ASX 200 down 44 points to 5279 as selling accelerates as 5300 gives way. Financials and healthcare in the spotlight. Volume on the low side as traders await macro-economic events and meetings. Asian markets slip again with Japan the worst of the bunch down 2.36%. China unchanged at lunch. AUD 72.40 cents. US Futures down 39.

A soft start gave way once again to selling as momentum players jumped on the band wagon to trigger stops below 5300. The selling picked up as Asian markets came on line around mid-day so suspect the HK funds are taking profits in the region as a whole. Financials were in the crosshairs today with the big four basket falling to $160. Insurers too struggled with losses in IAG and QBE of around 1%. The smattering of private equity action was unable to inspire the buyers today despite an agreed deal now for Patties of a Four and Twenty plus sauce option, and even much maligned ALS were in the bidders sights as private equity emerged from the shadows to lob a highly conditional, back of an envelope bid at 530 cents by way of scheme of arrangement.

After seven weeks of gains and a big 3.3% rally since the last OPEC meeting in Doha, it was only a matter of time until the momentum faded and the sellers took charge. Today seemed to be that day. Actually we are now 150 points (2.7%) off our recent 5427 high on 27th May.

Many funds have missed the rally as they were overweight cash and the FOMO together with some short covering has pushed the index up. The pullback will come as sweet relief for some and an opportunity for others. With rates low and potentially heading lower this will distort asset prices to the max. We have seen that in property prices in capital cities and although equities have missed out a little the favourite retail favourite stocks have pushed ever one wards and upwards. There will come a time when investors should seriously consider their exposure to the crowded trades and start to move out of the fashion into the less fashionable sectors. Just like Hula Hoops or an Apple watch their day in the sun can only last so long. Even the Blackmores infant formula bubble has burst after all.

Stocks and Sector Highlights:

- Aged care sector smashed on research report from Merrill Lynch. Sector facing zero earnings growth. Estia Health (EHE)-5.67%, Japara Healthcare (JHC)-8.99% and Regis (REG)-8.52% hit hard.

- Financials in spotlight. Big four banks down around 1.5%. Goldmans downgrades regional banks. Bank of Queensland (BOQ)-3% and Bendigo and Adelaide (BEN)-5.61%.

- Lithium bubble burst by Pierpont article suggesting it’s a Poseidon-like bubble and unsustainable. Orocobre (ORE)-6.84% and Galaxy (GXY)-3%.

- Speculative stock of the day: Kidman Resources (KDR) +40.6% after ‘spectacular’ lithium assays at Mt Holland project in WA.

Corporate News

- G8 Education (GEM) -2.48% – Update on debt and cash flow.Net debt to EBITDA is now 2.1 times after recent redemptions and rollovers.

- Cardno (CDD) -Accelerated non renounceable entitlement offer.1:1.07 at 40 cents to raise $92.5m

- Patties Food (PFL)+6.96%-Board backs private equity bid at 165 cents.

- ALS +27.2% rejects Bain and Advent private equity bid at 530 cents as inadequate.

- Seek (SEK)-3.3% after MD Seek Education resigns.

- Challenger (CGHF)-% holds an investor day.

- Z Energy+4.1% after the NZ super fund has engaged UBS to sell 36.4m shares in a block trade agreement through a bookbuild.

Economic News

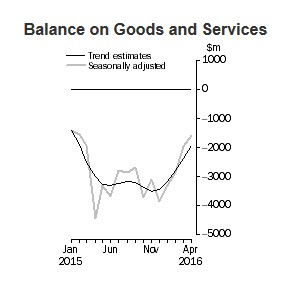

- Australia’s trade gap narrowed to $1.58 billion in April, down from $2.26 billion in March, and well below the $2.1 billion deficit economists were expecting.

- Exports rose 1.0 % in the month, while imports were down 1.0 %.

- Retail spending rose 0.2% in April, which missed economists’ expectations of a 0.3% rise. There was a 1% rise in the cafes and restaurants category while food sales fell 0.3%.

- Lending to business has risen by 7.4% in April, the biggest rise since January 2009.

- Go to economist at the moment, Paul Dales from Capital Economics has cut his forecast for cash rates to 1% as they believe inflation will be lower for much longer. Macquarie and Morgan Stanley are already there with the 1% call.

In Asia

- Japanese stocks drop the most in a month following PM Abe postponement of sales tax hike to 2020

Europe and the US

- Saudi Wealth fund takes a $3.5bn stake in Uber.

- OPEC meeting in Vienna. Talk of a ceiling on production and an olive branch from Saudi to other OPEC members helping keep WTI crude bubbling around $50.

- ECB meeting tonight. Rate decision and press conference from Draghi.

- Apple is hoping to sell a fixed rate June 2020 note for Australian investors at a yield premium of 0.85% above BBSW. Last year they issued $2.25 bn of notes for 4 and 7 years.

- Brazilian economy shrinks 5.4% Big challenge for new Temer government.

- S. jobs report from the ADP Research Institute is forecast to show 173,000 workers were taken on in May, up from 156,000 the previous month. Official employment figures are due Friday.

- Brexit fears back on in Europe as polls narrow.

Online Guardian poll

And finally one forecaster has suggested that by 2025 all cars in Australia will be electric. Given that there were just 948 electric cars sold in 2014 out of 1.1m, it does seem like a big stretch.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com