Today’s Headlines

- ASX 200 falls 41 pts to 5970 on Royal Commission.

- High 6003 Low 5949.

- Bank switching after government backflip.

- CBA seen as the risk.

- Miners struggle on lower metal prices.

- Defensives find buyers.

- AUD steady at 75.85c on capital data.

- Bitcoin recovers to $10600 after 20% fall.

- US futures up 14.

- Asian markets easier as tech sell off continues. CSI 300 down 0.55%. HK down 1.28% but Japan down 0.02%

STOCK STUFF

- LVH +10.58% gaining fans.

- LYCDA -1.46% first day trading after consolidation.

- AWE +22.94% up on Chinese state company bid at 71c.

- FMG -0.43% appoints two women to run the company.

- ORL – Goes into administration.

- APX +22.47% returns after positive capital raising and acquisitions.

- EHL +4.00% completion of acquisition.

- CCL +2.32% defensive buying.

- MYR +6.08% stirring.

- RFG +2.97% AGM positive.

- KDR -3.64% profit taking.

- JIN +5.06% positive outcome from TAH/TTS CrownBet talks.

- WTC -3.65% director selling take wind out of sales.

- BPT +1.94% finding buyers after AWE bid.

- TLS +1.18% yield investors chase on bank falls.

- EUR +20.00% Insider leader continues rally.

- Speculative stock of the day: Love Group (LVE) +39.53% after a presentation to shareholders on matchmaking site global potential.

- Biggest risers – APX, VRL, MYR, SLC, WGX and RFG.

- Biggest fallers – ALL, ASL, CLQ, AWC and IGO.

TODAY

- Aristocrat (ALL) –6.82% The company has delivered a strong performance with EDITDA up 24.2% to $1001.2m. EPS up 36.2c. Final dividend of 20c fully franked. Outlook is continued growth in FY18. Investors will like that. The company has also announced a strategic acquisition of a social media gaming company Big Fish for US$990m. This will transform ALL into the #2 social casino owner by revenue.

- Tabcorp (TAH) -unchanged- has entered an agreement with Crown Resorts (CWN) -1.36% for CWN not to oppose the merger with TTS. In return TAH has agreed to supply a digital stream of SKY 1 and 2 to CrownBet for betting customers. This is a good move for TAH and the TTS merger.

- AWE +22.94% The company has received another indicative proposal from China Energy Reserve (CEROG) for the company at 71c. This is not the first time the company has been bid for with the last one failing to get up at around 80c. An interesting move from a Chinese state run company. That is now both STO and AWE under siege from predators. Who is next?

- Oroton Group (ORL) – The company has been placed into administration and suspended from the exchange. Another retail casualty. Hardly a surprise just surprising that high profile fund manager Will Vicars from Caledonia still has around 18% of the company.

- Fortescue Metals (FMG) –0.43% Finally the company has announced its Core Leadership Team (CLT) with Elizabeth Gaines being promoted to CEO to replace Nev Power. Ian Wells becomes CFO, Julie Shuttleworth becomes deputy CEO and Greg Lilleyman is COO.

ECONOMIC NEWS

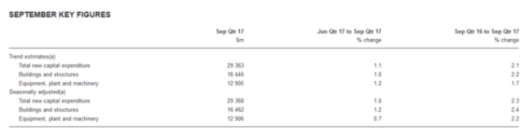

- Private Capital Expenditure has risen 1.0% in September.

- The trend volume estimate for total new capital expenditure rose by 1.1% in the September quarter 2017 while the seasonally adjusted estimate rose by 1.0%.

- The trend volume estimate for buildings and structures rose by 1.0% in the September quarter 2017 while the seasonally adjusted estimate rose by 1.2%.

- The trend volume estimate for equipment, plant and machinery rose by 1.2% in the September quarter 2017 while the seasonally adjusted estimate rose by 0.7%.

- Dwelling approvals rise 0.7%.

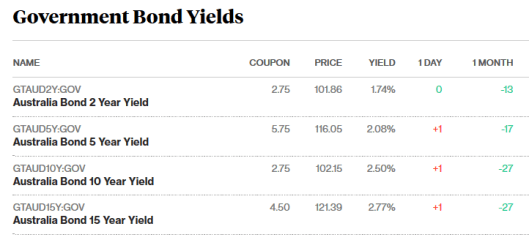

BOND MARKET

ASIAN MARKETS

- Tech stocks continue to sell off in Asia. FANGs for the memories.

- The official Purchasing Managers’ Index (PMI) released on Thursday stood at 51.8 in November, compared with 51.6 in October. Growth in China’s manufacturing sector picked up in November, despite a crackdown on air pollution and a cooling property market.

- Economists see fourth-quarter economic growth moderating to around 6.6%, and slowing further to 6.4% in 2018, as borrowing costs rise and the boost from earlier infrastructure projects begins to fade.

- New manufacturing orders picked up to 53.6 from 52.9

- New export orders increased to 50.8 from 50.1

- The steel industry PMI rose to 53.1 from 52.3

- The Bank of Korea has raised interest rates for the first time in more than six years, heralding a tightening cycle on the back of the country’s export-driven economic recovery.

- Japan’s industrial production returned to growth in October but grew at a slower pace than forecast. YoY grew at 2.5%.

EUROPE AND US MORNING HEADLINES

- US calls on China to stop oil supplies to North Korea and warns if it comes to war ‘regime will be utterly destroyed’.

- UK consumer confidence has fallen to -12. Consumers shunning major purchases. All five measures used by GfK to calculate the score declined, with the willingness of consumers to make major purchases posting the biggest drop.

- Poor old Theresa May now being attacked by Trump Tweets as the UK tries to justify the divorce payment to the EU.

- Sterling having a decent run as Brexit fears ease.

- Rooney hits three against West Ham.

- US Tax cuts in the spotlight but maybe 22% not 20%.

- UK is building an $140m battery research base in Coventry. The National Battery Manufacturing Development Facility (NBMDF) will bring together academics and businesses to work on new forms and designs of batteries, as well as their chemistry and components.

And finally….

Negotiations between union members and their employer were at an impasse. The union denied that their workers were flagrantly abusing the sick-leave provisions set out by their contract.

One morning at the bargaining table, the company’s chief negotiator held aloft the morning edition of the newspaper, “This man,” he announced, “called in sick yesterday!”

There on the sports page, was a photo of the supposedly ill employee, who had just won a local golf tournament with an excellent score.

A union negotiator broke the silence in the room.

“Wow!” he said. “Just think of the score he could have had if he wasn’t sick!”

Clarence

XXXX