ASX bounces 17 points to 5821 as the banks and Telstra rallies and miners and oil companies slip. Retail stocks hit as Amazon announces plans. Asian markets modestly higher with Japan up 0.07% and China up 0.09%. AUD pushed up to 75.09c with US futures up 7.

STOCKS AND SECTORS

- Miners slipped again after iron ore reversed early gains in Asia. Fortescue Metals (FMG) -1.15%, BHP -1.13% and RIO -0.39%. Base metal stocks continued to decline led by Independence Group (IGO) -4.24%, Western Areas (WSA) -3.69% and Oz Minerals (OZL) -2.95%.

- Energy stocks suffered as WTI Crude fell heavily last night on inventories. Woodside (WPL) -1.19%, Santos (STO) -2.46% and Oil Search -0.55% with coal stocks too weaker as Whitehaven Coal (WHC) -1.40% though New Hope (NHC) +1.74%.

- Gold miners down again though small caps had spots of strength including Gold Road (GOR) +1.63% but Saracen Minerals (SAR) -5.94% continued its decline as did Northern Star (NST) -1.08% and Evolution Mining (EVN) -0.42%.

- Industrials mixed with retail under pressure as Amazon confirmed its vast and fast strategy for Australia. Harvey Norman (HVN) -3.45%, Super Retail (SUL) -1.82%, JB Hi-Fi (JBH) -1.77% and Vita Group (VTG) -3.04%. Downer EDI (DOW) +2.36% continues to bounce back after the retail offer was placed.

- IT and telcos mixed with the action in Telstra (TLS) +2.91%, back on the offensive with Vocus Group (VOC) -0.29% resuming the down trend and TPG Telecom (TPM) +2.89% gaining friends. Nothing much shaking the trees in the IT sector with losses in Carsales (CAR) -unchanged, Computershare (CPU) -0.44% and MYOB (MYO) -unchanged.

- Banks and financials a pocket of strength as the Big Bank Basket gained after a few days of losses. The BBB hit $183.59 with insurers also doing well as QBE Insurance (QBE) +0.57%, Suncorp (SUN) +1.13% and IAG +1.01%. REITS also did well with Westfield Corp (WFD) +1.54%, Vicinity Centres (VCX) +1.37% and Scentre Group (SCG) +1.14%.

- Healthcare rose modestly with Resmed (RMD) +1.32% a stand out as were Japara Healthcare (JHC) +1.46%.

- Speculative stock of the day: Hills Ltd (HIL) +20.59% after announcing a continued investment in Hills Health Solutions with its dementia software platform or its nurse call solution.

CORPORATE NEWS

- Sydney Airport (SYD) +1.02% showed 5.7% passenger growth in international traffic with domestic up a mere 0.2% for a total increase of 2.2% The decision to develop Badgerys Creek rests with SYD due 8th

- Santos (STO) -2.46% has reported a further reduction in costs and debt. Net debt was lowered by $US380m ($505 million) in the March quarter to $US3.1bn. Sales in the March quarter climbed14% from the March quarter last year to $US684m, despite a 6%slide in output to 14.8m barrels of oil equivalent.

- Woodside Petroleum (WPL) -1.19% reported sales of $US895m in the March quarter, down 8.8 per cent from a year earlier. Production slid 9.7% to 21.4m barrels of oil equivalent, impacted by a worse-than-usual cyclone season and the expiry of a domestic gas sales contract. The company still maintained its full-year guidance for production.

- Rio Tinto (RIO) -0.39% The company has reiterated its previous forecast to ship between 330m and 340m tonnes from WA in 2017. A wide guidance has been set with copper production of between 525,000 to 665,000 tonnes after the strike at Escondida affected production.

- Iluka Resources (ILU) +11.04% after a quarterly report was a positive on mineral sands strength with higher sales and volumes. The company reported revenue of $218.5m up from $102m a year ago. Production for the quarter also jumped to 336,900 tonnes, from 233,200 tonnes a year ago. The recent takeover of Sierra Rutile looks to be bearing fruit and the stock hit a new yearly high.

- Challenger (CGF) -0.86% announced annuity sales up 53% to $0.9bn with AUM and funds of $66.6bn with net inflows of $1bn. The company is now forecasting Cash Operating Earnings of beteeen $620m to $640m

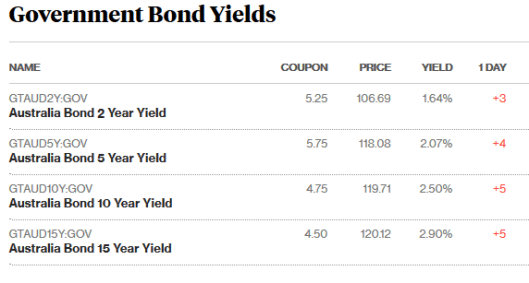

BOND CORNER

ECONOMIC NEWS

- New Zealand’s inflation has finally hit the central bank’s target mid-point of around 2%. The consumer price index rose 1% from the previous quarter, according to Thursday’s report from Statistics New Zealand, leading to annual inflation of 2.2%.

ASIAN NEWS

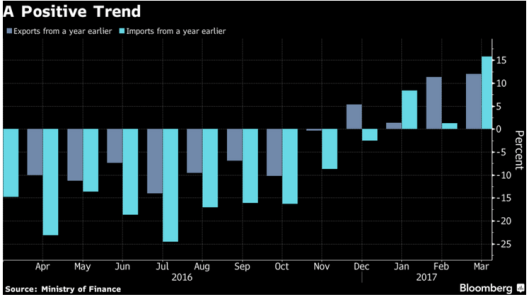

Japan’s exports expanded for a fourth consecutive month in March,, according to the Ministry of Finance today.

Key Numbers

- Exports rose 12% from a year earlier (median estimate +6.2 percent).

- Imports increased 15.8% (median estimate 10 percent).

- The trade surplus for March was 614.7 billion yen (US$5.64 billion), compared with an estimate of 608 billion yen.

EUROPE AND US

- Brussels is starting to freeze the UK out of EU contracts. Hardly a surprise.

- The IMF has declared ‘Austerity is Over’. After five years of the austerity and belt tightening from major economies. “Advanced economies eased their fiscal stance by one-fifth of 1%c of GDP in 2016, breaking a five-year trend of gradual fiscal consolidation.”

- Facebook has confirmed it is working on mind reading technology. Thought it was April Fools’ Day when I read this. At Facebook’s annual developer Building 8 (a secretive FB division), said it was working on “optical neuro-imaging systems” that would allow people to type words directly from their brain at 100 words per minute: five times the speed possible on a smartphone. Hope they have spell check.

And finally…

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com