Today’s Headlines

- ASX 200 fights back from early losses to close up 14 at 5891.

- High 5894 Low 5838.Volumes dropping off slightly.

- One Nation rules out tax cuts.

- Financials rally on NAB results. CBA still struggles.

- Miners take a hit on lower metal prices despite RIO results.

- Energy shares lower as WTI falls.

- TLS finds some friends.

- AUD steady at 78.26c

- Bitcoin rally continues up to US$8014.

- AUD Bullion around $1314

- US futures finding support down 55 points.

- Asian markets mixed with CSI 300 down 1.14% and Japan +0.29%.

STOCK STUFF

Movers and Shakers

- IEL +0.74% rally continues as brokers upgrade.

- CAR -2.48% broker downgrades after result.

- SWM +7.00% good bounce back.

- BKL +6.53% thin volume.

- DMP +3.88% short squeeze.

- AOG +2.79% EHE +1.53% running into class action.

- KGN +3.20% buyers chasing.

- BIG -6.73% continued profit taking.

- TAH -6.85% messy result and UK issues.

- WSA -3.77% metal price falls.

- ORE -2.60% GXY -3.12% lithium unwinds.

- MHJ -6.22% Market update

- SGH -9.03% company says share priced overvalued. Unusual. But right.

- HVN +3.97% shorts being squeezed a little.

- Speculative stock of the day: Blackham Resources (BLK) +22.00% record gold production of 6,498 oz up 19% and AISC reduced to $1,158 down 15%.

- Biggest risers – SGF, SWM, BKL, IRI, MMS and BGA.

- Biggest fallers – EWC, BIG, TAH, NGI, FXL and EHL.

TODAY

- National Australia Bank (NAB) +2.34% First quarter profit rose 3% from a year ago to $1.65bn. It was down 1% from previous quarter though. Expenses rose 4% and Net Interest Margins were down but no details provided which is a shame. Bad and doubtful debts fell 2.4% which helped the numbers. headwinds in housing and potentially higher interest rates. CET1 Ratio was up 1bps to 10.2% with a January 2020 deadline of 10.5% looking very achievable. Solid result but nothing really to get excited about. It is only 1Q and cost cutting remains a focus with the bank previously signalling some 6000 job losses although 2000 to be hired in the technology side of the business.

- Rio Tinto (RIO) -0.98% Announced a record full year dividend of $5.2bn and an additional share buy-back. Guidance of capex expected to be around $5.5bn in 2018 and $6.0bn in 2019 and 2020. Production guidance is unchanged. A good solid result. 69% of earnings are from iron ore but copper seems to be becoming a crucial part of the growth strategy.

- Tabcorp (TAH) -6.85% First half revenue up 19% to $1.4bn, net profit down 58% to $24.6m on the back of integration costs with former rival Tatts Group Ltd and write downs with its Sun Bets business in the UK. It expects $130m in annual EBITDA savings from the Tatts merger. Seems that WES is not the only company having issues with its UK expansion.

- Mirvac (MGR) +0.49% Reaffirmed FY earnings per share guidance of 15.3c to 15.6c. First half net profit was down 7% on year to $456m. The company said it remains confident in its ability to deliver operating earnings growth of around 6-8% in FY18. Chief Executive, Susan Lloyd-Hurwitz also unveiled plans to buy back up to 2.6% of Mirvac’s stock. It was up 2% yesterday.

- AGL –2.05% First half revenue up 7% to $6.45bn. Record net profit up 91% to $622m. Affirmed FY18 guidance for an up to 30% rise in underlying earnings this financial year. The stock was down 0.7% yesterday. Result maybe short of forecasts by Citigroup and Morgan Stanley, although JPMorgan said the numbers were “slightly better” than it was expecting. The company has reiterated guidance.

- BHP -1.37% has announced that it has completed a $350m upgrade to the smelter at Olympic Dam. 3000 short term jobs were created. The whole planned expansion is far bigger though at around $2.1bn.

ECONOMIC NEWS

- The NAB business conditions index rose 1 point, to +15 in the fourth quarter to a level the bank said was well above the long-run average.

- The NAB business confidence index eased slightly from +8 to +6 points in the quarter, a little above the average.

BOND MARKET UPDATE

ASIAN MARKETS

- Chinese January imports rise 30.2% forecasts was for around 5%.

- Exports rose 6.0% in January in yuan terms from a year earlier.

- The trade surplus stood at 135.8 billion yuan ($21.6 billion).

- Some of these numbers may have been affected by the upcoming Chinese Lunar New Year holidays.

EUROPE AND US MORNING HEADLINES

- World Bank chief says crypto currencies are Ponzi schemes.

- Dutch bank Rabobank has admitted flaws in its anti-money laundering defences were exploited by Mexican drug cartels.

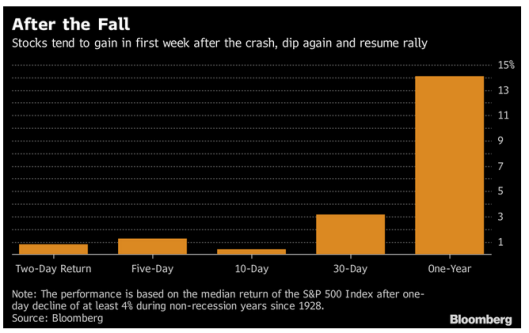

- Analysis by Bloomberg in 4% or above falls in the S&P 500 and subsequent performances suggest ultimately a return of 14% once the dust has settled. They have looked at the results from 1928 but have not included recession years.

- Tesla back in the news. And in orbit for a million years. Wonder what the warranty is like.

- Senate reaches deal. Now for Congress.

- Fed’s John Williams says US economy can handle higher rates.

And finally……………

Clarence

XXX