Today’s Headlines

- ASX 200 slips 0.2 to 5986 with miners in demand.

- High 5991 Low 5971 Thin markets, low volume.

- Amazon softly softly launches (maybe).

- BHP and miners leading the rises.

- Banks under pressure early as calls for inquiry grow.

- Big bank basket falls to $171.

- Iron and coal rally strongly in Asia.

- AUD bounces to 76.21c as USD fades post FOMC.

- Bitcoin US$8244 in relative quiet trade.

- US futures up 13.

- Asian markets mixed with China CSI 300 down 1.10%. Japan closed for a holiday, Hang Seng up 0.24%

STOCK STUFF

Movers and Shakers

- CCL -4.89% lowest in ten years as price cuts weigh.

- AHG +6.94% after selling refrigerated business.

- ELD +2.81% broker upgrades.

- EVN +2.39% business update.

- WEB -6.67% broker downgrades and CBA selling.

- HUB +2.96% buyers still chasing.

- A2M -4.16% too close to the sun and broker downgrades.

- TRS -1.10% broker report.

- BIG -2.15% profit taking.

- FLT -2.60% catching the WEB disease.

- CAN -5.86% profit taking.

- WHA -7.89% bubble bursting.

- CSL +0.70% still the one.

- MDC +9.79% positive announcement.

- SWF -20.00% after IPO fails to fire.

- Speculative stock of the day: MYQ +40.98% after the recent announcement on patent protection for its IP in Australia. MYQ has a smart phone app for body imagining to better track personal goals targeting weight loss or muscle gain.

- Biggest risers – ZIM, AHG, YAL, PSI, PME and MOE

- Biggest fallers –WEB, CCL, A2M, APT, CTD and BAL.

TODAY

- Isentia (ISD) +4.69% AGM commentary today. King Content exit will be completed by the end of the year and revenue has stabilised with revenue around previous guidance of $133m-$135m and EBITDA of $32m-$36m.

- Automotive Holdings (AHG) +6.94% The company is selling its refrigerated logistics business to HNA International for $400m. This follows an unsolicited offer from HNA. $280m in cash and an assumption of $120m in lease liabilities.

- Phoslock (PHK) -5.13% Forecasting revenue of $22m as the company transforms and turns to China. The board is currently projecting revenue of $40m for FY19.

- Evolution Mining (EVN) +2.39% Business update with cash generation reducing debt and gearing. YTD EBITDA margin of 54% Net Debt reduced to $282m. AISC of $739. Net cash flow $67.6m. New COO has been appointed in Bob Fulkner after Mark Le Messurier departs at year end.

- Woolworths (WOW) +0.38% Sales performance has remained positive Australian Food sales up 4.9%. Dan Murphys up 3.3% BIG W up 2.9%. Continued improvement in fresh food store format. BIG W is turning around which is a relief and the signs are good.

- Coca Cola (CCL) –4.89% A $40 million investment to accelerate growth in Australian beverages will take a toll on earnings in 2018. The company is cutting prices to help grow its market share of products outside of carbonated drinks. The company is looking to focus on tea, juice and other areas where they are currently underweight.

- Thorn Group (TGA) –9.77% Write off of $20.7m in goodwill on Radio Rentals and Trade and Debt Finance.

- Primary Healthcare (PRY) –1.69% AGM today – Outlook looks to be a little disappointing and the company is talking about mixed results. GP Recruitment is softer than expected and the company is focussed on reduction in rental for its pathology and imagining business. Net profits are expected to be $92m -$97m with a skew to the second half.

- Tabcorp (TAH) -1.41% Tatts Group (TTS) –1.14% The ACT has now published its recommendation that the scheme to merge is allowed and will bring substantial benefits to the two groups. As a result, the companies involved have postponed the AGM and Scheme meeting to take this into account and send out additional information to shareholders. The AGM is now set for 12th December.

ECONOMIC NEWS

- Scott Morrison has summoned bank chiefs for a grilling as the calls for a Royal Commission grow. He met with Westpac chairman Lindsay Maxsted, Commonwealth Bank chair Catherine Livingstone, ANZ Bank chair David Gonski and National Australia Bank chairman Ken Henry in Sydney today. Sure they were trembling.

BOND MARKET

ASIAN MARKETS

- Singaporean GDP grew at its fastest pace in three years.

EUROPE AND US MORNING HEADLINES

- Thanksgiving Holiday in US. The Turkey index is down 6.7% this year. At Walmart the cost of a traditional Thanksgiving is US$54.84 whilst at Aldi it is US$41.19 down 2.6%

- Billionaire Peter Thiel sold 73% of his stake in Facebook this week. Thiel, a member of the board, sold 160,805 shares for US$29 million, according to a regulatory filing this week.

- Larry Hatheway, the head of investment solutions at GAM, says his two biggest concerns right now are China and inflation. And the Spanish Inquisition.

- In the UK Chancellor Hammond has pledged to fix the UK housing market abolishing stamp duty on first time buyers paying up to GBP300,000.

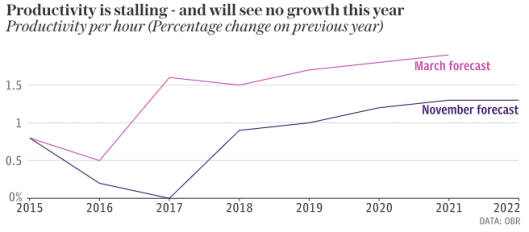

- Meanwhile the UK economy will grow by an average of just 1.4% across each of the five years ahead, down from the 1.8% average forecast by the Office for Budget Responsibility (OBR) in March. Poor productivity growth is the main reason.

- Some trivia to contemplate about behemoth Alibaba. It accounts for 75% of China’s retail sales. 731m Chinese are now online. it is now ranked among the world’s top 10 companies in terms of market value. And the shopping platform is doing some shopping of its own.

- “5% of the increase in stock market value (US$250 billion), and 7.5 times our monthly trade deficit with China has gone to one Chinese company.” According to a tweet from Mark Cuban to President Trump. And we think Amazon is a threat.

And finally…first day of Ashes…go England!

Clarence

XXXX