Not a good way to finish the week!!

The day the market died???

Today’s Headlines

- ASX 200 down 82 to 5703 on broad based selling of banks and USD earners.

- Top to bottom of the range in a day. High 5779 Low 5693.

- Weekly loss of 20 points. Increased volatility a focus.

- US tech sell off hurting sentiment.

- Banks slide 1.5% to 2% on profit taking. Resources give back ground.

- Bond proxies weaker.

- FMG rallies despite sector woes.

- Healthcare takes a hit.

- Telcos buck selling on defensive nature.

- Consumer and gaming stocks sold down. DMP falls over 3%

- US healthcare act fails to pass Senate. No repeal of Obamacare.

- AUD slips to 79.67c.

- US Futures down 46.

- Asian markets mixed with Japan down 0.66% China up 0.16%.

STOCK STUFF

- BKW +2.79% on trading update and WA consolidation.

- TLS -0.24% finding a little support.

- BWX -7.62% drops on more profit taking. Beef woes highlight China risk.

- A2M -3.33% Goldman Sachs sells down holding.

- FMG +3.44% cost cutting and production report.

- WEB -6.87% at odds with auditors.

- KGN +7.14% after insurance deal yesterday.

- AWE -5.00% disappointing quarterly.

- LOV +4.06% in thin trade.

- BHP -1.25% no restart expected this year for Samarco.

- HVN +0.93% short covering continues

- Biggest risers – NHC, FMG, BAL, BKW, LYC and FNP.

- Biggest fallers –WEB, OGC, BWX, AHY, A2M and MYX.

TODAY

- Webjet (WEB) –6.87% The company has announced it is having some issues with its auditor on the accounting treatment of the Thomas Cook acquisition. Despite 2 of the big four accountancy firms agreeing with WEB the auditor BDO disagrees and so the accounts will be qualified.

- Origin Energy (ORG) -0.87% and ConocoPhillips have successfully completed performance testing at their APLNG gas export project in Queensland.

- Downer EDI (DOW) -2.18% has secured 74.5% of Spotless, bringing the contactor close to the crucial 75% mark that enables it to attempt to delist the services group.

ECONOMIC NEWS

- The quarterly producer price index (PPI) rose 0.6% in April-June, following a 0.5% increase the previous quarter, the ABS reported. The median estimate was a gain of 0.6%.

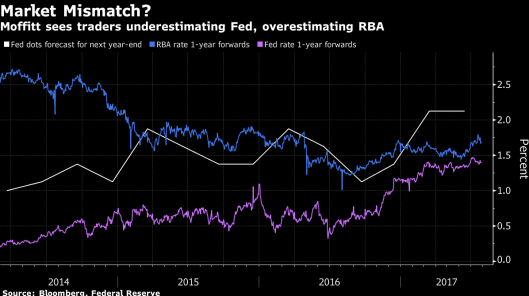

- Goldman Sachs Asset Management is calling the top of the AUD rally. It sees unrealistic expectations of RBA rate rises.

BOND MARKET UPDATE

ASIAN NEWS

- Core consumer prices, which exclude fresh food, increased 0.4% in June from a year earlier (estimate +0.4%).

- Excluding fresh food and energy, prices were unchanged (estimate -0.1%).

- The unemployment rate fell to 2.8 % (estimate 3%).

- Household spending rose 2.3% from a year ago (estimate +0.5%), its first gain in more than a year.

EUROPE AND US MORNING Headlines

- Corporate results due Friday include Credit Suisse Group AG, Nomura Holdings Inc., Exxon Mobil Corp., and Barclays Plc.

- With just under half of S&P 500 components having reported June-quarter results already, earnings growth stands at 10.5%, according to consensus data. The blended estimate, earnings and expected earnings, is 10.7%.

- Atlassian -CEO Scott Farquhar said the company expects its strong growth to continue into 2018 after it booked a 36% annual rise for the 2017 financial year. Atlassian’s 36% revenue jump saw it hit $US619.9m for the 2017 financial year, with an increased net loss of $US42.5m. The company forecast slightly lower revenue growth of 33% to 34.5% to between $US826m- $US834m. The CFO has resigned though in some bad news.

- EU citizens will still be allowed to come to live and work in UK after Brexit, the government has said.

- Virgin Atlantic founder Sir Richard Branson sells 31% stake in airline for £220m as part of new tie-up with Air France-KLM.

And finally…thanks to Hans for this cracking ad from Germany.

Have a great weekend

Clarence

XXX

Up on the Gold Coast next week for a few days at the AIA Conference speaking on ‘How to avoid Landmines in the market”. May or may not have time to post!!! We shall see.

Get a Global take on things at http://www.ntmarkets.com