Juanuary…sounds so much more cosmopolitan!

ASX 200 misses the ‘Buy’ memo!

Today’s Headlines

- ASX 200 down 1 to 6014 after rally reverses.

- High 6035 Low 6014

- Jobs numbers strong again but headline rate weakens on more participants.

- Miners remain under pressure on production reports.

- Banks modestly higher in thin trade.

- Telcos recover TLS +1%

- AUD rallies then falls back to 79.61c on jobs number.

- Bitcoin $11,265

- US futures up 35 as rally continues. ASX didn’t get the memo

- Asian markets slightly positive with CSI 300 up 0.12% and Japan up 0.65%.

STOCK STUFF

Movers and Shakers

- GOR +6.99% Gruyere project update

- NWL +6.38% quarterly business update.

- GXY -6.63% PLS -5.63% lithium stocks under pressure again.

- WHC -6.18% Narrabri coal concerns.

- ICQ -9.26% selling appears.

- LVH -9.75% disappointing business update.

- WTC -3.71% profit taking.

- MYO -3.41% broker downgrade.

- ELD -4.53% technical selling.

- UPD -3.85% low volume selling.

- SRX +1.46% positive broker moves.

- SAR -3.41% disappointing quarterly yesterday

- Speculative stock of the day: AB1 +203.45% after a new gaming app Crazy Defense Heroes earns $200k in first week.

- Biggest risers – NWL, GOR, EWC, DCN and OMH

- Biggest fallers – GXY, WHC, PLS, SWM and ELD

TODAY

- BHP +0.13% Full-year production guidance maintained for oil, copper, iron ore and energy coal. Production guidance for Met coal reduced to between 41-43Mt as a result of ‘challenging’ conditions. The company has also warned that the recent US tax changes will result in an impairment charge. The changes relate to the deferred tax assets in the US, but the company has stressed that the tax changes will be very positive long-term. BHP will also take a charge to take into account $350m of write-offs at Escondida as a result of new concentrators. Like the tax charge, the new concentrator at the copper mine is already paying off with production 17% higher in the December quarter.

- Woodside (WPL) –0.77% Fourth quarter report showed higher QoQ sales of $939m and production of 21.9MMboe. The company also said it anticipated a significant increase in LNG production and a cash flow neutral price of $35 a barrel. Guidance is raised slightly to 85-90MMboe from 84.4MMboe.

- Livehire (LVH) –9.75% Quarterly update with Talent Community Connections (TCC) up 20% to 583,035. Not quite sure what TCCs are but there you go. Sounds like jargon for job seekers and employers. Cash receipts increased to $541k up 22%.

- Whitehaven Coal (WHC) –6.18% ROM coal production of 5.4Mt for the quarter and 11.2Mt for the half. Narrabri mine is transitioning at the moment with issues with the roof and a fault zone which is a negative given strong demand and strong prices currently.

- Alumina(AWC) –0.81% The ASX listed Alcoa holding company announced the Alcoa US 4Q results this morning. Fourth-quarter earnings rose though the profit missed analysts’ estimates amid higher costs for energy and raw materials and unfavourable movements in exchange rates. The fourth-quarter net loss was US$106c a share, compared with a loss of US68c a year earlier. Earnings excluding one-time items were US$104c a share. AWC is a 40% holder of the AWAC bauxite and alumina business. AWC had net debt of US$58.4m.

- Myer (MYR) -1.53% Some new management appointments and restructure announced today. Mark Crispey has been promoted to a new role of COO and Nigel Chadwick has been appointed CFO.

ECONOMIC NEWS

- Jobs numbers showed a 34700 increase in employment with the headline rate now 5.5% against consensus of 5.4%. Higher participation rate affects the headline. Strong jobs growth again above consensus and AUD pushing back towards 80c.

- Australian household debt to income ratio has now reached the 200% level. The increase was due to the Australian Bureau of Statistics revision to included self-managed superannuation debt. That resulted in a 3% increase in household debt from “extremely elevated levels”, and pushed the ratio to income to 199.7%

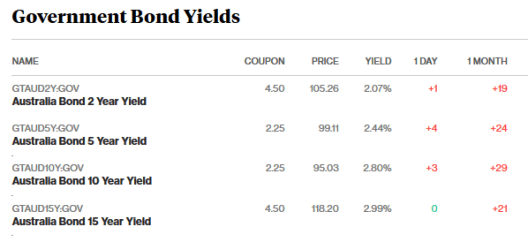

BOND MARKET

ASIAN NEWS

- In China new-home prices, excluding government-subsidised housing, in December rose in 57 of 70 cities tracked by the government, compared with 50 in November. Prices in major cities declined slightly or stayed mostly flat. Prices dropped 0.3% in Guangzhou and 0.2% in Shenzhen, edged up 0.3% in Shanghai and were unchanged in Beijing.

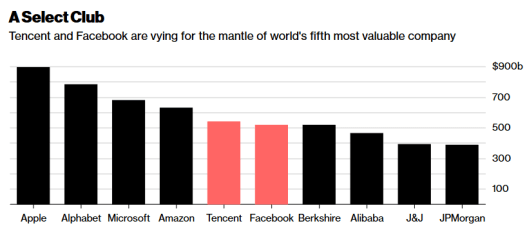

- Tencent is pulling away on the relative valuation from Facebook after FB announced changes to the way users see updates from friends rather than paid content.

- Bank of Korea holds key interest rate at 1.5%

EUROPE AND US MORNING HEADLINES

- The Bank of Canada, as expected, lifted the target for its overnight rate to 1.25 per cent, saying “recent data have been strong, inflation is close to target, and the economy is operating roughly at capacity”.

- Trump calls Apple’s money coming home a ‘huge win’ for US.

- Peugeot owner PSA will offer all of its models with an electric option by 2025, its CEO said.

- Chile’s SQM, one of the world’s largest producers of the battery material lithium, said it had resolved a long-running dispute with the government, striking an agreement to expand production to meet demand from electric cars.

- Hostilities have broken out in GKN with Melrose launching a GBP7.4bn takeover offer for the 259-year old GKN. The bid at 430.1p is the biggest hostile takeover for a FTSE 100 company since Kraft bought Cadbury in 2009.

And finally…..thanks to David for this gem…

My friend Dave recently moved to a farm near Dubbo.

His new neighbour Fred visited, and as a way of welcoming Dave, invited him to a party that night.

But Fred warned his parties were pretty wild: “…There’ll be some drinking…There’ll be some fighting…And there’ll be some fornicating.”

Dave was surprised, but was up for it. “OK! What time do I arrive” Dave asked.

Fred replied “Oh, anytime – it’s just the two of us.”

Clarence

XXXX