Today’s Headlines

- ASX 200 slips 4 to 5983 after weak start finds support..

- High 5984 Low 5951 Quiet session boosted by options expiry volume.

- ASX 200 up 16 points for the week.

- Asian markets weighing on sentiment.

- Queensland election tomorrow.

- Banks again seeing negative sentiment.

- Big miners cautious despite commodity rises.

- US markets back open briefly tonight.

- Where is Amazon?

- China cuts import tariffs on dairy and alcohol.

- Iron ore jumps again by nearly 4% after 16% this month.

- AUD bounces to 76.21c as USD fades post FOMC.

- Bitcoin falls to US$8084.

- US futures up 35.

- Asian markets failing to recover from recent large losses. China CSI 300 down 0.81% and Japan down 0.05%. HK though still positive up 0.32%

STOCK STUFF

Movers and Shakers

- PNI +5.48% after snagging star MacBank fund managers.

- ASB +9.85% wins ship building contract from RAN

- BIG -7.47% starting to unwind.

- TLS +% finally a positive day.

- RSG +3.43% gold hedging in pace at $1712.

- ACX +6.42% short squeeze continues.

- NCK -5.26% on thin volume.

- MIN +7.89% enjoying the iron ore price rise. AGM comments helping too.

- MVF -18.06% AGM presentation. Low cost providers making life tough.

- MYR +1.41% AGM. First strike and Lew fails.

- PMV +0.07% Solly fires back. Not happy Jan.

- WEB -3.17% fall out from downgrade continues.

- 4DS +19.57% after presentation to shareholders.

- CAN -8.42% cannabis stocks smoked.

- THC -5.47% rolled.

- Speculative stock of the day: Missed one Northern Cobalt (N27) +41.00% following a presentation at the AGM on the outlook for cobalt and their project in NT.

- Biggest risers – ASB, MIN, HSN, PNI, ACX and RSG.

- Biggest fallers – BIG, NHC, NCK, RWC, LNK and MOE.

TODAY

- Primary Healthcare (PRY) +0.29% has warned there is a shortage of GPs and recruitment is an issue. The PRY medical centres division is suffering from a margin decline as the company moved through the accounting and commercial impacts of transitioning GPs onto new contracts. The company told shareholders at its AGM that underlying net profit after tax for the year was forecast to be in the range of $92m to $97m, with the second half’s trading likely to be stronger than the first half. It compares to last year’s profit of $92m.

- ACCC said today it is proposing to re-authorise for a further five years, coordination involving three Asian based Jetstar branded joint ventures: Jetstar Asia, Jetstar Pacific, and Jetstar Japan. Jetstar also wants to coordinate with shareholding airlines – Qantas, Japan Airlines and Vietnam Airlines.

- Rio Tinto (RIO) +0.12% Announced this morning its plans to extend its Channar Mining JV with Sinosteel. This is the third extension of the JV which will see an additional 10m tonnes of iron ore delived from WA.

- Syrah Resources (SYR) – unchanged- Announced it has reached its first production milestone at its Balama Mine.

- Ten Network Holdings (TEN) – last day on the ASX today. It is to be removed from the official list after market close following the acquisition by CBS International Television Australia.

- Crown Resorts (CWN) – 0.64% The company has responded to media speculation regarding consolidation in the sector and has admitted it is in discussions concerning its 62% interest in Crown Bets.

- Myer (MYR) +1.41% AGM today with the company announcing no improvement in trading in Q2 compared to Q1. Q2 is the Xmas period and have said the impact of Amazon is unknown. Q1 sales were $699m down 2.8%. Comparable sales down 2.1%.

ECONOMIC NEWS

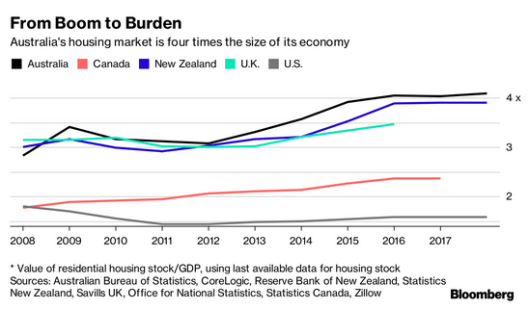

- The market value of the nation’s homes has ballooned to $7.3trillion in the last five years.

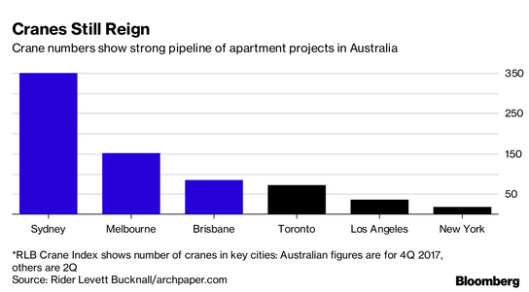

- And the cranes still have it. Certainly, Sydney is a building site and with a $2.5bn upgrade to stadia in the city there looks like more to come.

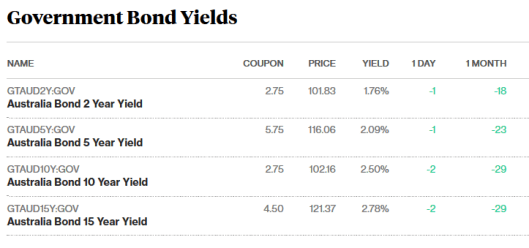

BOND MARKET

ASIAN MARKETS

- Plenty of important stuff happening in China post party convention. China’s Finance Ministry has said it will reduce import tariffs on a selection of consumer goods from the beginning of December.

- Profit margins at Chinese banks will be squeezed next year and credit growth is likely to slow as increasing regulation eats up capital, Fitch Ratings said.

- Chinese regulators are sweeping through the country’s US$40 trillion financial sector in a bid to contain risk after total debt ballooned to about 260% of the size of the economy. In the past week alone, they’ve proposed rules governing returns from asset-management products, laid out limits on bank shareholdings and unveiled a purge of cash micro-lenders. No wonder the stock market has taken a bit of a hit this week.

- Analysts said investors are concerned about a slump in China’s bond market spilling into equities as authorities step up a campaign to reduce leverage. The government’s message that Kweichow Moutai Co. shares were rising too fast has also sent ripples across the market

- Mitsubishi Materials sank on Friday a day after the company admitted its subsidiaries falsified data about products used in crucial parts of aircraft and cars.

EUROPE AND US MORNING HEADLINES

- Barmy Army may have something to sing about at the Gabba.

- Compare the Market has secured an investment from Canada’s largest pension fund valuing it at £2.25bn, around the level it had been expected to obtain on the public markets before it delayed its planned listing in September.

- Eurozone PMI at 17-month high as Europe powers ahead. Business is booming best survey for 6 years.

And finally………..

Clarence

XXX