ASX 200 closes up 2.1 points to 5408 after a day of back and forth. Low volumes and 5400 proving to be both support and resistance at times. Consumer staples stronger as banks wane. Asian markets mixed with China up 0.08% and Japan up 1.29%. AUD weaker at 71.62 and US Futures closed for Memorial Day.

A quiet day where the market seemed unable to make up its mind. After solid leads from international markets and a good performance on the futures there was some optimism that we could climb clear of the 5400 level. However, a mid-morning sell off in the banks and some profit taking across the board ensured we struggled to keep our noses in front today. Banks as usual were the swing factors today going from positive to negative with most eyed pinned on the swathe of data that is due out later this week from here and overseas.

Stocks and Sector Highlights

- Resources: Muted performance from the big miners BHP-0.67% and Oz Minerals (OZL)-1.79% the biggest losers.

- Energy: Mixed performance from oilers, Caltex (CTX)-1.34% eased on the Woolworths news

- Gold: Weaker across the board with Evolution Mining (EVN)-3.85% and Silver Lake (SLR)-9.78% together with Resolute Resources(RSG)-11.35% the stand out losers.

- Financials and Banks: Once again the swing factor with the big four basket today at $162.00 with National Bank (NAB)-0.18% the only of the four to escape some selling pressure. Macquarie Group (MQG)+1.32%. REITS continue to hold firm in the low rate environment. Scentre Group (SCG)+0.65% and Westfield Corp (WFD)+0.75%.

- Industrials: Qantas(QAN)+3.33% following slightly better than expected traffic and capacity numbers. CSL +0.59%

- Speculative Stock of the Day: Galaxy (GXY) +11.39% and General Mining (GMM)+15.45% after announcing plans to merge the two businesses to become a $700m diversified lithium producer.

Corporate News

- The world’s biggest pie maker Patties Food Limited (PFL)+17.67% after receiving a non-binding highly conditional offer from Pacific Equity Partners at 165 cents in cash. The board has engaged with the potential suitors.

- ALS (ALQ) -7.13% after reporting full year earnings that disappointed estimates. Underlying profits fell 27% to $99m while revenue dropped 8.6% to $1.36bn. They also posted a statutory annual loss of $240.7 million, mainly due to impairment charges of $314 m against the company’s oil and gas investments. final dividend of 6 cents.

- Spotless (SPO) +5.53% after reaffirming guidance and the possibility of a sale of their laundries business for around $650m. Spotless may offload its laundries unit, which generates around 10 % of group revenues, but which has the fattest margins of any of the group businesses, at around 28 %.

- Lend lease (LLC)+1.42% sold all 391 apartments of the third and final stage of its Darling Square apartments on Saturday, collecting about $460 million. In a four-hour frenzy, a mostly domestic group of 400 buyers, who started turning up from 8am, scooped up the apartments priced between $630,000 and $3.5 million.

- AMP -0.88% will announce that it is banning mortgage lending to most non-resident borrowers, highlighting growing lender nerves about possible fraud and money laundering.

- Lynas (LYG)-2.86% has done a deal with its lenders to postpone debt repayments due in May and September until December. The US$2m principal payment due in June together with interest rate payments from January will now be due in December without interest or penalty.

- New LIC entrant Wilson Leaders Fund (WLE)-2.73% joined the boards today including the option (WLEO) it is trading at a slight premium.

- Woolworths (WOW)+1.4% was buoyed today with talk that BP had sent a team of executives out to Australia to run the slide run over the Woolworths petrol service station business. This would free cash up for investment in the core business but may run into ACCC issues or may even trigger a rival bid from Caltex (CTX)+%.

- Australian New Zealand bank (ANZ)-0.62% ANZ is planning a US-dollar hybrid of at least $US750 million. The plan is for a perpetual security with either a 5 year or 10 year call date and is expected to have a cost of more than 550 basis points above the bank bill swap rate once swapped back into Aussie dollars.

- Alumina (AWC) unchanged after acting to protect existing shareholders from Alcoa’s proposed corporate separation.

- Clearview (CVW) in a trading halt as the company updates the market and is raising $50m through a 1:10.2 entitlement offer at 85 cents. Underlying NPAT for the full year 2016 results (when compared to 30 June 2015), will be broadly consistent with those achieved in the 1H FY16 and in the range of 30%-35%. Update looks positive.

Economic News

- Company gross operating profits fell 4.7 % in the March quarter, missing market expectations for a 0.4 % rise. They were down 8.4 % in the 12 months to March. The estimate of income from sales by manufacturers fell 0.3 % in seasonally adjusted chain volume measures, and for wholesalers it was up 3.2 %. Estimated business inventories, in seasonally adjusted chain volume terms, rose 0.4 % in the first quarter.

- Housing Industry Association (HIA) said its survey of large-volume builders showed new home sales fell a seasonally adjusted 4.7 % in April, down from March when they jumped 8.9 %.

- Another success story in the hedge space’ Bitcoins’ following the lead of the gold price in AUD in the last year or so.

In Asia

- The offshore yuan has extended a weekly decline after China’s central bank weakened the currency’s daily reference rate to the lowest level since February 2011. The fixing was cut by 0.45 % to 6.5784 per US dollar after the greenback strengthened

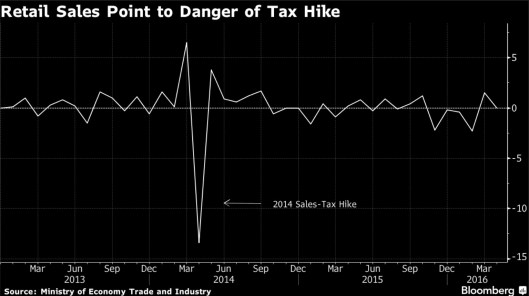

- Japan’s retail sales were unchanged in April from the previous month, a government report showed Monday. The median forecast of economists surveyed by Bloomberg was for a 0.6 % decline. From a year earlier, sales fell 0.8 %, compared with a decline of 1.2 % forecast in the survey.

- PM Abe has been pessimistic about the global; growth outlook and it may be that his next hike in the sales tax is off the agenda. One adviser suggested Japan needs to delay increasing the sales tax until late 2019 to sustain its economic recovery.

- Noble Group Ltd. said Yusuf Alireza resigned as chief executive officer and announced a plan to sell part of its gas and power unit.

Europe and the US

- Holidays tonight in the UK and the US.

- EU set to impose record cartel fine on truck makers Six groups set aside €2.6bn over charges they fixed prices and delayed emission technologies.

- France has no intentions of backing down on Google taxes, French finance minister Michel Sapin confirmed. French authorities are said to be pursuing some €1.6bn in corporation tax and VAT from Google, after the Californian company paid just €5m of taxes in France on €225.4m revenues in 2014.

Clarence

xxxx

Get a Global take on things at http://www.ntmarkets.com