Today’s highlights…

- ASX 200 up 20 to 5724 as buying eases.

- Volume remains low with a high of 5747.5.

- Banks and industrials lead. Retailers stir.

- Resources ease on oil price.

- ACCC appeals TAH/TTS decision.

- SOL/BKW win court case against cross shareholdings.

- AUD 76.06c

- US Futures up 19.US reporting season kicks off this week.

- Yellen testifies in Congress Wednesday.

- Asian markets mixed with China CSI300 down 0.02% and Japan up 0.84%.

STOCK STUFF

- QBE +2.76% higher bond prices helping recovery.

- SGM +4.60% US news on steel imports helping.

- FLT +3.24% rally continues on profit upgrade.

- APT -5.79% completion of the recent merger.

- SYR +2.46%Tanzanian issues highlight Mozambique and SYR prospects.

- GXY +2.38% lithium buzz continues.

- RIO +0.09% Mongolian concerns as new resource nationalist elected president.

- JHC-2.39% EHE -2.23% on concerns for the sector.

- SGH requests trading halt over mediation outcome.

- Biggest Risers – SGM, TGR, SYR, MQA, JHG and JBH

- Biggest fallers – APT, MSB, PLS, MTR, NCK, and HSN

TODAY

- South32 (S32) –3.20% The company announced operations are still suspended and will be for some time at its Appin Colliery site, part of the Metallurgical Coal operation, pending a safety and operating practice review.

- Neometals (NMT) –unchanged- The sale period for the company’s equity stake in the Mt Marion project has closed after receiving no bids. However, the company has said over the period, the project has reached significant milestones increasing the projects value.

- CIMIC Investment Group (CIM) +0.76% A Middle-Eastern company which CIM has a 45% stake in has gained a construction contract for a Dubai project that will bring in revenues of $224m. The company will build five 16-storey towers due to be completed in June 2019.

- Ardent Leisure Group (AAD) +1.47% The monthly theme parks trading update showed visitation was down 30.5% and revenue down 35.3% mom. Revenues were $4.4m however both visitation and the revenue both improved in comparison to the May number.

- CSL (CSL) –0.63% In the US, the company Bioerativ has filed a complaint with the courts that a product of CSL infringes on 3 intellectual property patents. CSL say that the intellectual property is theirs and they will strongly defend the allegations.

- Kidman Resources (KDR) –14.52% The company has won court dispute over the rights to the lithium in the Earl Grey deposit at the Mt Holland project.

- Soul Pattinson (SOL) -0.06% The investment company has had a big win in court against Perpetual. The court found that the cross shareholding in BKW +0.75% was in the best interests of the company. Perpetual will have to pay costs and this will also remove the unnecessary distraction of the move to unwind the cross shareholdings.

- Programmed (PRG) –3.06% The company as entered a 50/50 joint venture for marine services with Atlas Professionals, both being staffing services companies to operate in Australia and New Zealand. Programmed has sold atlas all of its international business and half of its Australia and New Zealand business for $29m.

BOND MARKET UPDATE

- Commonwealth Bank (CBA) has broken new ground with last weeks 30-year US dollar bond. The $US1.5 billion 3.90% 144A/Reg S note, priced at 103bps over Treasuries. The spread is believed to be the tightest for any 30-year bank bond in dollars, and the coupon the lowest in the US market at that maturity. The sale attracted an order book of $US3.4bn

ECONOMIC NEWS

- Westpac (WBC) has withdrawn some of its mortgage and equity-release products in a high-level review of its product range and underwriting standards. The top-down review is expected to reassess dozens of loans and lending packages.

ASIAN NEWS

- Sunac China agreed to buy hotels and projects from Dalian Wanda for 63.2 billion yuan (US$9.3 billion), in one of China’s largest property transactions.

- Japan current account fell11 JPY trillion yoy to 1.65 JPY trillion surplus. This was below expectations which predicted a rise to 1.8 JPY trillion. Exports fell 11.7 and the goods moved into a 0.12 JPY trillion deficit compared to a 0.03 JPY trillion surplus in May 2016.

- Japan core machinery orders fell 3.6% mom versus an expected 1.7% rise for May. This is the second straight month of declines, having a 3.1% fall the previous month.

- China producer prices rose 5.5% yoy, the same as last month and expectations. This is the tenth straight month of increases however since the 7.8% peak in February 2017, the trend has been down.

- China’s inflation rate remained at 1.5% meeting expectations. This is the highest since January.

EUROPE AND US MORNING HEADLINES

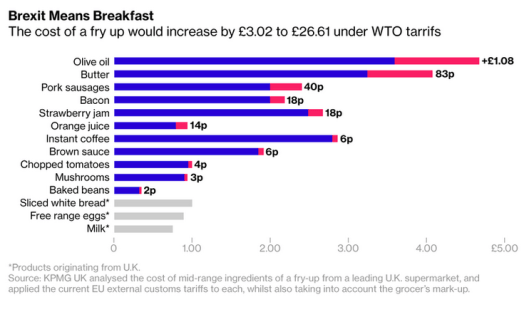

- What Brexit means for Breakfast. KPMG has analysed the great British fry up and found it will cost more than GBP3 more under WTO tariff rules. Up 13% mainly on the back of Spanish Olive Oil, orange juice and French butter.

And finally……………

Trumpy no mates!!

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com