentary from eth company though in an exercise in minimalistic investor relations.

- SG Fleet (SGF) +6.59% Has acquired Fleet Hire Holdings based in the UK. The purchase price was £19.6m, with an anticipated 4.5% EPS accreditation in the first full year of ownership expected. It will be funded by ₤12.0m in debt facility, ₤5.8m in cash and ₤1.8m in equity to vendors.

- Beston Global Foods (BFC) -15.96% disappointing guidance below prospectus forecasts. FY16 dividend will be 0.35-0.65cps, lower than the target range of 1.5c -2c.

ECONOMIC NEWS

The RBA released its Statement of Monetary Policy today (SOMP).

- The bank left its forecasts of growth and inflation unchanged from May.

- Australian GDP growth was better than expected in March due to weather conditions.

- Growth expected to be between 2.5% and 3.5%.

- Slow wage growth and competition in the retail markets, and is expected to “persist for some time”.

- The bank reiterated its warning about over-supply of apartments in parts of inner-city Melbourne and Brisbane.

The statement was broadly neutral with regard to future rate moves.

ASIAN NEWS

In Japan total wages rose by 1.3% year on year in June, one of the highest growth rate so far in the year boosted by summer bonuses up 3.3%.

- Flooding in China last month caused about US$33 billion in economic losses, with less than 2% of the sum covered by insurers. Storms and flash flooding in the U.S. resulted in at least US$1.5 billion of losses, two-thirds of which were insured.

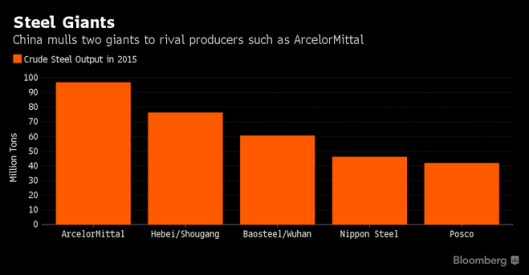

- In a sign of how much damage the soaring yen has done to Japanese exporters, Nippon Steel & Sumitomo has been overtaken as the world’s most valuable producer by Europe’s ArcelorMittal and is neck and neck with a revitalised Posco in South Korea for second place.

If China merges its major producers in the north and south they slip even further down the list.

EUROPE AND THE US

- Royal Bank of Scotland results in London showed a GBP 1bn loss.

- UK hiring levels plunge post-Brexit at their fastest rate in 7 years.

- Allianz Europe’s biggest insurer, said second-quarter profit fell on higher claims from natural disasters. Net income declined to 1.1 billion euros (US$1.2 billion) from 2.02 billion euros a year earlier. Forecast was for 1.55bn euros.

Following the Bank of England rate cut last night governor Mark Carney will NOT be heading down the negative rate path unlike some of his peers.

- Carney is now firmly in league with Yellen in saying the policy’s not for them.

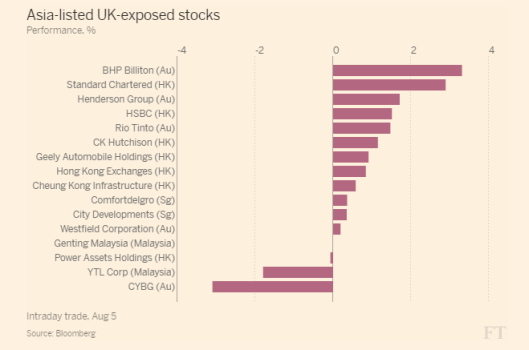

Some of the UK exposed stocks listed in Asia

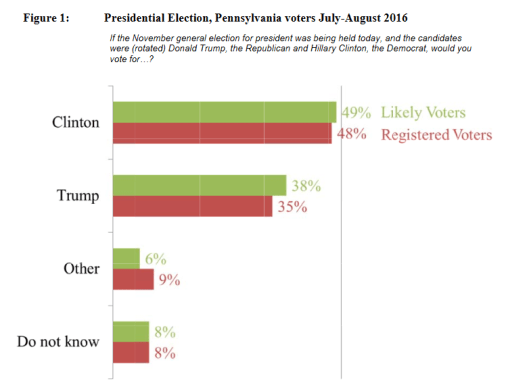

Trump has had a bad week with this poll in Pennsylvania (a crucial battleground)

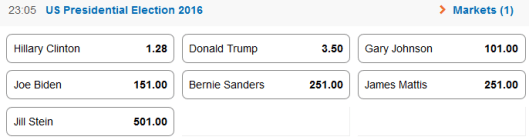

Latest odds

And finally………….

Little Johnny comes running into the house and asks, “Mommy, can little girls have babies?” “No,” says his mom, “of course not.” Little Johnny runs back outside yelling to his friends, “It’s okay, we can play that game again!”

Ok its Friday so maybe just one more..

Little Johnny’s father asks him if he knows about the birds and the bees. “I don’t want to know!” Little Johnny says, bursting into tears. Confused, his father asks what’s wrong. “Oh, Dad,” Little Johnny sobs, “first, there was no Santa Claus, then no Easter Bunny, and finally, no Tooth Fairy. If you’re about to tell me that grownups don’t really have sex, I’ve got nothing left to believe in.”

Have a great weekend!

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com