Headlines today…

- ASX 200 falls 55 points to 5674 as buyers sidelined.

- Volume remains low as 5700 level gives way. Closes near low of 5665.

- Iron ore miners hold the line, just.

- Gold miners mixed on bullion rise.

- Banks suffer big losses on APRA concerns.

- Confession season. Upgrades for two retailers APE and ADH.

- Telcos slip. Healthcare sold off CSL leads.

- Bond proxy stocks drop. REITs and infrastructure in focus.

- AUD firmer at 76.50c.

- Yellen kicks off testimony tonight as her future looks uncertain.

- US Futures up 3.

- Asian markets mixed with China CSI 300 up 0.11% and Japan down 0.54%.

STOCK STUFF

- GXY -3.76% on profit taking.

- CSL –2.54% broker downgrades following patent law suit.

- MQA -3.33% infrastructure selling.

- HVN +1.79% shorts covering.

- PTM -2.69% broker downgrade and profit taking.

- QAN -2.90% as oil rises.

- MTS -2.83% second thoughts on new ex Tesco CEO.

- GNC -3.17% wheat forecasts down.

- RSG ++2.71% on good production and costs.

- SYR -2.73% profit taking.

- RWH +37.69% takeover by US group.

- BIG +13.68% positive quarterly update.

- NEA +3.15% positive announcement yesterday

- Quarterly production ahead. WHC Friday. RIO, BHP, STO, WPL next week.

- Biggest risers – APE, RSG, CDD, NCM, SRV, VRL and AHG.

- Biggest fallers – GXY, PLS,MYX, MQA, GXY and GNC.

TODAY

- Adairs (ADH) +34.21% Trading update with a strong second quarter. Total sales up 8.3% to $140.4m and FY 17 full year sales expected to be $264.9m. Underlying EBT between $18.5m and $19m. Positive outlook statement. ADH had a significant profit downgrade in November last year and has struggled to regain market confidence ever since.

- Lynas (LYC) -unchanged- The company recorded a record cash flow of $15.8m up from $11.6m It also noted improved market conditions which is in line with the comments from GGG a week or so ago. Strong demand for magnetic metals in China. LYC is the leading NdPr producer in the world.

- BT Investment (BTT) -2.28% FUM grew by $3.2bn to $46.1bn. Good performance fee increase from $3.5m to $9.4m.

- Downer EDI (DOW) -0.32% Has extended the Spotless (SPO) offer as management at SPO suggests to remaining investors to reject the offer.

- Wattle Health (WHA) +22.11% after the infant formula supplier acquired a stake in Australian infant formula maker Blend & Pack, which Wattle Health says will help secure its business in China.

- AP Eagers (APE) +5.07% expects to report a record first-half profit of $68.1m, up from $67.9m in the first-half of FY 2016. This follows a very positive May and June in the run up to the end of financial year in new vehicle sales.

- Resolute (RSG) +2.71% reported a production ahead of estimates of 330koz at a AISC of $1130 below previous forecasts of $1280. Gold production now expected to be around 300koz in FY18. The company has cash and bullion of $290m.

- Kidman Resources (KDR) -11.97% Chilean lithium miner SQM will pay $US110m for a 50 % joint venture interest in the Mt Holland lithium project in Western Australia.

ECONOMIC NEWS

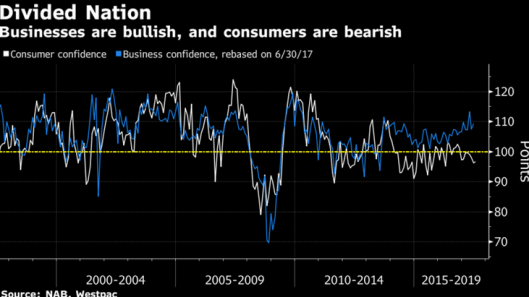

- Westpac Consumer sentiment has risen 0.4% to 96.6 in July compared with last months’ reading of 96.2.

- Pessimists still outweigh optimists and it will be still sometime before the figure jumps about 100 again, bucking the 8-month long trend.

- Consumers are bearish probably as wages stagnate and energy prices rise. Business, though remains bullish on the outlook. Households are being squeezed by high debt and weak wage growth, consumption supported by drawing on savings and home equity, resulting in a halving of the savings ratio since 2013 to 4.7%.

- Dwelling starts decreased 11.4% for the Quarter with Private sector apartments hard hit decreasing 15.3%. Dwelling approvals remain at near record highs of 40,186 dwellings.

ASIAN NEWS

- Apple will establish its first data centre in China to speed up services such as iCloud for local users and abide by laws that require global companies to store information within the country. The new facility will be solely powered by renewable energy.

- Unemployment in South Korea rose more than expected in June and to the second-highest level for the year to date, despite growth in the country’s manufacturing sector.

EUROPE AND US MORNING Headlines

- Spare a thought for the holders of cryptocurrencies. Bitcoin, Ethereum and Ripple (never even heard of this one) are down more than 20% from their highs. Digital coins are currently worth around US$80 billion, down from a market capitalization of US$100 billion last Friday.

- Canada may be the first developed country to raise rates this evening.

- Trump Jnr faces media. Reveals ‘I love it’ on Clinton email exchange with Russians.

- Reports that Yellen is on the way out in favour of Goldman alumni Gary Cohn. Twitter has a new CFO. Ex Goldman man Ned Segal. So that’s the Fed and Twitter Perfect.

- In the UK Debit, credit and charge cards were used for 10.3bn transactions in 2016, a rise of 5% on 2015 that gave plastic a 54% share of all retail payments by volume, according to the latest figures from the British Retail Consortium (BRC). Cashless payment providers in vogue with Worldpay takeover by US rival last week.

And finally…

Phone rings, woman answers. The pervert, with heavy breathing, says,

“I bet you have a tight ass with no hair? Woman replies, “Yes I do, he’s watching golf – Who shall I say is calling?”

After the honeymoon, the new wife told her husband, “I think it’s time for you to stop playing golf. In fact, you might as well sell all of your clubs.”

The husband replied, “You’re starting to sound like my ex-wife.”

His wife looked at him crossly and said, “I thought you said you’ve never been married before?”

The husband responded simply, “I haven’t.”

Clarence

XXXX