The ASX 200 finished at a three-week low down 56 pts at 8711 (0.6%). Broad-based losses again, Banks managed to hold firm, the Big Bank Basket flat at $289.43 (). CBA rose 0.9% and ANZ up 0.3%. Insurers eased, QBE dropped 1.2% and REITs also under pressure, GMG off 1.8% and SGP falling 2.2%. Tech and industrials also fell, WTC down 1.9% and XRO off 2.0% with the All-Tech Index down 1.6%. TLS succumbed to some profit taking, off 0.9%, WES continued to fall off another 2.1% with ALL falling hard. Healthcare remains in ICU with CSL dropping again, down 2.2% and COH falling 2.4%.4DX continued to unwind its gains, PME also fell. In resources, BHP fell 1.3% and gold miners were under pressure as bullion fell, EVN down 3.0% and NST off 2.9%. Lithium and rare earths found friends, LYC up 3.5% and PLS rising 3.0% as UBS upgraded the sector. Oil and gas also in demand, WDS up 0.8% and coal stock better together with uranium stocks better. PDN up 0.6% and WHC rising 3.9%.

In corporate news, RWC reaffirmed guidance rising 3.6% and DMP stuffed again off 10.7%, after the US parent dropped nearly 9% on disappointing numbers. ORG fell 3.9%, again after a downgrade following yesterday’s numbers.

On the economic front, the BoJ held rates at 0.75% with the Fed Meeting kicking off today.

Asian markets ease, Japan down 1.3%, China off 0.3% and HK off 1%.

US Futures ease, Nasdaq down 74. Dow up 2. Europe expected to open slightly higher.

HIGHLIGHTS

- Winners: ARU, ELV, AEL, ELS, NXL, MIN, LTR

- Losers: EIQ, PNR, DMP, SMI, DTR, WAF

- Positive Sectors: Banks. Oil and gas. Uranium. Rare earths. Critical metals.

- Negative Sectors: Gold miners. Tech. Healthcare. REITs. Industrials.

- ASX 200 Hi 8733 Lo 8693

- Big Bank Basket: Rises to $289.43(+0.3%)

- All-Tech Index: Eases 1.6%.

- Gold: Eases to $6454

- Bitcoin: Slips to US$76951

- 10-year yields: Drifts to 5.02%

- AUD: rises to 71.77c.

MARKET MOVERS

- ELV +6.3% lithium upgrades.

- ARU +7.3% rare earths going well.

- RWC +3.6% reaffirms guidance.

- LTR +4.0% keeps going higher.

- EUR +45.6% CRML takeover offer.

- HCH +6.2% copper back.

- FTI +19.6% Strategic placement

- EIQ -14.0% EchoSolv deployed into Mount Sinai.

- DTR -7.8% continues lower.

- PNR -11.3% quarterly report.

- DMP -10.7% stuffed crust.

- DXB -38.5% timeline pushed out.

- AI1 -24.5% profit taking.

- IVZ -15.6% bouncing around.

- Yesterday’s Hero: PAT -12%.

- Speculative Stock of the Day: 14D +133% – Now trading halt.

ECONOMIC AND OTHER NEWS

- Fed meeting kicks off. Powell’s last?

- Novartis results below expectations.

- China’s state planner has decreed that Meta Platforms Inc. must cancel its acquisition of AI startup Manus, a deal that was sealed four months prior.

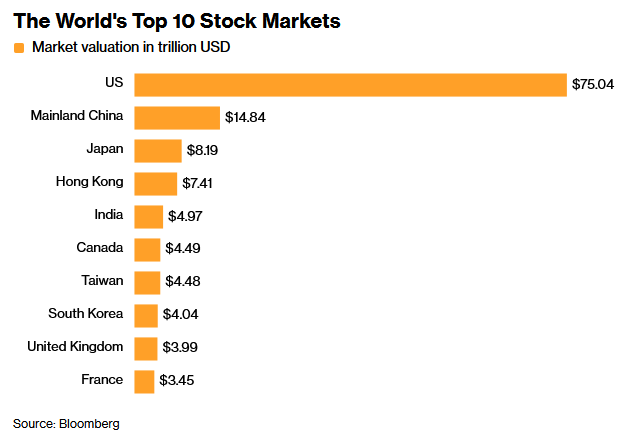

- South Korea now the eighth biggest stock market. Surpasses UK.

- China’s state planner has decreed that Meta Platforms Inc. must cancel its acquisition of AI startup Manus, a deal that was sealed four months prior.

- OpenAI recently failed to meet its own goals for new user acquisition and sales, fueling internal concerns that the company may struggle to support its astronomical spending on AI infrastructure.

- BoJ keeps rates on hold. The bank raised its core inflation forecasts to 2.8% from 1.9%.

- CATL plunges more than 8% as the Chinese battery maker unveils $5 billion share placement.

- European markets set to open slightly higher.

And finally….

I asked the surgeon if I could administer my own anesthesia. He said, “Sure. Knock yourself out.”

Clarence

XXXXX