ASX 200 closes up 15.6 points at 5388.1 after a volatile options expiry day. Energy, banks and material stocks the big winners as WTI Crude pushes through $50. Asian markets mixed as China weakens by 0.8% and Japan slightly higher up 0.52%. AUD back above 72 cents after a slight drop on the Capex numbers. US futures down 7.

Volatility to the max today as the local market lurched from pillar to post on options expiry day. After a very strong opening on the back of US market moves the index succumbed to profit taking and some serious caution ahead of the Capex number mid-morning. Before the number, the ASX 200 gave up all the gains and reversed into negative territory as regional markets took a hit on some comments coming from Japan knocking us hard before buying again took it back up. 5400 looks to be a serious psychological level and we are unable to break through it. Banks were once again the swing vote in the market with BHP in full flight. The fall-out from Wesfarmers (WES) write down continues and has now spilled over in to Woolworths (WOW).

The range today was 5402-5354 as the market range telescopes with a break out hopefully looming. Volume again on the low side considering the volatility.

As the ASX 200 rises the ASX Volatility Index is falling.

After seven straight weeks of rises, we may see some more backing and filling as we mount our summit attempt.

Top of the Pops

- Commonwealth Bank leads a group of 35 Australian firms ranked among Forbes’ annual Global 2000 list, which calculates the world’s 2000 largest public companies by looking at sales, profits, assets and market value.

- CBA is the top-ranked Australian company at No.58 with a market value of $US99.2 billion. Rivals Westpac (72), ANZ (84) and National Australia Bank (88) are also in the top 100, with telco giant Telstra the next highest-ranked Australian company at No.262.

- Wesfarmers (264) and supermarket rival Woolworths (760) both feature, as do insurance giants Suncorp (530), QBE (571) and IAG (891).

Talking of top. Harry Triguboff has topped the BRW Rich List for the first time. $10.62bn to his name. Apartment boom is going well for some.

Stocks and Sector Highlights

- Resources: BHP +2.7% the stand out on the higher crude price.

- Energy: In demand Woodside (WPL)+2.06%, Santos (STO)+4.91% and Origin Energy (ORG)+2.68%. Coal stock Whitehaven Coal (WHC) +9.33% is continuing its solid recovery from around 37 cents back in February.

- Gold: A solid bounce despite the lull in the bullion price although in AUD terms it is still around $1706 not far from its all-time high. Perseus Mining (PRU)+11.58% and Silver Lake (SLR)+5.43% the bolters.

- Financials and Banks: Suncorp (SUN)-3.64% brokers cut ratings after an investor day yesterday. Big four banks see sawed with National Bank (NAB)-0.44% slipping slightly as Clydesdale Bank (CYB) +% continued to power ahead.

- Industrials: Dominated by moves in Telstra (TLS)-0.53% Woolworths (WOW)-1.21% and Wesfarmers (WES)-3.58%. Spotless Group (SPO) -9.91%. Great Rally from CSL+1.11% to a fresh high on an FDA approval.

- Speculative Stock of the Day: Austin Exploration (AKK) +81.82% after striking oil in Colorado. Drilling has intersected an 800ft column of crude oil. Testing to begin after they wipe the oil and smiles off their faces.

Corporate News

- Asciano (AIO) -0.11% The ACCC released a statement of issues which means its final decision on the drawn out takeover deal will now be delayed until July 21 and the transaction will now stretch to more than a year if completed. the regulator had received a large number of submissions with some in the market concerned by the prospect of less competition from the tie-up between Patrick, Qube and ACFS.

- Aristocrat (ALL)+0.16% announced net profits for the first half of 2016 by 66% to $183.2 million, in line with expectations, due to strong growth in Australia and North America and more punters using its social gaming apps. They increased the dividend for the six-monthly period by 2c to 10c per share. Revenue increased by 47 per cent to $1.01 billion. Second half growth is expected to match the first half and is on track to lift its full year profit by 55%. Strong earnings growth from their US acquisition VGT.

- Orocobre (ORE)+6.15% another strong day after the company released and investor update which they will present in Las Vegas at a Lithium conference.

- Santos (STO)+4.91% after announcing the GLNG train 2 had started producing LNG from Curtis Island.

- Yowie (YOW)-1.03% after signing a deal to license a Yo-Kai watch deal in Japan.

- Fonterra (FSF)+0.57% are forecasting a Farmgate milk price of NZ$4.25. This may have implications for our big four banks through non-performing loans to NZ farmers.

Economic News

- Business investment (capex) fell by 5.2 %in the March quarter, which was worse than forecasts.

- The closely-watched figures cover investment in capital goods which includes such things as buildings and equipment.

- Businesses collectively expect to invest $126.819 billion on capital goods by the end of the 2015-16 financial year, which is 15.3 % lower than the same estimate made for the previous year, the ABS said.

For the full breakdown from the ABS

The New Zealand budget was handed down today: From Bloomberg a quick round up of the winners and losers.

Winners

Entrepreneurs

- The government is trumpeting a NZ$761 million ($511 million) innovation package to encourage entrepreneurship, skills and economic growth. It will boost investment in science and innovation, tertiary education and apprenticeship programs.

Small Businesses

- A new pay-as-you-go option will give up to 110,000 small businesses a way to pay tax as they earn income from April 1, 2018.

Losers

Income Earners

- There is no mention in the budget of tax cuts.

Smokers

- Starting Jan. 1, the government will increase the tax on tobacco by 10 percent each year for the next four years, as part of a package of measures aimed at making New Zealand smoke free by 2025. The price of a standard pack of 20 cigarettes will likely increase to around NZ$30 in 2020 from NZ$20 today, generating an extra NZ$435 million in tax revenue.

Pollution Emitters

- The government is phasing out over three years a subsidy in the emissions trading scheme that allows some businesses to pay one emissions unit for every two tons of pollution they emit. The move will help New Zealand meet its target of reducing emissions to 30 percent below 2005 levels by 2030, the government said.

In Asia

- China warns G7 not to ‘escalate tensions’ in Asia. Beijing tells group from which it is excluded to focus on economic matters

- G7 leaders are meeting in Japan. A number of issues on the agenda. Steel overcapacity is a general problem for EU. Beijing which is not in the G7 meeting despite China being the second largest economy in the world.

- Oil and global markets back in sync.

- The chief executive officer of China’s Lufax, peer-to-peer lender and broker, said an initial public offering will be postponed until next year amid turmoil in the market and questions over government regulation.

Europe and the US

- SGX (the Singaporean Exchange) began discussions with the Baltic Exchange three months ago in the hope of buying the 250-year-old firm, which offers trading in cargo contracts as well as derivatives based on the global shipping industry.

- The Baltic Dry index is often used as a proxy for commodity trade around the world. The deal could be worth around US$100m, according to Reuters.

- French Nuclear workers have joined the strike by others in the energy sector including oil refinery workers and the train drivers as the strike looks to be spreading. The issue is over controversial labour reforms which the French government forced through parliament last month.

- Nuclear power provides about 75% of the country’s electricity. Transport Minister Alain Vidalies said 40% of petrol stations around Paris were struggling to get fuel. President Francois Hollande told ministers on Wednesday that “everything will be done to ensure the French people and the economy is supplied”. Analysts say France has nearly four months of fuel reserves.

And finally:

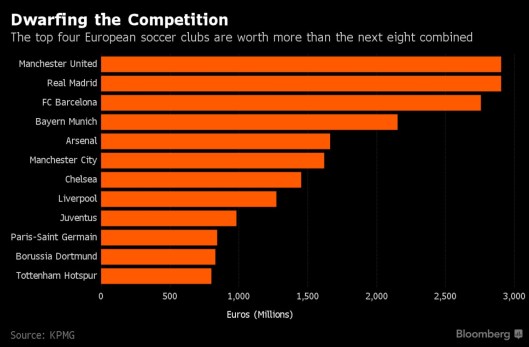

- Despite coming fifth in the EPL the value of Manchester United is a lesson in branding and marketing success. Man Utd is worth EUR 2.9bn according to KPMG which makes the shares that trade in New York look a little cheap as the market valuation is only US$2.8bn

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com