ASX 200 closes down 29.4 points to 5378.6 after toying with 5400 again and finishing near its low. Financials and industrials slip across the board in lacklustre trade. AUD jumps to 72.4 cents on better economic numbers whilst China posts strong gains up 3.04% and Tokyo up 1.05% US Futures closed.

After a very soggy start to the day primarily due to weakness in the banking sector the market clawed its way back into the game and above 5400. The early weakness may have been attributed to yet another hybrid issue from the banking sausage machine that churns them out in order to keep retail brokers in school fees. The 1% commission is a life line and the appetite seems to be insatiable for the product with yield hungry investors. It does however sap demand for the underlying equities and we saw some selling of underlying shares to make room for the hybrids.

Better than expected export number helped the AUD kick back above 72 cents and this too dragged the market higher as it popped above the seemingly magnetic 5400 level. Consumer stocks were dragged a little lower as media reports on the rise of Aldi hurt both Wesfarmers and Woolworths.

- Dalian iron ore futures in China, up 1% helping.

- Standard and Poor’s has highlighted their fears on the looming apartment glut just as banks slow their lending down leaving some settlement risk. Brisvegas seems to be following Sydney and Melbourne in the avalanche of units being built.

- Stage is set for an interesting GDP release after the stronger export numbers today. Economists are busy revising their GDP estimates back up towards 3%. Glenn and his pals will be watching closely to see if they panicked too much.

Stocks and Sector Highlights

- Resources: Second liners doing well with Lithium continuing to attract traders and investors. Orocobre (ORE)+5.58% and Pilbara Minerals (PLS)-0.76% after broker upgrades and research.

- Energy: Some profit taking as we head into the OPEC meeting which starts on Thursday. Woodside (WPL)-2.39% the biggest casualty.

- Gold: The sector continues to show signs of life lurching from sell off to rally. Newcrest (NCM)+1.33% and Resolute Mining (RSG)+8.54% the two performers.

- Financials and Banks: Softer early but staged a good turnaround during the session only to turn negative at the close. The winner was Clydesdale Bank (CYB) +2.65% again as the rally continues. Commonwealth Bank (CBA) -0.96% the worst. Wealth Managers enjoying some positive momentum, Platinum Asset Management (PTM)+1.7% the standout.

- Industrials: Consumer stocks doing well Beacon Lighting (BLX) +2.31% continue to bounce back as better construction numbers and home sales help home maker retailers. RCG Corp (RCG)+3.38% and Baby Bunting (BBN)+1.69%.

- Speculative Stock of the Day: Another day another Lithium Story. Latin Resources (LRS)+40% after claiming 70,000 hectares in Lithium Pegmatite district in Argentina.

- IPO Sky and Space Global (SAS) +40% debuts on the ASX after raising $4.5m. Narrowband communication through nano-satellites in case you were interested.

Corporate News

- National Bank (NAB) -0.37% has launched a $750m Hybrid issue today with quarterly distributions at a margin of 4.95%-5.1% over BBSW. (Yes remember that was the one allegedly fixed).

- Virgin Australia (VAH)+7.14% will join with China’s largest private airlines operator HNA in a deal to capitalise on the growing Asian tourist dollar. HNA will also take a 13 % stake at 30 cents in Virgin Australia worth $159 million as part of the deal. Virgin said this morning that HNA would increase its stake in the company to 19.99 % over time

- Flexigroup (FXL) -6.79% today announced a $30m write off today with the finish of its enterprise, paymate and telco business unit. They also announced they will separate the Blink, Think Office and Flexi Enterprise Brands. They said it now expected its FY2016 cash profit, excluding impairments, to hit $97m, up 8 % on last year. The number represents an improvement from prior forecasts for a $92m-$94m reading, although it falls just shy of analyst forecasts.

- ALS (ALQ)-2.88% Investor day following the downgrade yesterday. Brokers expecting more downgrades to come.

- Spark Infrastructure (SKI) and Duet (DUE)-0.84% have reported that SKI has used the current strong share price to exit its stake in Duet over a period of time. They sold 8% at 225 cents.

- Wesfarmers (WES)-2.1% back in the spotlight following a Fair Work Commission tribunal decision that found that it had underpaid 77,000 workers at Coles with lower penalty rates and casual loadings. It is expected to cost Coles millions in back pay.

- Oil Search (OSH)-1.31% gets important backing of its US$2.2bn takeover of InterOil from Institutional Shareholder Services (an unfortunate ISS tag). However, some brokers have suggested it will have to sweeten its cash offer for the company.

Economic News

- First quarter net exports will add a strong 1.1 % to GDP growth. The current account deficit shrank to $20.8bn in the first quarter, down from $22.6bn.

- Private sector credit growth remained within expectations, rising 0.5 % in April.

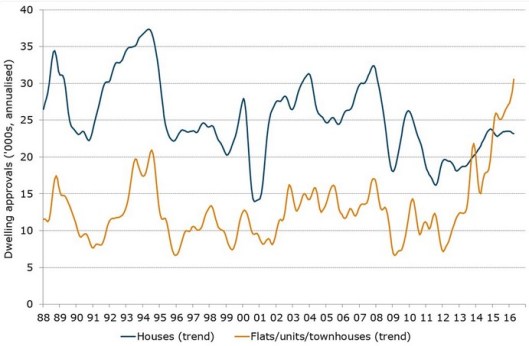

- New housing approvals rose in April to their highest monthly level in six months, pushed by an 8 % rise in apartments, townhouses and semi-detached dwellings.

- The total 20,243 new homes given the tick by planning authorities was the most since October. The number of apartments approved for construction rose to 10,490 from 9,650 in March – also the highest since October’s 10,838 – even as approvals of new detached houses fell 1.9 % month on month to 9,695.

In Asia

Chinese stocks surged Tuesday in the largest one-day gain in two months, on hopes it may soon be included soon in an influential global benchmark, MSCI Emerging Market Index.

- Strange times though as the Chinese futures market plunged by its daily limit of 10% in one minute only to recover again as quickly. Volume has dried up in the stock index futures markets in China and this is the second such unexplained crash in futures this month. A similar one occurred in Hong Kong on May 16th. Not a great look for a market trying to get the world to take it seriously.

In Japan

Industrial Production

- Output rose 0.3 % (versus 1.5 % decline forecast) from March, when it gained 3.8 %.

- Production is projected to rise 2.2 % in May, and then 0.3 % in June.

- Measured year-on-year, industrial production fell 3.5 % (versus 5 % drop forecast) after rising 0.2 % in March.

Household spending

- Household spending fell 0.4 % from a year earlier (versus 1.3% drop forecast), following a 5.3 % decline in March.

Unemployment

- The unemployment rate was unchanged at 3.2 % (versus 3.2 % forecast).

- The job-to-applicant ratio was 1.34 (versus 1.30 forecast), indicating a tight employment market.

Europe and the US

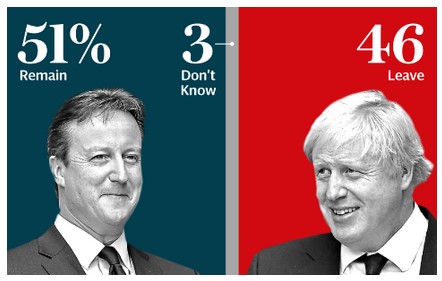

Should I stay or should I go?

Latest poll on ‘Brexit’-Borders and immigration the biggest ‘leave’ drawcard.

- Industrial unrest spreading across France as railway workers join the ‘holiday’ spirit with a strike.

And finally those old Disney VHS tapes may have been the greatest investment you could have made for your kids.

Good luck digging them out.

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com