Today’s Headlines

- ASX 200 up 22 to 6084.5 as rally fades.

- 6100 proving serious resistance

- High 6110 Low 6076.

- Low volumes. Budget in focus.

- Banks mixed as miners rally. NAB sags.

- Industrials doing well with energy better.

- Brent Crude at a 4-year high.

- REH capital raising and acquisition.

- AUD weaker at 75.21c

- Bitcoin higher at US$9319

- US futures up 89

- Asian markets mixed with Japan down 0.04%, China CSI up 1.39%.

STOCK STUFF

Movers and Shakers

- CBA -0.07% Fitch negative outlook citing RC concerns.

- BLA -8.09% abandons guidance/board and management changes.

- AX1 +4.51% broker upgrade.

- KGN +5.78% rally continues.

- FAR +4.35% oil price helping.

- LOV +3.14% broker upgrade.

- WTC -1.71%% broker upgrade.

- ORI -6.36% results disappoint. Second half story.

- MFG -2.48% FUM outflows.

- MQG +1.93% broker upgrades following results.

- PDN -7.69% Noteholder consent received.

- SYD +0.85% $400m freight rail spend in the budget.

- BDR -16.67% capital raising.

- TLS +0.31% rally continues.

- SRX –0.75% trading halt. Another bid at the last pitched at 3360c cash.

- GFY -unchanged- trading halt on earnings downgrade.

- JBH -0.98% ASX has rap over the knuckles over disclosures.

- AMP -0.48% UBS downgrades to a sell.

- LYC +4.35% broker upgrade.

- WOW +0.35% Shaw downgrades to a sell

- PDL -6.51% fund managers under pressure.

- ALL +1.06% keeps on getting cherries.

- AGI -2.07% no jackpot here.

- Speculative stock of the day: No standouts today.

- Biggest risers – PNI, KGN, AX1, FAR, LYC and CUV.

- Biggest fallers – CVW, ORI, SYR, PDL, SPL and WGX.

TODAY

- Westpac (WBC) +0.82% Brian Hartzer said the outlook for Australia remains positive with GDP growth expected to be near trend at around 2.7% for the remainder of 2018 and 2019. “Australia is experiencing solid employment growth and continued business investment, especially in the construction sector. However, household income growth remains lacklustre and inflation is low. The Reserve Bank is likely to keep rates on hold for some time,” Hartzer said.

- Orica(ORI) -6.36% Lower first half in line with guidance. Strong demand for an improved second half in store. First-half statutory net loss after tax of $229m. Excluding individually significant items, net profit after tax for the first half was $124m, down 37% on the prior corresponding period (pcp). As previously advised on 1 March 2018, earnings were impacted by operational issues, with earnings before interest and tax (EBIT) of $252m for the half, down 20% on the pcp. The outlook for the second half of FY18 remains unchanged from the update released on 1 March 2018. The second half result will benefit from deferred contract renegotiations offset by lower forecast business initiatives. ORI expects the stronger run-rate from the second half of the 2018 financial year to continue into the 2019 financial year. Nothing to get too bullish about here.

- Reece(REH) – is launching a $560m raising to help fund an acquisition in the US of MORSCO. The acquisition will cost US$1.44bn. MORSCO is a leading US distributor of plumbing, waterworks and heating and cooling equipment (HVAC) products. The Equity Raising will be conducted at 930c per New Share (“Offer Price”), representing a 13.5% discount to the last traded price of 1075c on 4 May 2018. A 12.2% discount to TERP of 1059c (including placement). The Placement price will be determined by a bookbuild from the Offer Price.

- Newcrest (NCM) +1.25% announced to the market that it had received approval from the New South Wales (NSW) Department of Planning and Environment to use the first 200m of the old Cadia Hill open pit as a tailings storage facility. Newcrest began depositing tailings into the Cadia Hill open pit following the completion of the construction and commissioning work for the pipeline infrastructure. After a short ramp-up period, Newcrest expects Cadia to return to full production rates before the end of the current financial year

- Macquarie Group(MQG) +1.93 is looking to raise around $600m with the release of convertible notes. The notes will trade under the code MQGPC and have a margin of00% and 4.20%.

- Blue Sky Alternative Investments (BLA) -8.09% The company has ditched earnings forecasts completely and its CIO and is vowing to sell four of five businesses by June 30th. Chairman John Kain has also resigned together with Tim Wilson as a non-executive

- Sirtex(SRX) – The Scheme meeting (scheduled for today) has been postponed due to the new proposal form CDH on Friday. New all-cash bid at 3360c.

- Magellan Financial Group (MFG) –2.48% FUM grew 1.4% due to growth in global equities. There were net outflows of $268m which included net retail outflows of $64m and net institutional outflows of $204m

ECONOMIC NEWS

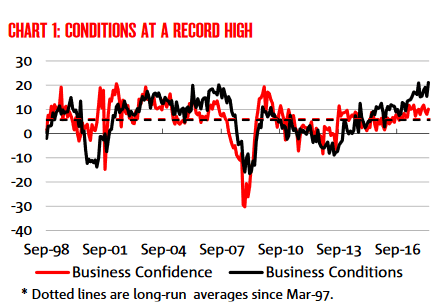

- NAB Business Confidence Surveyshows business conditions in April up 6pts to 21.

- Broad-based rises across the country but mining states recovering well.

- Expectations for more strength next month from NAB economist. WA and QLD offer some upside.

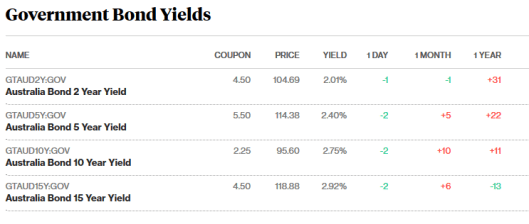

BOND MARKET UPDATE

ASIAN MARKETS NEWS

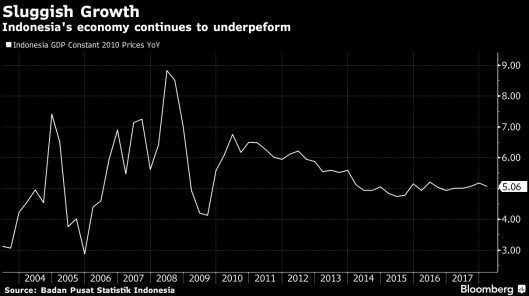

- Indonesian GDP rose 5.06% in the first quarter versus an estimate of 5.2%.

- China’s financial regulator stepped up its crackdown on industry malpractice, imposing a total 183 million yuan (US$29 million) of fines on three institutions for transgressions including lax lending practices and understating of risky assets.

EUROPE AND US MORNING HEADLINES

- Warren Buffett says bitcoin is ‘probably rat poison squared’

- Nestle and Starbucks to form a global coffee alliance. Nestle pays Starbucks US$7.15bn as part of the deal.

- Ping An Healthcare Technology slipped nearly 11% in HK today to below its offer price. It only listed last week.

- France’s credit outlook was raised to “positive” from “stable” by rating agency Moody’s.

- Wells Fargo has agreed to pay US$480m to settle a class-action lawsuit from the US bank’s shareholders over its bogus account scandal.

- UK Retailers are in their worst shape for nearly five years and the industry’s woes look set to deepen in the face of weak demand and soaring costs. The health of the retail industry dropped by one point to 79 during the first quarter, hitting its lowest level since 2013.

- May Day holiday in UK.

And finally………………..

An old guy in his Volvo is driving home after playing a terrible round of golf. The man is incensed and completely immersed in what went wrong with his round that he’s driving home simply out of habit with little regard for street signs, other drivers or pedestrians.

In the midst of going over his round over and over in his mind, his phone rings and his wife is on the line. The man clicks the speaker on his phone so as to not disturb his driving.

“Honey,” the golfer’s wife says in a worried voice, “be careful. There was a bit on the news just now, some lunatic is driving the wrong way down the freeway.”

“It’s worse than that,” the golfer says. “There are hundreds of them!”

She’s single… She lives right across the street and I can see her house from my kitchen window!

I watched as she got home from work this evening. I was surprised when she walked across the street, up my drive and knocked on the door!

I opened the door, she looked at me and said: “I’ve just got home, and I have this strong urge to go dancing and drinking, and maybe fool around a little….you know, have some fun. Are you doing anything tonight?”

I quickly replied: “Nope, I’m free!”

“Great!” she said. “Can you look after my dog ?”

Clarence

XXXX

If you want to listen to this report click https://w.soundcloud.com/player/?url=https%3A//api.soundcloud.com/tracks/440473413&color=%23ff5500&auto_play=false&hide_related=false&show_comments=true&show_user=true&show_reposts=false&show_teaser=true&visual=true“>here