Headlines Today

- ASX 200 up 50 to 5677.

- High 5788. Low 5643. Below average volume again.

- Miners and energy stocks lead the charge.

- Banks up around 1%.

- Gold miners give ground

- Builders continue recent rally.

- Utilities, telcos and defensives struggle.

- SUN takeover of TWR falls over on NZ competition concerns.

- RBA governor speaks.

- CPI below forecasts at 1.9% despite healthcare and tobacco rises.

- ACCC takes action against Ford on misleading consumers.

- AUD falls on lower CPI to 78.91c

- US Futures unchanged.

- Asian markets mixed with Japan up 0.45% China down 0.58%.

STOCK STUFF

- STO +5.28% moves ahead on oil price and recent report.

- MUA +13.64% recovers after board reaffirms confidence in business

- OZL +10.72% on copper price and quarterly report.

- TWE +1.98% on positive broker call.

- RFG +4.93% forms JV in Middle East

- FMG +4.74% bounce on iron ore price rise.

- DOW +3.06% has 68.37% of SPO.

- SDA +3.34% bounces on acquisition rethink.

- SVW +10.57% Caterpillar US results show good growth.

- IGO -3.65% disappointing quarterly.

- CGF -1.37% broker downgrade.

- SFR +8.19% copper price rise.

- CCL +0.73% recovers some fizz.

- TLS +0.24% trying hard to recover.

- DMP -5.17% suffer on high PE sell off.

- SUL -3.02% eases after good run yesterday

- SIG +9.88% drops legal fight with Chemist Warehouse.

- Biggest risers – OZL. SVW, SIG, SFR, FMG and CCV.

- Biggest fallers – DMP, ALL, OGC, SIQ, and SPK.

TODAY

- Mirvac Group (MGR) +2.33% has announced an agreement with Suntec REIT for the sale of a 50% interest in its Olderfleet, 477 Collins Street office development in Melbourne. The total consideration for the 50% interest of the completed development is $414 million.

- St Barbara (SBM) – unchanged – has released their quarterly report for Q4 June. The company has highlighted: Record consolidated production of 381,101oz of gold. Low AISC of $907/oz. Debt free with $161m Cash at bank.

- Nextdc (NXT)+1.98% has bid for its Asia Pacific Data Centre REIT (AJD) – unchanged – at 185c and 360 Capital has withdrawn its request for the meeting Friday. the proposed acquisition for the REIT is to be funded by existing facilities and remaining cash reserves. 360 Capital (TGP) +% the winner with $6.6m profit on stake.

- Bapcor (BAP) +% Bapcor is eyeing a toehold in Asia in its next leg of expansion after the company revealed it had found an extra $11m in cost savings after a review of the Hellaby business it acquired in New Zealand for $334m in January.

ECONOMIC NEWS

- Second quarter CPI lifted 0.2% leaving the annualised inflation rate at 1.9%. Core inflation, by contrast, matched forecasts coming in at 0.5% for the quarter for annual growth of 1.8%.

- Philip Lowe relaxed and in no hurry to lift rates. Will not move in ‘lockstep’ with other central banks. Lowe said: “Just as we did not move in lockstep with other central banks when the monetary stimulus was being delivered, we don’t need to move in lockstep as some of this stimulus is removed”.

- On wage growth, he said no sign of any economies experiencing of sustained wage growth.

- The RBA has not sought to stimulate a rapid lift in inflation.

For the full text of his speech click here.

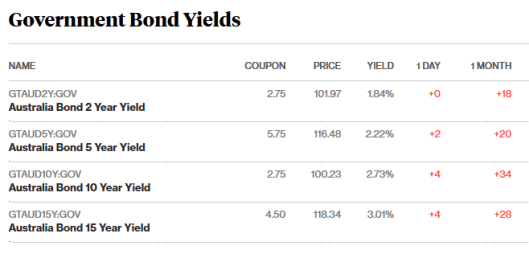

BOND MARKET UPDATE

ASIAN NEWS

- Trading in Hong Kong-listed shares of China Ocean Industry Group was halted on Wednesday after the stock tumbled as much as 74.5% to a record low.

- Chinese conglomerate currently under serious scrutiny, HNA Group’s planned US$416m investment in a US in-flight entertainment and Internet-services provider collapsed after the two companies failed to get approval from Washington.

EUROPE AND US MORNING HEADLINES

- UK GDP Q2. French consumer confidence.

- Mega Thursday looming for European results with companies worth around US$3 trillion reporting. Pharmaceutical giants Roche Bayer and AstraZeneca are on the agenda, along with telecommunications providers Orange, Telefonica and Telecom Italia SpA and transportation giants Volkswagen, Airbus and Fiat Chrysler. Consumer stocks to report include Anheuser–Busch InBev, Nestle SA, Danone, Diageo Plc and British American Tobacco Plc, along with a trading update from Britvic.

- US senate votes for Russian.

- Healthcare reforms stall again.

- Yellen is not being completely ruled out of a new term despite Gary Cohn rumoured to be tapped on the shoulder.

- FOMC USD in focus.

- Sperm counts have dropped 50% in 40 years in North America, Europe, Australia, and New Zealand.

- UK to ban new diesel and petrol cars from 2040.

- BMW has chosen the UK to build electric Mini. New model due 2019.

And finally…………….

Dearest Dad,

I am coming home to get married soon, so get your check book out. I’m in love with a boy who is far away from me.

As you know, I am in Australia … and he lives in Scotland. We met on a dating website, became friends on Facebook , had long chats on Whatsapp. He proposed to me on Skype, and now we’ve had two months of a relationship through Viber.

My beloved and favorite Dad, I need your blessing, good wishes, and a really big wedding.

Lots of love and thanks.

Your favorite daughter,

Lilly

THE RESPONSE

My Dear Lilly,

Like Wow! Really? Cool!

Whatever … I suggest you two get married on Twitter, have fun on Tango, buy your kids on Amazon, and pay for it all through PayPal.

And when you get fed up with this new husband, sell him on eBay.

Love,

Your Dad

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com