ASX 200 down 55.4 points to 5233.2 on widespread selling with banks in focus. GDP numbers send economists back to the drawing board and the AUD higher with 73 cents in its sights overnight. Asian markets drop on Chinese data and Abe moves on sales tax and stimulus. Japan down 1.62% and China down 0.13%. US Futures up 4.

Winter is coming

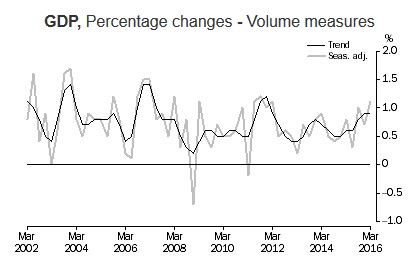

The official start of Winter sent a shiver through the markets today. Overnight leads and a soggy futures market were exaggerated with a across the board sell off. We have had seven weeks of gains and we needed a rest. Today we saw the market test 5300, as we touched the bottom of our new trading range before we saw some buying. The market was on tenterhooks before the GDP number at 11.30 am and the much better than expected number gave us a chance to rally before it slipped again. We had a range of 5306 -5366 for the day but the news seems to be now in the glass half empty camp rather than half full. Don’t they know they can refill the glass at any time. Anyway the AUD rallied on the GDP number and we completely ignored the better than expected Chinese data showing the world’s second biggest economy is stable.

It looks like the RBA will be on hold with any more rate cuts after the 3.1% headline number.

Banks were once again the focal point for the sellers as the hybrid program continues to suck money out of the sector.

Having tested the top of the recent range at 5400 it looks like momentum has slowed and we may see further weakness as we head towards the Fed meeting and the Brexit vote. If 5300 gives way we may see a move back to 5200. Hard to get bullish for any move back up above 5400. Short term trend is down.

Stocks and Sector Highlights

- Resources: BHP-3.09% dominated the sector together with South32 (S32)-4.49%. Lithium stocks though continue to leave the rest behind. Orocobre (ORE)+3.08% and Galaxy (GXY)+7.53%

- Energy: Some profit taking as we head into the OPEC meeting which starts on Thursday. Santos (STO)-3.97% on a drilling report but Woodside (WPL) -1.79% slips too.

- Gold: A rare bright spot today Newcrest (NCM)+2.05%, Dacian Gold (DCN)+8.6% in the small caps having a great day.

- Financials and Banks: A 1%-1.5%% fall across the board for the big four with wealth managers down too. Macquarie Group (MQG)-1.56%. Big faller today was Clydesdale (CYB) -5.34%.

- Industrials: Continued pressure on the grocery sector with Woolworths (WOW)-% and Wesfarmers (WES)-0.49%. Telstra (TLS)-1.25% continues to be sold off

- Speculative Stock of the Day: Rox Resources (RXL)+107.14% following an announcement on the maiden inferred resource at their world class Zn-Pb resource at Teena in the NT.

- IPO Focus: GTN+12.11% after listing today. The company supplies traffic reports for media channels and leverages its platform for advertising and partnership programs. Think Vic Lorusso and the morning traffic report.

Corporate News

- ALA(ALQ) Trading halt following a potential change of control event. Trading update two days ago looks to have opened the door to an opportunistic approach.

- Mesoblast (MSB) -% Trading halt pending an announcement on a material corporate development.

- Sirtex (SRX)-7.17% after announcing a lacklustre trading update. America seems to be doing well with 18-20% sales growth but EMEA and APAC suffering due to delays in product reimbursement and a tighter funding environment in several European markets.

- Mineral Resources (MIN)+3.41% Lithium offtake agreement for their Mt Marion project with Neometals (NMT)+1.04%.

- Amcor (AMC)-0.8% completion of the Alusa acquisition. Alusa is the largest flexible packaging business in South America with sales of around US$375m.

Economic News

- GDP grew a huge 1.1% in the first quarter which was far better than analysts had predicted and for the year we are now growing at 3.1%. This is a good result whichever way you dice it and means the RBA will be less likely to follow through with rate cuts next week or even July.

- Chances of an August move fell to 52 %, from 60 % before the GDP data, according to interest rate futures, and most economists still expect at least one more rate cut this year.

Courtesy of TD Securities.

In housing news:

- House price growth is accelerating again with the national growth rate back to 10 % in the year to the end of May. In December last year, the annual growth in the CoreLogic Home Value Index had slowed to 7.4 %. In May, the CoreLogic Hedonic Home Value Index rose 1.6 % across the capitals driven largely by a strong 3.1 % growth in Sydney, compared to 1.6 % for Melbourne.

In China:

- Official Purchasing Managers’ Index (PMI) was steady at 50.1 in May, and just above the 50-point mark that separates growth from contraction on a monthly basis.

- Official non-manufacturing Purchasing Managers’ Index (PMI) stood at 53.1 in May, compared with the previous reading of 53.5 but still well above the 50-point mark that separates growth from contraction

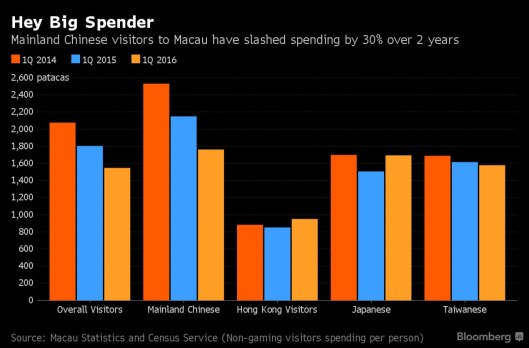

- Macau casino revenues fell 9.6% in May compared with 9.5% drop in April. Gross gaming receipts fell 9.6 % to 18.4 billion patacas ($2.3 billion), completing a two-year decline, according to data from Macau’s Gaming Inspection and Coordination Bureau. That followed a 9.5 % decrease in April. Not good news for Crown Resorts (CWN)-0.42%.

In Japan:

- PM Abe has announced a push back in the sales tax increase which was due to be brought in in 2017 of a 2% rise to 10%. He has now pushed it out another 2 ½ years which is forever in Japanese terms.

- Abe’s government is set to propose a stimulus package of 5-10 trillion yen ($45-$90 billion) in a special legislative session after the July election

Europe and the US

- Europe and the US are racing to keep their trade agreement on track before the Obama administration ends.

- The UN World Tourism Organisation says tourism spending has outpaced global trade for the fourth year in a row. The US followed by China are the world’s most popular destinations, followed by France and Spain. According to the UNWTO’s figures, released earlier this month, international tourism grew by 4% in 2015 generating $1.4trn ($966bn).

- The disruption to France continue ahead of Euro 2016 with Resident Hollande pushing ahead with his controversial labour reforms and facing off against the strike action across the country.

- Brexit rears its head again with a new poll showing the vote is closer than many thought. Bookies seem to be at odds with that view

And finally the head of now defunct stockbroker BBY, Glenn Rosewall has been revealed as a big supporter of a psychic to run his business. Obviously not a very good one as they certainly did not see bankruptcy coming at all. Or maybe they did.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com