Today’s Headlines

- ASX 200 outperforms as shorts cover but still down 53 points to 5838.

- High 5867 Low 5787.Good volume.

- ASX 200 drops 4.6% this week.

- Banking Royal Commission kicks off next week.

- Winter Olympics kicks off in Korea. Kim wins gold in skating on thin ice.

- US Government shut down.

- Miners lead losses. Banks hold up relatively.

- High PE stocks under pressure.

- AUD under pressure on RBA Governor speech 77.80c

- Bitcoin hold steady at US$7876

- AUD Bullion around $1690, one of the few winners.

- US futures finding support up 74 points.

- Asian markets crushed ahead of New Year China CSI drops 4.43% and Japan down 2.93%. HK down 3.18%

STOCK STUFF

Movers and Shakers

- AMP – unchanged- Broker reports mixed.

- TAH -4.41% unwinds equity swap.

- NAB +0.03% quality rises pays 7% yield

- EVN +4.49% ERM -2.60% high grade copper results

- RSG +3.77% SBM +0.55% Aussie gold producers in focus.

- UPD – 6.50% valuation concerns.

- APX – 4.27% tech valuations shrinking

- WTC – 7.09% High Pes suffering.

- NXT – 3.85% profit taking.

- ORG – 4.10% negative broker comments after write-down.

- AZJ – 0.22% withdraws Galilee Basin rail proposal.

- AYS – 2.57% finding support after horror day yesterday.

- BIG – 42.24% on AFR take down piece. Now Small. Moelis changes tune.

- WOR – 3.86% oil price weighs

- MND – 0.82% mining services slowing.

- CZZ -2.31% on no volume despite results of NPAT of $5.99m

- Speculative stock of the day: Classic Min (CLZ) +50.00% after high grade gold results at its Hannans – Forrestania project. CLZ owns 20% of project.

- Biggest risers – EVN, HSN, RSG, SBM, KDR and IEL

- Biggest fallers – MYR, UPD, BAL, WTC, APX and BPT.

TODAY

- Myer (MYR) -9.30% Yet another downgrade on a sales slide. A non-cash impairment charge to come too. The company says its underlying first half net profit will be between $37m to $41m. The company posted an interim net profit of $62.8m. CEO Richard Umbers blamed the poor sales in part to losing customers to its competition and to internet shopping.

- BHP -1.09% Two of BHP Billiton’s biggest institutional shareholders, BT Financial and Aberdeen Standard, have called for the company to respond to activist fund Elliott’s latest push to unify BHP’s dual London and Australian listings under an Australian umbrella, saying it appears to have merit.

- NewsCorp (NWS) – 0.59% Revenues up 3% to $2.18bn, above Reuters forecasts of $2.13bn. Led by growth in its digital real estate unit. Softness in their advertising business put pressure on the news and information services segment. NWS reported a net loss of $84 million, compared with a loss of $290 million, in the same period a year earlier. Results were also affected by US tax cuts.

- Specialty Fashion Group (SFH) +28.89%The former deputy CEO of Myer, fashion veteran Daniel Bracken, has been appointed the new chief executive. Results out too with underlying EBITDA up to $18.5m above forecasts of $14m-$17m. The company has also updated on the non-binding offer that has been made, saying That due diligence is ongoing.

- REA Group (REA) +2.04% first-half net profit fell by 55% to $132.4m due to the one-off gains last time on its sale of European Operations to Oakley Capital. Dividend 47c . Underlying profit — which strips out one-time items such as gains on asset sales — rose by 21% to $147.3m in the half-year period from $121.8m a year ago.

ECONOMIC NEWS

- ANZ no longer sees the Reserve Bank of Australia raising interest rates in 2018.

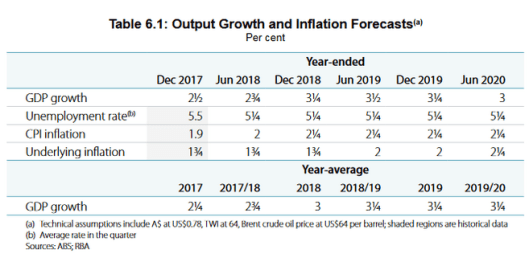

RBA Statement of Monetary Policy

Key Points:

- Inflation is likely to increase gradually over time, as the economy and labour market strengthen. Underlying inflation is expected to be around 2.25% by mid-2020. Quarterly forecasts largely unchanged.

- The labour market has been particularly strong. GDP growth picked up to2.75% over the year to the September quarter.

- GDP growth is expected to increase over the period ahead, to be a little above 3% over both 2018 and 2019.

- Trade weighted AUD has been in a narrow range.

- An appreciation of the AUD would dampen growth.

- Curbs in bank lending has cooled housing but household debt still high.

- Jobless estimates to be from 5.25% to 5.5%.

For the full statement click here

- The total value of dwelling commitments excluding alterations and additions (trend) fell 0.1% in December 2017 compared with November 2017 and the seasonally adjusted series fell 1.6% in December 2017.The total value of owner occupied housing commitments (trend) rose (up $29m, 0.1%) in December 2017.The seasonally adjusted series for the total value of owner occupied housing commitments fell 1.0% in December 2017. At the end of December 2017, the value of outstanding housing loans financed by Authorised Deposit-taking Institutions (ADIs) was $1,637b, up $8b (0.5%) from the November 2017 closing balance.

- Banking Royal Commission kicks off next week and the commission head is already focussing on the extraordinary profits banks make.

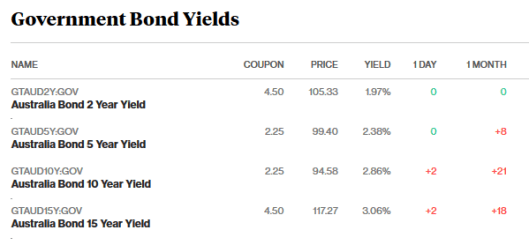

BOND MARKET UPDATE

ASIAN MARKETS

- Chinese markets rocked ahead of New Year. Year of the Dog. Seems appropriate. CSI down 4.86%.

- Japan rallies from initial falls down 3.22%

- In China.the producer price index rose 4.3% in January from a year earlier

- That matches projected 4.3% rise in a Bloomberg survey and 4.9% in December

- The consumer price index climbed 1.5%, the statistics bureau said Friday

EUROPE AND US MORNING HEADLINES

- US Government has shut down.

- Have we reached peak ‘Buy the Dips Mantra?

- Bear this in mind. Most millennial traders have never seen a crash.

- Twitter posts first profit as Trump tweets lift earnings.

- Jim Rogers says the next bear market will be a doozy. More catastrophic because of high debt levels. “Debt is everywhere, and it’s much, much higher now.” Bless.

- Here’s a contrarian view on Euro growth. Eurozone money supply figures have begun to flash early-warning signals of a sharp economic slowdown later this year. Janus Henderson says its key measure of money growth in the currency bloc – six-month real M1 – has seen the steepest drop since the onset of the Lehman crisis over recent month suggesting that the stronger euro and the gradual withdrawal of stimulus by the European Central Bank is starting to take a toll.

- The UK government is still ‘a million miles away’ from agreeing the UKs position on Brexit. Due to leave in 12 months. Coming? Ready or not.

And finally…hope you have survived a torrid week…time for a Chinese takeaway perhaps…

Chinese New Year kicks off in a week..The Year of the Dog…is that an Omen?

Clarence

XXX