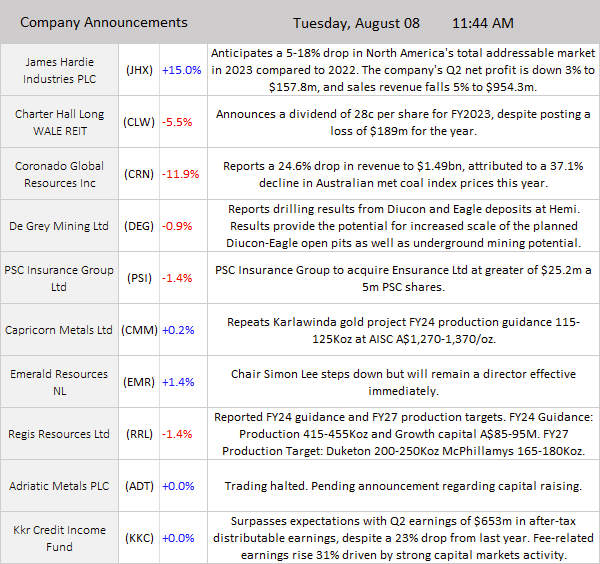

ASX 200 closed flat, up 2 points to 7311 (+-%), losing early morning gains, with mining and financials balancing the market. Iron ore giants were mixed FMG up 0.4%, BHP down 0.6%, and RIO off 0.4%. Goldman predicts a fall in iron ore prices this year. Iron ore futures in Singapore have fallen 11.6% from its cyclical high last month. The “big four” banks were mixed CBA and NAB in the green while ANZ and WBC stumbled. Big Bank Basket up to $177.19 (+0.1%). Lithium stocks were broadly lower, AKE down 2.5%, SYA tumbled -13.2%, while PLS rose 2.7% on broker upgrades. Gold stocks tracked bullion prices lower, NST down 2.3% and NCM off 0.5%. Tech stocks tracked the Nasdaq higher, XRO +0.2% and WTC up 0.2%, while SQ2 fell another 0.2%. Energy sector was buoyed by gains in WDS and COE as oil edged higher. Industrials under pressure, MTS down 1.1%, WOW off 0.2% and DMP falling 0.2%. Healthcare doing ok. Insurers, not so much IAG, MPL, and SUN all losing ground. REITs fell with SCG down 0.7% and VCX off 1.6%. In corporate news, WDS +0.6% after announcing that it will sell 10% of its flagship Scarborough gas project. JHX jumped 14.6% on upbeat forecasts despite posting a decline in revenue and profits. MYR fumbled the ball, down 14.1% on results despite raising profit outlook. CRN off 11.6% on drilling results. In economics, Consumer confidence fell 3.4 points to 75 despite the RBA cash rate pause. In contrast, Australia’s business mood improved slightly; NAB’s business confidence index rose to 2 in July from a downwardly revised -1last month. Australian building permits fell for the third time this year, falling 7.7%, MoM and China Exports dropped the most in over three years down 14.5% MoM, the steepest decline since Feb-20. Asian markets mixed, Japan up 0.3%, and HK down 1.8% with China off 0.3%. Dow Jones futures down 92 points, and Nasdaq futures down 76 points.

HIGHLIGHTS

- Winners: JHX, AZS, RED, BOE, REH, BFL, AQZ, 360

- Losers: MYR, SYA, CRN, LRS, CLW, FCL, RSG

- Positive sectors: Healthcare. Tech. Old skool platforms.

- Negative sectors: Base metals and lithium. Industrials.

- High 7342 Low 7311 Narrow range. Gains evaporate.

- Big Bank Basket: Drifts higher to 177.19 (0.15%)

- All-Tech index: Up 0.5%

- Gold steady at $2955

- Bitcoin: Steady at US29185

- Aussie Dollar: Steady at 65.46c

- 10-Year Yield: Back to 4.05%

- Asian markets: Japan up 0.2% HK down 1.4%, China unchanged.

- US Futures: Dow down 98 Nasdaq down 80

- European markets set to open down 0.4%

MAJOR MOVERS

- JHX +14.4% great results.

- AZS +7.1% continues to excite Andover fist.

- RED +5.7% KOTH guidance.

- REA +2.8% house price predictions?

- PLS +2.7% broker upgrades.

- RCE +14.8% patient updates.

- NXS +7.1% investor presentation.

- POS unchanged – another placement at 2c to raise $6m. Missed it yesterday.

- IVC – looks like deal done at 1270c

- MYR -14.1% trading update.

- CRN -11.6% results fail to impress, Coal price the issue.

- LRS -6.3% profit taking continues.

- ARU -3.5% run ends.

- RBL -14.3% burst.

- DLI -11.3% Mt Ida drilling update.

- A11 -8.9% Resource and exploration update.

- RAC -8.7% strategic update.

- SYA -13.3% slipping again.

- MSB -8.5% well and truly blasted.

- ABP -2.4% ASK +3.3% its complicated.

- Speculative Stock of the Day: Hawsons Iron (HIO) +16.7% – successful exploration program discovers mineable intersections of surface magnetite.

COMPANY NEWS

HEADLINES

- Consumer confidence dropped by 3.4 points to 75 despite the Reserve Bank’s cash rate pause, as per ANZ-Roy Morgan survey. Weak confidence below 80 points continued for a record 23 weeks; indebted homeowners exhibit lower confidence due to tight interest rates impacting finances.

.png)

- The WA government has scrapped the state’s controversial Aboriginal cultural heritage laws and promised a simpler system.

- More than one in 10 firms in the retail, hospitality and construction sectors are at risk of going bankrupt in the next 12 months according to research from credit company Illion.

- China’s exports fell for a third straight month in July. Overseas shipments dropped 14.5% in dollar terms last month from a year earlier, the worst decline since February 2020. Imports fall 12.4%, much deeper than economists expected.

.png)

- China’s exports to the U.S. plunged by 23.1% year-on-year in July, while those to the European Union fell by 20.6%. Chinese imports of crude oil dropped by 20.8% in July from a year ago, while imports of integrated circuits fell by nearly 17%.

- European markets set for a soft start. Down around 0.4%

- Zoom calls employees back to office after riding work from home wave.

- Tesla CFO and company veteran Zach Kirkhorn quits. Musk said he may require surgery and is planning to receive an MRI on his neck and upper back.

- The iPhone 15 is slated for sales launch around Sept. 22, Bloomberg reports.

- UK Retail sales record slowest growth in 11 months.

And finally….

Clarence