ASX 200 drops 60.12 points to 4946.4 on broad-based losses. Oil slips in Asian trading, China fails to rebound after savage falls yesterday, down another 2.96% at the break and inflation numbers give RBA no reason to cut rates. US Futures down 36 as Apple rocked to the core.

The market seemed to be suffering from an Australia Day hangover. After a tentative start, we slipped into modest losses before accelerating in the afternoon as Chinese markets failed to recover. Inflation numbers at 11.30am also took the wind out of our sails, pointing to a maintenance of the status quo on interest rates. Falls in the Asian oil price were unhelpful as were falls in US futures. As the afternoon wore on the sell-off continued and we closed near our lows for the day.

Shaping up as the worst January since 2008 with a fall so far of 6.6%.

Stocks and Sectors

- Banks gave up a significant part of their recent gains today with National Bank (NAB) -3.1% the worst of the bunch following the vote to rid itself of its English problem. Australia and New Zealand (ANZ) -1.95% announced some senior management reshuffling and other financials were also in the dog house with Macquarie Group (MQG) -2.1%, Perpetual (PPT) -2.56%, AMP -1.48% and QBE -1.48% the standouts. REITS, though, bucked the downward momentum with Scentre Group (SCG) +0.94%, GPT +1.26% and Folkestone Education Trust (FET) +3.79%.

- Resources slid again following disappointing Chinese numbers and a falling oil price again. Oil Search (OSH) -4.62% led the way followed by Origin Energy (ORG)-4.2%, Santos (STO) -2.7% and Woodside (WPL) -1.63%. Coal stocks were also sliding away with Whitehaven (WHC) -6.82% and No Hope (NHC) -4.0%.

- Big miners continued to follow a predictable path, BHP -1.77%, RIO -2.68% and Fortescue Metals (FMG) -3.95%. South32 (S32) -4.02% continued to head south although other base metal stocks held relatively steady. Sandfire Resources (SFR) -1.24% and Independence Group (IGO) +0.47%. Biggest losers in the sector was Mincor (MCR) -18.42% and Panoramic Resources (PAN) -30.83%.

- Gold stocks rallied led by Newcrest (NCM) +3.21%, OceanaGold (OGC) +7.2% and Evolution (EVN) +3.04% after a positive December quarterly production report.

- Industrials were soggy across the board. Mining services again horrible. Decmil (DCG) -4.50%,Seven Group (SVW) -2.42% and Cimic Group (CIM) -1.88%.

- Healthcare stocks were in minor day surgery today with CSL -1.64%, Ramsay Health Care (RHC) -1.02% and Sirtex (SRX) -2.48%.

- Builders also out of friends with James Hardie (JHX) -1.84% and CSR –2.76%. Amcor (AMC) -2.56% after announcing a small acquisition in China for US$13m together with some management changes.

- Speculative stock of the day: One we talked a few weeks ago, Holista Colltech (HCT) +63.04% following its breakthrough with the low GI white bread formula and a Q&A session to clarify the potential of its formula.

- Corporate Fail: Bitcon miner Bitcoin Group (BCG) has failed to attract the $20m it was seeking as part of an IPO. They managed to raise a huge $367,902.20 through the new ASX Bookbuild service. This did not include direct applications though and the proposed listing has been pushed back from Feb 2nd to the 8th.

Corporate News

- National Australia Bank (NAB) -3.1% held its crucial vote on its imminent divorce from the UK business this morning in Melbourne. Shareholders voted 98% to back the plan to hive off the Clydesdale Bank in a separate listing on the ASX and London. NAB’s price range for the float is £1.75 ($3.57) to £2.35 per Clydesdale share.

- GUD Holdings (GUD) -9.75% announced an earnings downgrade by as much as 8.8% as losses from Sunbeam on a weaker AUD and demand for Dexion shelving takes its toll. The company expects to earn $82-88m before interest, tax and one-off charges for the full year,compared with previous guidance of $90m and earnings of $58.9m in 2015.

- RIO -2.68% today announced the sale of its Mount Pleasant Thermal coal project to the privately owned MACH Energy Australia for $320. MACH is backed by Indonesian group Salim Group which owns part of Goodman Fielder. Mt Pleasant is a large mining project in the Hunter Valley, with total marketable reserves of 474 million tonnes of coal reserves. It has government approvals to produce 10.5 million tonnes of coal annually, but it has remained undeveloped.

- Greencross (GXL) +2.94% has announced that it had received a number of inquiries from interested parties following a rejected $740m takeover offer from TPG Group. The price was $6.45 a share and was put to the board back in December. Following board rejection, the company tried to buy 14.99% on market at $5.79. It succeeded in acquiring a 6.9% stake.

- Oil Search (OSH) -4.62% has written off most of its exploration assets in Kurdistan. December quarter revenue slipped 10% to $US342.9m on production of 7.51 million barrels of oil equivalent,which is up slightly from the 7.42 million barrels in the September quarter.

- Talking oil, AWE +56.94% today announced that it had sold its 10% stake in the US gas project Sugarloaf for $271m in cash. Once debt has been repaid the company will have $60m in the bank. It will have remaining projects at Waitsia, BassGas and Casino and other undeveloped assets.

- There is movement at the station for the word has passed around that market guru Geoff Wilson from Wilson Asset Management (WAM) +1.41% has approached Century Australia (CYA) +10.9% with a restructuring proposal. The proposal is for a buy back at the NTA of CYA which at the end of the year was 89.7 cents and then a new management contract with Wilson Asset Management.

Economic News

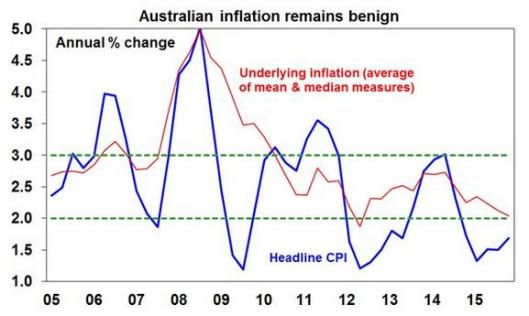

- December quarter inflation of 0.4% or 1.7% yoy. Underlying inflation coming in a tad higher than expected, at 0.6% for the December quarter, or 2.1% yoy.

- The RBA looks at two core inflation measures – trimmed mean and weighted median. Today’s report showed:

Key movers:

- Tobacco gained 7.4% QoQ

- Domestic holiday travel and accommodation climbed 5.9%

- International holiday travel and accommodation rose 2.4%

- Automotive fuel fell 5.7%

- Fruit prices dropped 2.6%

The report also showed quarterly inflation of 0.5% for tradable goods, which are affected by the currency and other international factors, and 0.4% for non-tradable goods, which are impacted by domestic variables.

Looks like the chance of a rate cut next week has shifted dramatically from 20% to 4%, while economists have pushed out longer term cut projections from June to August. No wonder the AUD is strong today at 70.27

In Asia

- Profits earned by Chinese industrial firms in December fell 4.7% from a year earlier, the seventh straight month of declines. Industrial profits – which cover large enterprises with annual revenue of more than 20 million yuan from their main operations – fell 2.3% in 2015 from 2014, the National Bureau of Statistics (NBS) said on Wednesday. That compared with 3.3% growth in 2014.

- The head of China’s NBS is being investigated for suspected corruption.

- Suzuki shares rose 10.5% on rumours that it was in talks with Toyota, up 3%, about a possible tie up. Both companies denied such talks. Toyota was named No 1 car company by sales, taking the crown from VW.

Europe and US

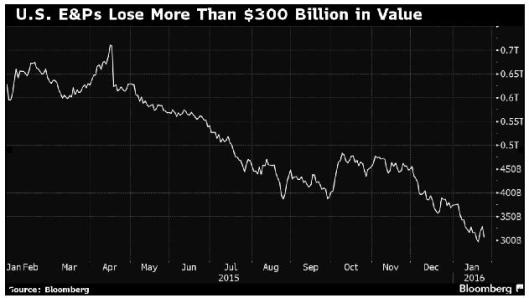

- During the next eight days, independent US oil explorers are expected to report 2015 losses totalling almost $14b, the result of the steepest price collapse in a generation.

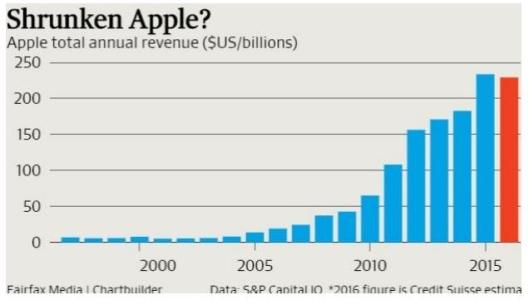

- The Apple sours a little as the slowdown on iPhone sales bites. iPhone 7 looks even more important now in September.

- Peak smartphone?

- Tim Cook said “We’re seeing extreme conditions unlike anything we’ve experienced before just about everywhere we look.” Not a good sign.

- Apple does have US$216bn on its balance sheet and gross margins of 40.1% and a low (no) tax status, so it is not all bad.

FOMC concludes tonight. Let the games begin.

Ahead in Europe

- FTSE -24 points.

- DAX +99 points.

- CAC +47 points.

Get a Global take on things at http://www.ntmarkets.com