ASX 200 rallies 76.9 points to briefly test the 5400 level and retreat to 5372.5 having bounced from the low of the range yesterday. Banks and materials rally in unison. Asian markets mixed, China down 0.15% and Japan up 1.57%. AUD back above 72 at 72.09 cents with US futures up 39 points.

It is looking like we will have a 7th week of gains at the present rate. From the outset it was game on as US and Euro markets provided the shot in the arm we needed to rally hard. Banks were in demand after Clydesdale Bank (CYB) results and the US counter parts rallied hard. The short position in our local banks has been building and building and today they were forced to run for cover today. Add in a decent rally in resources on the back of a steadier iron ore price and we synchronised for a change.

Volume was a little underwhelming at $5bn given the strong adrenaline shot, and after the initial rush we basically flat lined again. Volatility was from the open with a lack of follow through to breech the 5400 level. We may again baulk at this psychological level and trickle back down. After 7 weeks of gains we need a rest. Support base is very strong and the world is now looking at the half full story and an increasingly growing US economy. China fears have receded from our forefront.

The late fade on the match out was slightly worrying and given the talking heads on TV are finding it hard to find value this may be a portent for a fall back tomorrow on profit taking.

We could be seeing some market on close selling every afternoon just knocking the gloss off the headline index as traders take money off the table.

Stocks and Sector Highlights

- Resources: Stability in the iron ore price helped a recovery in miners. BHP +2.83% and Fortescue Mining (FMG)+1.75%. Well off their highs though. Base metal stocks also recovered with Independence group (IGO)+4.12% and Western Areas (WSA)+2.88% attracting buyers.

- Energy: Another positive day for the big oil stocks as crude pricing heading towards $50 for WTI. Woodside Petroleum (WPL)+2.65%, Origin Energy (ORG)+3.71% and Santos (STO)+2.64%

- Gold: Under serious pressure today as the US dollar resumes its move up on rate rises perhaps as early as June. Losses across the board with Newcrest (NCM)-5.14% and Saracen Minerals (SAR)-10.24%. Losses were more muted in Evolution Mining (EVN)-1.42% and Regis Resources (RRL)-1.97%

- Financials and Banks: Superstars today. The big four were back in demand as the shorts were squeezed resulting in gains of around 2 % for the best of them. Research changes by Macquarie on Commonwealth Bank (CBA)+1.07% put a little dampener on the stock but Wealth Managers also had a strong day. Macquarie Group (MQG)+2.72%, Challenger Limited (CGF)+2.43% Suncorp (SUN)+1.07% and Magellan Financial (MFG)+2.58%. REITS solid with Westfield (WFD)+1.54%

- Industrials: Solid bounce today from Flight Centre (FLT)+2.89%. Telstra (TLS)+1.79% and CSL +1.14%. Cimic Group (CIM)+3.33% continues to push ever higher and Woolworths (WOW)+1.32% at the expense of Wesfarmers (WES)-0.17% after the Target write downs hit hard at first then the buyers emerged.

- Speculative Stock of the Day: Lake Resources (LKE)+263.64% following the proposed acquisition of a private Lithium focusses explorer. Any mention of lithium is enough to drive traders into a frenzy at the moment. Enjoy it while it lasts.

Corporate News

- Clydesdale Bank (CYB)+11.42% stunning results for the National Bank shareholders that have held on to the allocation as the stock soared today after some good numbers showing a cost out story in full flight. Costs down from $760m to $730m with underlying earnings of GBP 107m. The bank’s net interest margin of 2.25 % was slightly wider than a year earlier, and in line with expectations. In mortgages, where Clydesdale wants to take market share off bigger British banks, its loan book grew 9.8 %.

- Programmed (PRG)+10.24% after reporting a net loss of $98m however revenue jumped 54.6% to $2.22 largely due to the takeover of Skilled group where the integration is going well. Guidance continues for $100m-$110m for the coming year.

- Wesfarmers (WES)-0.17% warned today that its full year profit will be hit by write-downs and restructuring costs of up to $2.3 billion on its ailing Target chain and its struggling coal business. The conglomerate said this morning it would take a non-cash impairment of up to $1.3 billion on its Target business, mainly on the value of goodwill. Wesfarmers will also take a non-cash impairment of up to $850 million against its coal business, Curragh.

- Australian Agricultural Co (AAC)+12.37% Where’s the beef? Seems that AAC have it in spades with sales revenue soaring top $489m up 87% from $132m. Beef sales accounted for 88% of the revenue especially in the premium Wagyu space. No dividend to be paid but results are now coming in for shareholders after a three-year repositioning story is starting to bear fruit.

- Adelaide Brighton Cement (ABC)+4.24% Adelaide Brighton expects improved sales in several of its key products, due largely to demand from east coast markets. Chief executive Martin Brydon told the company’s annual general meeting that the company expects 2016 sales volumes of cement and clinker to be similar or slightly less than in 2015.They also expect significant growth in sales of pre-mixed concrete, and aggregate sales volumes, in 2016, due to stronger east coast markets.

- Primary Healthcare (PRY)+2.19% is under threat of a takeover from a Chinese group Jangho which is moving slowly and patiently up the share register now at 16.9%. Jangho bought the ASX company Vision Eye recently.

- Telstra (TLS)+1.79% has joined with others in an investment round of funding for US security start up vArmour. Telstra has invested only a $5-10m in the latest round but it does show that they are taking security seriously in their cloud services business and the protection of their growing data centre in Australia.

- Worley Parsons (WOR)+7.6% after an investor day and positive outlook commentary from the company. Focus on cost, cash and safety. Seems the market is getting more positive on the reinvestment in oil and gas assets by companies on the increasing oil outlook after years of decline and neglect.

Economic News

- The amount of construction work in Australia fell 2.6 % in the March quarter, which was worse than economists’ expectations of a 1.5 % fall. In the 12 months to March, construction work – a component of next week’s first-quarter GDP – was down 6.7 %, the ABS said this morning. Total building work done on homes and non-residential buildings such as offices and shops, fell 1.0 % in the quarter. Engineering work done, which includes mines, roads, bridges and the like, was down 4.2 % in the quarter.

In Asia

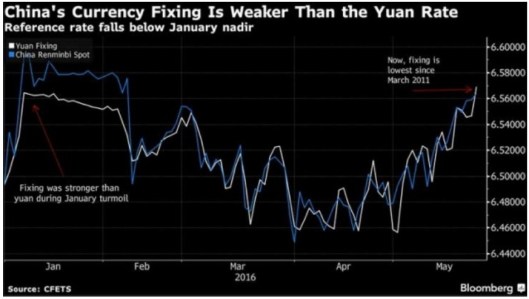

- China’s central bank has weakened its currency fixing to the lowest since March 2011 as the US dollar continues to strengthen. The reference rate was lowered by 0.3 % to 6.5693 per US dollar.

- China’s leading market regulator said that its clampdown on speculation in raw materials futures has successfully reined in the frenzy, and pledged to beef up oversight as the country seeks to dislodge rivals and become the global centre for commodities pricing.

Europe and the US

- Portuguese-backed consortium is in pole position to save BHS after Matalan founder John Hargreaves and Select Fashions Cafer Mahiroglu retreated from the bid battle.

- Greece reaches breakthrough debt deal. Eurozone finance ministers have agreed to extend further bailout loans to Greece as well as debt relief, in what they call a “major breakthrough”. After late-night talks in Brussels, the ministers agreed to unlock 10.3bn euros ($11.5bn; £7.8bn) in new loans.

- Toyota and Uber have joined forces to create a strategic partnership to allow Uber drivers to lease cars and the payments will be covered by the earnings they generate. In January, General Motors invested $500m in Uber’s main rival Lyft, while Apple recently announced plans to invest $1bn into Chinese ride-hailing service Didi Chuxing.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com