Tags

ASX200, Australian Sharemarket, Ben Bernanke, BHP, cba, Charlie aitken, commonwealth bank, diggers and dealers, essex Lion, fairfax, Fortescue mining, gold, Interest Rates, iron ore, Mario Draghi, Whitehaven Tinkler coal bid cash

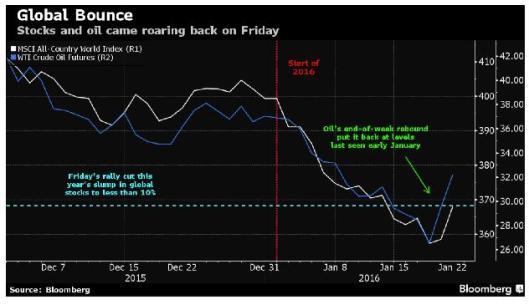

ASX 200 rises 90.6 points to 5006.6 on stimulus hopes and oils rebound. Low volumes though at around $4.2bn. Banks in demand along with energy stocks. Asian shares rally as oil stays above $32. China up 0.8% with Tokyo up 1.2%. US futures up 13.

After the positive overseas leads from Friday and the huge run in oil prices, it was inevitable that we would rally hard today. Volume was on the low side as many traders took advantage of a ‘claytons’ long weekend. A positive Chinese and Japanese market also helped sentiment and the market kicked around lunch time to a high of 4999.8, before another good push into the close ensured the level was breached well and truly on the close. Banks and other financials surprisingly led the gains with energy stocks kicking in.

It seems there is a whole generation of traders and computer systems that are addicted to central bank stimulus and throw a temper tantrum when things do not go their way. Maybe they need some tough love or a trip to the traders’ equivalent of ‘Brat Camp’.

Stocks and Sectors

- Banks, up around 3%, and financials were especially firm today with Australian and New Zealand Bank (ANZ) +3.43% the big winner whilst Challenger Financials (CGF) +5.99% reiterated its profit numbers and rallied hard. Other wealth managers also did well, Macquarie Group (MQG) +2.63%, Platinum Asset Management (PTM) +3.34% and Perpetual (PPT) +2.97% the biggest gainers. On a forward P/E basis, the banks trade at 11.3x, a 35% discount to the average large cap industrial stock, the widest level in 20 years. And on a price/book ratio they trade on a 39% discount. This is just slightly higher than the last recession in 92, the one we had to have.

- REITS also proved positive with Mirvac (MGR) +1.63%, 360 Capital (TGP) +2.2% and Carindale Property (CDP) +3.73%.

- In resource stocks, energy shares fared well with Santos (STO) +4.23%, Woodside (WPL) +3.81% and Origin Energy (ORG) +5.47% showing a clean pair of heels. Beach Petroleum (BPT) +10.81% and AWE +9.09% together with Liquefied Natural Gas (LNG) +11.67% all look good for more gains on an oversold basis.

- Big miners were less enthused with RIO -1.24% and BHP +0.13% together with base metal stocks like Sandfire (SFR) -4.9%, Oz Minerals (OZL) -4.22% and goldie St Barbara (SBM) -14.02%.

- In industrials Healthcare stocks were in the out patient’s department, Sonic Healthcare (SHL) +4.45% and Mayne Pharma (MYX) +5.96% two standouts. Gaming stocks were good too, Tabcorp (TAH) +1.76%, Crown Resorts (CWN) +3.91% and Aristocrat Leisure (ALL) +2.04%. Media stocks also positive on hoped for media reforms Seven West Media (SWM) +4.4% and TEN +14.5%. Treasury Wine Estates (TWE) -5.17% fell after consideration of their profit upgrade on Friday. Qantas (QAN) -2.77% on higher fuel prices.

- Slater & Gordon (SGH) – A short covering rally helped drive SGH shares +18.64%.

- Speculative stock of the Day: Smart Parking (SPZ) +11.48%.

Corporate News

- Beach Energy (BPT) +10.81% has copped some serious flack over its decision to take a massive hit to its balance sheet at 4.30pm on a Friday before a ‘long’ weekend. $650m in asset write downs when no one was looking or so they had hoped.

- The ASX rival Chi-X has been sold to private equity house J C Flowers. The ASX rival now accounts for 20% share of the share trading volumes and made its first profit in the four years after opening.

- Challenger Financial (CGF) +5.99% announced early that its first half annualised profit will be around $185m when it reports in February. The company wanted to reassure punters following significant falls in January.

- Fantastic Holdings (FAN) -2.7% expects to report a sharp jump in half year profit on the back of strong sales growth. The company said its like-for-like sales rose 15.7% in the half year to December 27, likely boosting sales revenue to $270 million.

Economic News

- The NAB Business Conditions Index fell to +7 points over the period (from +10 in November), which is still above the long-run average of the survey (+5 points).

- Sydney has been ranked the second least affordable city to buy a home. Hong Kong is the winner where households have to spend 19 times their income to buy a home. Sydney requires a mere 12.2 times income to buy a home. This is up 2.4 points in the largest jump ever.

Surprisingly Tweed Heads was only just slightly behind San Francisco! Go figure.

Some facts on Australian property

In Asia today

- Japan’s annual trade deficit narrowed almost 80 % in December from a record as the cost of energy imports dipped and weakness in the yen spurred some gains in exports.

- Not long until Chinese New Year. Monday February 8th as we start the year of the Monkey. The Fire Monkey no less.

Europe

Brexit? What Brexit.

UK PM David Cameron has promised to hold a referendum on the UK membership of the EU by the end of 2017 with an early vote this year now almost a certainty.

This is the amount of discussion about what could be a defining moment in 2016. The possible exit from Europe of the UK. Seems that the Bank of England considers it a low risk event. That may change and with the current refugee crisis in Europe helping the exit case significantly.

Still in the UK, this week we should get a decision on whether HSBC stays in the city or moves overseas.

Happy Australia Day.

Back on Wednesday.

Ahead in Europe

- FTSE +35.50 points.

- DAX +223 points.

- CAC +130 points.

Clarence