The ASX 200 grinds out a 5-point gain to 7257 (0.1%) as banks gain and resources fold. ASX 200 up 0.5% for the week. Big iron ore and base metals were under pressure following LME price falls on disappointing Chinese numbers. BHP off 1.2% with RIO down 1.0%. Gold miners sold off too as bullion slid slightly and NCM extended the period of DD for Newmont falling 2.2%. Lithium stocks better though as LRS caught a gust of buying, up 21.4%, MIN gained 0.6% despite iron ore falls. PLS flat and IGO threw in the towel with MCR. Oil and gas stocks eased back on crude falls, Coal weaker too. Banks better as the Big Bank Basket rallied to $170.96(0.5%). MQG still struggling a little. Insurers floppy after QBE update on past disasters. Money managers better, AMP up 0.9% and MFG up 1.8%. Healthcare stocks the stand out with CSL up % and RMD running %. Industrials also in demand, WES up 0.8%, WOW up 0.2% and ALL up 0.4%. GMG and the REITs better and tech stocks in demand, WTC up 1.1% and the All-Tech Index up 0.9%. In corporate news, QBE disappointed, NWS rallied on its update, REA flat on slowing local economy and SHV cut its crop outlook falling 1.3%. Nothing on the economic front. Asian market mixed, Japan up 1.0% China down 1%. US futures positive.

HEADLINES

- Winners: LKE, GNC, LLL, NEU, CXO, NWS, GMD, CTT

- Losers: SBM, RMS, WGX, GRR, 29M, SFR, ADT

- Positive sectors: Banks. Healthcare. Tech. Defensives. Lithium.

- Negative sectors: Iron ore. Gold miners. Base metals.

- High 7257 Low 7234. Narrow range.

- ASX 200 up 0.5% for the week.

- Big Bank Basket: Bounces to $170.96 (0.5%)

- All-Tech index: Up 0.9%.

- Gold back up to $3001

- Bitcoin: Falls to US$28204

- Aussie Dollar: Steady at 66.96c

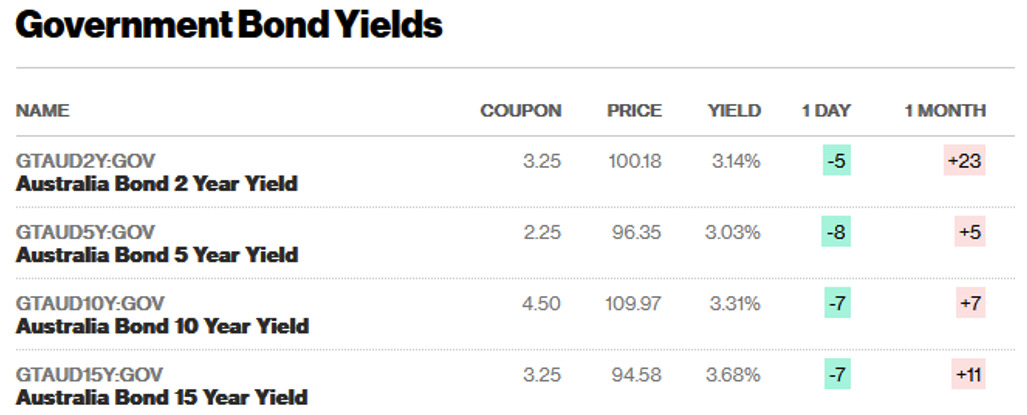

- 10-Year Yield: Falls to 3.31%.

- Asian markets: Japan up 1.0% China down 1% HK down 0.4%

- US Futures: Dow up 36 Nasdaq up 35

- European markets expected open higher. Eurovision beckons. UK GDP down 0.3% M/M.

MAJOR MOVERS

- LKE +13.04% LLL +5.65% lithium stocks in demand.

- NWS +4.68% quarterly update cheers.

- BRN +3.41% no reason really.

- NEU +5.09% back on the upward path.

- LTR +1.37% hits 300c.

- LRS +21.43% written up post conference.

- BTH +7.87% come alive.

- ZIP +8.00% HUM +7.14% SZL +10.08% onomatopoeia in fashion today.

- ADT -5.41% base metal falls.

- GRR -5.83% iron ore drops.

- PBH -3.91% runs out of bets.

- SLR -4.25% gold miners sell off.

- ALG -7.41% trading update.

- PAN -11.54% nickel on the nose.

- WGX -6.17% gold falls.

- BEZ -8.96% quarterly activities report.

- Speculative Stock of the Day: Nothing on any volume.

COMPANY NEWS

- QBE (QBE) -Raised its gross written premium (GWP) growth outlook to 10% for fiscal 2023, citing supportive interest rates. In Q1, GWP increased by 11%, with renewal rate increases averaging 10%, leading to a revised group combined operating ratio of 94.5%. The insurer also reported a net return of $384m and a rise in total investment funds under management to $29.1bn.

- News Corp (NWS) – Revenue in 3Q23 decreased by 2% to $2.45bn, due to challenging housing market conditions impacting the Digital Real Estate Services segment. Higher revenues from the Dow Jones segment and News Media and Subscription Video Services segments partially offset the decline. Net income and EBITDA also declined, but the company expects annualised savings of at least $160m from previously announced headcount reductions.

- REA Group (REA) – Revenue declined by 3% to $269m in Q3, missing revenue and cost forecasts. Weak economic conditions in Australia were cited as the reason, with earnings down 13% to $136m. The company expects higher costs ahead due to planned investment in its Indian unit.

- Medibank Private (MPL) – The Office of the Australian Information Commissioner (OAIC) is set to investigate a cybercrime complaint against Medibank, following a complaint lodged by Maurice Blackburn in November 2022. Medibank has confirmed that the OAIC is conducting its own investigation into the matter.

- Select Harvest (SHV) – Revised its 2023 crop forecast down to 17,500 metric tonnes, citing smaller volumes and lower crack-out rates due to climatic conditions. However, a decrease in the US almond crop has allowed the company to raise its net average pricing forecast range to $7.40-$7.80/kg, with the potential for further increases. Despite the challenges, Select Harvest expects a return to profitability with more normal weather conditions and the maturity profile of their almond trees.

- Chalice Mining Ltd (CHN) – Raised approximately $70m via a private placement at $7.30 per share and plans to raise up to $10m more through a Share Purchase Plan; the funds will be used to conduct exploration and pre-development activities for about 24 months.

- TechnologyOne (TNE) – Assures customers that they were not impacted by the recent cyberattack on its internal Microsoft 365 back-office system, as confirmed by independent security experts. Investigation ongoing.

- Ardent Leisure Group Ltd (ALG) – Provided an update on its trading performance for the period ending April 2023. ALG’s financial results significantly improved, recording a positive EBITDA result for the first time in six years.

- IGO has sold its $50.7m holding in Mincor (MCR) to Wyloo Resources.

ECONOMICS & OTHER NEWS

- The RBA has materially upgraded its assumptions regarding the so-called neutral cash rate, which it now believes is 3.8%. Crucially, that is in line with the current cash rate.

- China and Australia’s trade ministers will hold their first in-person talks since 2019. Don Farrell is currently in Beijing to meet Wang Wengtao

- Developed economies across the world are facing a debt problem, and that’s piling onto other headaches in the global economy as central banks continue to grapple with persistent inflation, according to World Bank President David Malpass.

ASIAN MARKETS

- China’s biggest domestic smartphone maker Zeku, is closing its chip design business as the global smartphone market extends a prolonged decline.

- Adani Enterprises, the flagship, as well as Adani Green Energy and Adani Transmission, may raise between $US3 billion and $US5 billion for a war chest to bolster the businesses.

- Taiwanese car battery maker bets on Northern France with €5.2bn plant.

US AND EUROPEAN HEADLINES

- European markets looking to open better.

- G7 Finance meeting in Japan.

- FDIC set to charge the big banks US$16bn over the next few years to bailout fund.

- NBCUniversal executive Linda Yaccarino is in talks to become Twitter’s chief executive officer, the Wall Street Journal reported. Musk said the company’s new CEO will start in about six weeks, without naming the individual.

- According to researchers at Imperial College London, wind turbines provided 32.4% of Britain’s electricity in the first three months of the year. That was the biggest slice with gas at 31.7%

- Elections in Turkey and Thailand this weekend.

- Eurovision song contest this weekend. Go Voyager.

And finally…..

Clarence

XXX