ASX 200 closed up 16 at 5353 as the rally ran out of puff and we gave back the majority of the gains at the close. Materials, the standouts as banks pulled back from days’ highs. Asian markets pushed higher again led by hopes of more Japanese stimulus. The Nikkei up 2.7% and China up 0.46%. AUD higher at 75.87 and the US futures market up 9.

The market once again leapt out of the gate following records on the S&P last night and the new PM in the UK steadying the nerves and vowing a good Brexit. However, enthusiasm waned as we approached 5400, towards the top of the range, as the ongoing reality of a workable Brexit exit is far more difficulty than replacing a PM with the least unpopular choice.

We hit a high of 5394 just shy of the crucial 5400 level.

US reporting has started well with Alcoa but most analysts will be watching the banks for any guidance to our own much maligned banking sector. Some nerves and vertigo may creep in to the US tonight. Seems strange that the strong US jobs numbers have not reignited fears of a rate rise.

STOCKS AND SECTORS

- Resources continue to be the stand out sector especially in base metals which continue to play catch up. South32 (S32) +5.41%, Sandfire Resources (SFR) +3.39% and Incitec Pivot (IPL) +4.41%.

- Gold stocks slipped with Silver Lake (SLR) -6.38% and Evolution Mining (EVN) -3.92% following broker upgrades to target prices playing catch up to current prices.

- Energy stocks struggled but coal continues to attract bottom pickers with even New Hope (NHC) +1.03% now following in Whitehaven Coal (WHC) +2.74% up again on potential corporate action.

- Banks slid from early strength to be only up around 0.5%-1%. The big four basket closed at $153 off the intraday highs.

- Gaming stocks did well Star Group (SGR) +1.08% and Tabcorp (TAH) +2.33% recovering after the greyhound ban looks to be slightly more problematic than first thought by the NSW government.

- Expensive defensives took a breather as analysts are starting to question the PEs after stunning performance. Transurban (TCL) -0.74%, Sydney Airport (SYD) -1.39% and Macquarie Atlas Road (MQA) -2.74%.

- London stocks rallied hard but cooled on profit taking Henderson Group (HGG) +2.75% and BT Investment (BTT) +1.54%.

- Speculative stock of the day: Bassari Resources (BSR) +23.81% after the company updated the market on its Makabingui mining negotiations in Senegal. The company has a number of prospective gold projects in the country.

CORPORATE NEWS

- Alumina (AWC) +0.72% following Alcoa results this morning. Alcoa posted revenue of $US5.3 billion in the quarter, which was 10% lower the June quarter of 2015. The company posted net income of $US135 million in the quarter, in a result that was better than expected.

- Impedimed (IPD) +8.57% having received a new US payment rate for its L-Dex procedure for the assessment of lymphoedema. Under the new code, the CMS has increased the payment by 13.1% to USA$127.42 a treatment.

- Mirvac Group (MGR) unchanged after the company announced they would split their results into four business segments to ‘unlock the full value of our business’.

- Peninsula Energy (PEN) +% after announcing that Uranium production was steadily increasing at the Atlance project in Wyoming.

- Base Resources (BSE) -13.51% following a disappointing investor presentation.

- Galaxy Resources (GXY) -3.92% has signed a second offtake agreement between General Mining (GMM) -0.62% and Mitsubishi Corp to supply 15,000 tonnes of lithium concentrate in 2016 and 60,000 tonnes in 2107. The company has received a prepayment of $4.5m.

- Telstra (TLS) unchanged, the company had 41% market share in retail fixed line broadband market, according to the Australian Competition and Consumer Commission (ACCC) before the NBN and over the last five years that has not changed. Optus 14%, iiNet 14%, TPG, 13%, M2 9% and others 9%.

- The Australian Bankers’ Association (ABA) announced on Tuesday it had appointed Mr Stephen Sedgwick, a former public service commissioner, and a panel of experts to conduct an independent, industry-funded, review of retail banking remuneration as the fear of a major Royal Commission fades.

ECONOMIC NEWS

- The NAB business confidence index has risen to +6, better than the +4 expected by some economists and up from the +3 previously. The Business Conditions Index rose 2 points to +12 in June, around the highest since the global financial crisis. NAB said most industry groups reported a pick-up in conditions, although retailers were a “notable exception”.

- The ANZ-Roy Morgan Consumer Confidence index has fallen 0.5% to 115.2, the third consecutive weekly fall and below the 4-week average. ANZ said the falls were due to political uncertainty and concerns over global growth.

- Households were 4.1% less confident about the economy over the next 12 months and 2.7% more downbeat about the economic outlook over the next five years.

ASIAN NEWS

In China

- In northern China, the government has ordered cuts to output for the rest of this month to try to improve air quality in Beijing.

- October benchmark contract for rebar on the Shanghai Futures Exchange surged 3.7% cent to 2514 yuan a tonne and to a more than two-month high.

- The most-traded metallurgical coke futures on the Dalian Commodity Exchange surged nearly 6% to 1,006.5 yuan a tonne.

- Coking coal futures climbed 3.8 % to 758 yuan a tonne and iron ore futures surged 3.6% to 443 yuan.

- Baosteel Group is rumoured to be planning to cut capacity by 9.2m tonnes between 2016-2018

In Japan

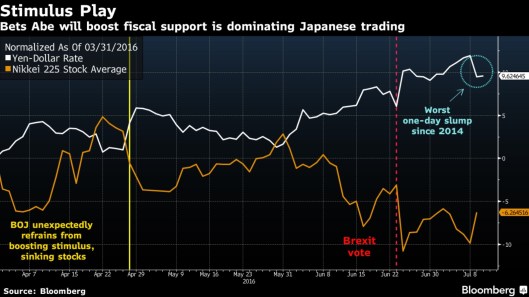

- Japan’s shares made their biggest two-day jump since February as PM Abe ordered his ministers to draw up a plan to pump another 20 trillion yen into the economy. Details were sketchy though with no decisions on how it will be financed or the timing of the stimulus measures. The expected timetable is, details in August and stimulus in September.

EUROPE AND THE US

- Finance ministers from the EU will meet for talks in Brussels on Tuesday.

- The International Court is due to deliver its ruling on a challenge brought by the Philippines to China’s claim to more than 80% of the South China Sea. Not that China will take any notice of course.

- Italy faces “two lost decades” unless the government does more to raise living standards, clean up the country’s banks and control its massive debt mountain, the IMF has warned. Unemployment is still 12% and GDP growth at 1% for the next two years, at least according to the IMF. Debt to GDP of 133% leaves them little room either.

- The IMF has also said that the problems of the weaker Italian banks could weigh on the entire banking system.

- Thursday will bring a change in UK PM and the sterling buds of May begins.

And finally…..

A guy goes to the supermarket and notices an attractive woman waving at him. She says hello. He’s rather taken aback because he can’t place where he knows her from.

So he says, “Do you know me?” To which she replies, “I think you’re the father of one of my kids.” Now his mind travels back to the only time he has ever been unfaithful to his wife and says, “My God, are you the stripper from my bachelor party that I made love to on the pool table with all my buddies watching while your partner whipped my butt with wet celery?”

She looks into his eyes and says calmly, “No, I’m your son’s teacher.”

Clarence

XXX

From our sponsors!