Ho! Ho! Ho!…

Twas the night before Clarence leaves for colder climes!!!

Today’s Headlines

- ASX 200 down 10.5 to 6011.

- High 6043 Low 6021

- MYR slumps on sales numbers.

- CBA shrugs off new AUSTRAC charges. For now.

- ACCC knocks back WOW/BP deal.

- WFD under pressure.

- Gold bounces on weaker USD.

- AUD jumps on Jobs data to 76.65c.

- Yellen calls Bitcoin ‘highly speculative’. Falls to $16,400

- US futures up 22.

- Asian markets weaker with China CSI 300 down 0.35% and Nikkei down 0.41%

STOCK STUFF

Movers and Shakers

- KDR +10.69% lithium stocks continue higher.

- PFP +0.85% broker upgrades.

- CTX +3.73% benefits from WOW/BP ACCC decision.

- WHC +4.87% broker upgrades

- MYR -9.66% ‘shock’ sales slump. Not much of a shock.

- WOW -0.63% ACCC decision.

- IGO +6.47% Deutsche becoming a substantial holder.

- CBA +0.16% AUSTRAC investigation.

- CIM +2.08% further share buy backs.

- EN1 +25.00% new float debuts.

- WTC -1.55% founder sells 2%

- TTS gone as TAH takeover finally complete.

- THC -12.66% placement at 63c.

- TLS -1.34% PM’s NBN comments weighing perhaps.

- NSR -1.89% completes placement.

- Speculative stock of the day: Anson (ASN) +30.14% on track to produce first lithium carbonate in April 2018. Discussions are also underway with battery manufacturers to test product. Drilling next year.

- Biggest risers – CIA, KDR, IGO, SIQ, RSG and WHC

- Biggest fallers – MYR, HUB, SKT, MSB and IEL.

TODAY

- Mineral Resources (MIN) +3.47% has updated the market on the AWE +% takeover approach. MIN states that acquiring gas assets with a WA focus is a logical and highly value accretive addition to its portfolio. The Waitsia II gas field is the attraction for both MIN and CERCG. More to play out in the AWE bid. The company has re-confirmed FY18 guidance which it announced at the recent AGM. It also confirmed there had been no adverse changes to either mining services or the commodity business.

- A2 Milk (A2M) +3.30% MD and CEO succession plans with Ms Jayne Hrdlicka replacing retiring Geoffrey Babidge. Jayne will take over at the start of 2019 with Babidge available until then.

- Monadelphous (MND) +2.979 New maintenance contract worth $110m secured. Three-year contracts for Dalrymnple Bay Coal Terminal, Muja Power Station and Mount Arthur.

- Woolworths (WOW) –0.63% The ACCC will oppose the acquisition of the service stations by BP. WOW currently has 531 sites and this will be a negative for the share price.

- Myer (MYR) –9.66% Hardly a surprise to anyone but the company has updated sales for the Q2 with a subdued performance and a profit shortfall. Total sales are down 2.3% in November despite a bigger marketing spend. Sales during the first two weeks in December have weakened further and were down 5%.

- Wisetech (WTC) –1.55% The CEO has sold 2% of his holding or around 5.8m shares to improve liquidity. The CEO, Richard White has said recently that he would sell some if it helped liquidity issues.

ECONOMIC NEWS

- The 61,600 rise in employment in November was well above the consensus forecast (+19,000) and much stronger than the 7,800 increase in October. 41,900 full-time jobs created. The unemployment rate held steady at a five-year low of 5.4%. The participation rate reached 65.5% compared to 65.1% a month ago.

- ANZ has downgraded its outlook for the housing market in 2018 and now expects capital city house prices to rise just 1.5%.

- Net Overseas Migration (NOM) to Australia increases 27% to 245,400.

- New South Wales was the most popular destination, with NOM of 98,600 and Victoria followed, with 86,900

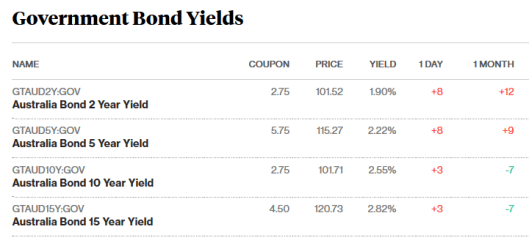

BOND MARKET

ASIAN NEWS

- The PBOC has raised rates by 25bps to 2.5% after the Fed raised US rates.

- China’s fixed-asset investment growth slowed to 7.2% in the January-November period, the National Bureau of Statistics said.

- Fixed-asset investment by state firms rose 11.0% in January-November, quickening from 10.9%in the first ten months.

- Growth of private investment slowed to 5.7% from 5.8% in January-October.

- Industrial output rose 6.1%.

- Retail sales gained 10.2% in November on-year, meeting expectations.

- Singles Day sales hit $38.25bn, more than the combined revenue for Black Friday and Cyber Monday in the United States.

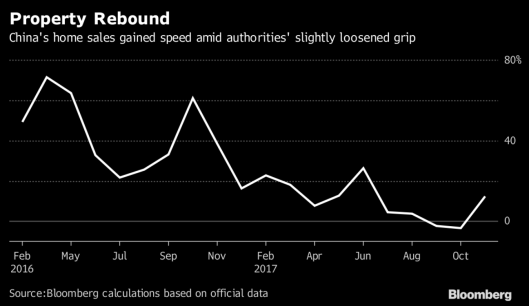

- New home sales grew 12.4% in value in November from a year earlier.

- Toyota is considering making batteries for electric vehicles (EV) with Panasonic. Car company president Akio Toyoda said the automaker’s annual sales target for petrol-electric and plug-in hybrids is 4.5m vehicles by 2030, and 1.0m units for EVs and FCVs. Panasonic is the world’s biggest supplier of batteries for plug-in hybrids and EVs.

EUROPE AND US MORNING HEADLINES

- Murdoch and his family will hold a stake in Walt Disney of less than 5% following the planned $US60bn sale of 21st Century Fox entertainment assets to the media company.

- Theresa May suffers defeat in major set back for Tory party and Brexit.

- The Italian Energy authority is probing 100 companies for market behaviour with two energy providers liquidating, forcing companies to find new suppliers. Power companies appear to have been withholding power and the benefitting from price spikes when state owned Terna stepped in to cover blackouts. Not the only ones with energy problems it seems.

And finally thank you for all your support this year..have a Jolly Xmas and a Brilliant New Year.

Back in 2018 with more market round ups…

In the meantime stay safe and party like its 1999!

Clarence

XXXX