ASX 200 rallies 44 points to 5771. Miners and industrials shine with banks trying hard to register gains as ratings agency move on property concerns. Asian markets mixed with China down 0.06% and Japan up 0.34%. AUD 74.45c and US Futures up 31.

STOCKS AND SECTORS

- Miners once again saw good gains led by BHP +1,44% and RIO +3.08%. Fortescue Metals (FMG) +2.48% rose enough to nearly pay for Twiggy’s huge philanthropic donation today of $400m. Hats off to you Twiggy. Base metal stock had a great day too, as Western Areas (WSA) +6.64%, Oz Minerals (OZL) +0.71% and Metals X (MLX) +6.29%. The gold sector was modestly higher with Newcrest (NCM) +2.11%, Resolute Mining (RSG) +3.80% and Dacian Gold (DCN) +5.03%.

- Energy shares jumped ahead of the OPEC meeting this week. Origin Energy (ORG) +3.95%, Caltex (CTX) +1.34% and Woodside (WPL) +1.89%.

- Banks and financials mostly firmer as the Big Bank Basket rose to $171.15. Spoiling the party for the small banks were S&P which downgraded smaller institutions on fears of potential housing slowdown. ANZ Bank (ANZ) -0.39% the only one of the big four to suffer today. Investors still feel nervous on the sector though wealth managers Henderson Group (HGG) 1.72+% and Challenger (CGF) +1.02% did well. REITs also had a good day with Scentre Group (SCG) +1.44%, Westfield Corp (WFD) +1.33% and GPT+1.37% the stand outs.

- In the industrials, we saw across the board gains with the exception of healthcare weighed down a little by CSL -0.60%. Infrastructure stocks Transurban (TCL) +1.26%, Macquarie Atlas Roads (MQA) +1.59% and Sydney Airport (SYD) unchanged. Retailers though once again unloved with Harvey Norman (HVN) -1.57%, Super Retail (SUL) -2.31% and Motorcycle Holdings (MTO) -4.00%. Media stocks under some pressure as APN Outdoor (APO) -5.79% fell into a hole following the merger with Ooh!Media (OML) +2.27% being abandoned last week.

- In consumer stocks both Woolworths (WOW) +0.19% and Wesfarmers (WES) -0.51% struggled as Moody’s predicted Aldi will continue to erode market share. The dairy and formula sector did well though with Bega Cheese (BGA) +%, Bellamy’s Australia (BAL) +4.18% and Webster (WBA) +8.59% building on harvest information. One that has done spectacularly badly is Murray River Organics (MRG) -41.94% after yet another profit downgraded and now at the mercy of its bankers.

- Telcos also in the sunshine with Telstra (TLS) +1.35%, Vocus Group (VOC) +4.62% trying hard to string some gains together and TPG Telecom (TPM) +0.67%. IT bounced hard too, Wisetech (WTC) +2.73%, Altium (ALU) +3.90%, Xero (XRO) +1.75% and Computershare (CPU) +1.31%.

- Speculative stock of the day: Western Mining (WMN) +16.67% on big volume following the general meeting.

CORPORATE NEWS

- Fisher and Paykel (FPH) -0.42% reported a net profit of NZ$1169.2m up 18%. An increase of 17% on the dividend too. The company has launched a new CPAP machine, SleepStyle. The outlook for FY18 is for NPAT of between NZ$180-NZ$190m.

- Surfstitch (SRF) -23.47% has announced the closure of the North American operations and the UK business is continuing to suffer from intense margin and sales pressure. The company is now forecasting an underlying loss in the $10.5m-$11m region.

- Alumina (AWC) +3.26% announced Mike Ferraro will succeed Peter Waslow as CEO.

- Westpac Bank (WBC) +0.78% have written to shareholders outlining the implications of the proposed tax(levy)on the banks. Whilst the bank is still waiting for more details, the changes will cost it $260m after tax or 8cps. The bank is urging the government to bring in a sunset clause to coincide with the budget returning to surplus and also the levy to extend to foreign banks.

- Suncorp (SUN) +0.64% has updated the market on the bank’s asset position. The bank lifted third quarter lending by 2.8% to $44.3bn and is optimistic it can benefit from APRA’s limit on interest only lending. It also said there was limited impact from Cyclone Debbie and it supported the new bank levy. Mainly as it does not apply to them.

- Downer EDI (DOW) +0.32% has extended its takeover offer for Spotless Group (SPO) unchanged to June 14.

- Village Roadshow (VRL) +3.12% in talks to offload its 50% stake in its Singapore cinema business to cut debt. It warned in April that numbers for its Theme Parks had fallen 9.4% for the first nine months due to the Dreamworld tragedy at Ardent Leisure (AAD) -0.49%.

- S&P Global Ratings downgraded the credit scores of more than 20 smaller financial institutions on fears of a property slowdown including Bank of Queensland (BOQ) -0.43%, Bendigo & Adelaide Bank (BEN) -1.66% and AMP Bank (AMP) +0.79%. The big four were not affected as they are deemed to be ‘backed’ by the government.

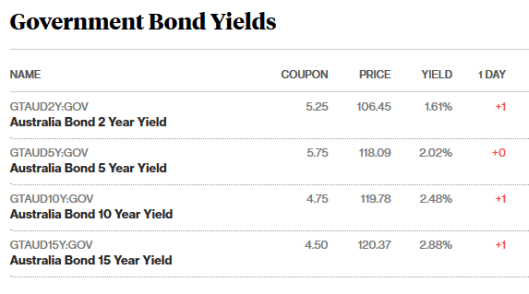

BOND CORNER

ASIAN NEWS

- Japanese exports rose 7.5% from a year earlier (estimate +8.0%), according to data today. Imports jumped 15.1% (estimate +14.8%).

- The trade surplus was 481.7 billion yen (US$4.3 billion) (estimate 520.7 billion yen).

- Chinese steel futures have jumped nearly 6% to their highest since March, stretching last week’s gains on concerns over limited supply. The most-traded iron ore on the Dalian Commodity Exchange rose as far as 501 yuan a tonne, its highest since May 4, and was last up 4.4% at 495 yuan.

- Adani is deferring its final decision on the Carmichael Mine until the Queensland government clarifies the proposed royalty holiday and rates.

EUROPE AND US

- The CEO of Ford is leaving and will be replaced by James P Hackett who was head of its Smart Mobility division. Since taking over in July 2014, as CEO, Mark Fields has seen a 30% share price drop.

- Huntsman and Clariant have agreed to a US$20bn all stock merger to create a global chemical company. Together Huntsman, which is based in Texas, and its Swiss-based rival would operate in more than 100 countries and employ about 32,000 people. American paint and coatings maker PPG Industries is currently in a battle to acquire Dutch rival Akzo Nobel NV for US$27 billion in cash and stock.

- The majority of Apple Pay tills in the UK can now accept mobile payments above £30. Apple Pay transactions in the UK have grown by 300% in the last year, with 23 banks now supporting the service.

- EU ministers meet in Brussels today to discuss their Brexit negotiating position after the U.K. threatened to quit talks on its departure unless the bloc drops its demands for a divorce payment as high as EUR100bn. A study by the Institute of Chartered Accountants in the UK put the cost at as low as GBP5bn. Negotiations begin June 19th after the UK election.

And finally

There were 3 good arguments that Jesus was Black:

1. He called everyone brother

2. He liked Gospel

3. He didn’t get a fair trial

But then there were 3 equally good arguments that Jesus was Jewish:

1. He went into His Father’s business

2. He lived at home until he was 33

3. He was sure his Mother was a virgin and his Mother was sure He was God

But then there were 3 equally good arguments that Jesus was Italian:

1. He talked with His hands

2. He had wine with His meals

3. He used olive oil

But then there were 3 equally good arguments that Jesus was a Californian :

1. He never cut His hair

2. He walked around barefoot all the time

3. He started a new religion

But then there were 3 equally good arguments that Jesus was an American Indian:

1. He was at peace with nature

2. He ate a lot of fish

3. He talked about the Great Spirit

But then there were 3 equally good arguments that Jesus was Irish:

1. He never got married.

2. He was always telling stories.

3. He loved green pastures.

But the most compelling evidence of all – 3 proofs that Jesus was a woman:

1. He fed a crowd at a moment’s notice when there was virtually no food

2. He kept trying to get a message across to a bunch of men who just didn’t get it

3. And even when He was dead, He had to get up because there was still work to do.

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com