ASX slips another 33 points to close at 5804 with banks,REITs and energy stocks leading the losses as buyer emerge in big miners and telcos. Asian markets slightly mixed as China drops 0.77% and Japan up 0.01%. AUD 75.25c and US Futures up 2.

STOCKS AND SECTORS

- Miners surprised with some bargain hunting as the price of iron ore stabilises a little. BHP -0.04%, RIO +1.55% and Fortescue Metals (FMG) +2.95%. Base metals though suffered some slings and arrows with Independence Group (IGO) -7.30%, Sandfire (SFR) -0.68%, South32 (S32) -1.79% and Oz Minerals (OZL) -0.67%.

- Energy stocks fell hard as Oil Search (OSH) -1.90%, Woodside (WPL) -0.91% and Santos (STO) -0.54%. Coal stocks too heavily sold off with Yancoal (YAL) -8.11% and Whitehaven Coal (WHC) -1.72%.

- Gold miners an unexpected casualty despite moves in bullion and AUD gold at $1710 oz. Northern Star (NST) -4.12%, Evolution Mining (EVN) -4.40%, Saracen Mineral (SAR) -2.42%. There were winners in the sector but mainly second liners like Westgold (WGX) +3.37% and Gold Road (GOR) +0.82%.

- Banks and Financials the big draw down today as the Big Bank Basket fell to $182.35 from $185 with Westpac Bank (WBC) -1.10% the worst hit. Insurers also in the negative led by IAG -1.49% QBE Insurance (QBE) -1.98% and NIB Holdings (NHF) -1.76%.

- REITs had a nasty day too, Scentre Group (SCG) -2.44%, Mirvac Group (MGR) -2.59% and Stockland (SGP) -2.22%.

- Industrials eased with Aurizon Holdings (AZJ) -1.92%, Transurban (TCL) -1.65% and Qube Holdings (QUB) -0.78%. Building stocks too fell with Boral (BLD) -1.37% and James Hardie (JHX) -1.00%.

- Healthcare sold off a little, CSL -0.83%, Sirtex Medical (SRX) -2.67% and Ansell (ANN) 1.53-%. Healthscope (HSO) +2.33% had a strong day as did Mesoblast (MSB) +4.98% after its recent pullback and consolidation.

- IT and Telco mixed with some aggressive buying in Telstra (TLS) +3.25% after the 400c became the line in the sand. Bargain hunters also crawled out from the trenches and punished the shorts in TPG Telecom (TPM) +7.09% and much maligned Vocus Group (VOC) +10.32%. A good day for the troubled trio but still a long way back to redemption. IT stocks though slipped as Computershare (CPU) -2.02% and Nextdc (NXT) -0.99% were a couple of casualties although elsewhere we saw some gains in Xero (XRO) +1.48% and Technology One (TNE) +0.95%.

- Speculative stock of the day: KIN Mining (KIN) +62.22% after a spectacular primary gold zone discovery at Lewis in WA. One intersection of 5m at 117g/t Au.

CORPORATE NEWS

- Brambles (BXB) +5.94% issued a positive update to trading conditions. New contract wins in the US. sales revenue from continuing operations for the first nine months of 2016-17 was up 4% to $US4.09bn compared with the previous corresponding nine months. Sales revenue growth from the Europe, Middle East and Africa pallets operations had been 1% for the same period.

- Tatts Group (TTS) +0.23% has received a new takeover bid from the Pacific Consortium at 421c cash. The new bid is aimed at upsetting the agreed $11bn merger between Tabcorp (TAH) +% and Tatts.

- SurfStitch (SRF) -3.70% has agreed to sell its online media business Garage Entertainment, the unit was picked up by Madman Entertainment, the film distribution business formerly part of Funtastic and taken private by a bunch of Australian businessmen, for a nominal price.

- Downer EDI (DOW) +5.95% after announcing the completion of the retail shortfall in a bookbuild. 1m retail entitlements were not taken up by shareholders, hardly surprising given the price at 595c.

- Yowie Group (YOW) -7.69% after announcing the launch of its “Discovery World’ addition to the portfolio. Unfortunately, the company also issues a small downgrade to guidance. Sales outlook now reduced from 85% to 75% with lower quarters in US.

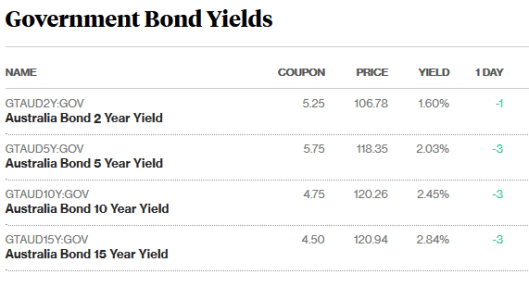

BOND CORNER

ECONOMIC NEWS

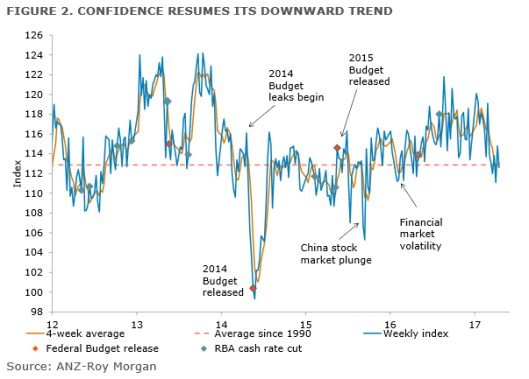

Consumer confidence fell 1.9% last week dragging the index below its long-term average.

- Mortgage lodgements by first home buyers rose to 10 per cent in the three months to March, the highest level since the September quarter of 2014, figures from listed mortgage broker AFG show.

- Annual growth of luxury vehicle sales has fallen to 4-year lows according to CommSec analysis.

ASIAN NEWS

- Japan’s benchmark 10-year bond yield fell to 0% for the first time since November.

EUROPE AND US

- The elephant in the room is the strategy to transition central bank balance sheets back to a more normalised level. Shrinking the balance sheets as it is known. Combined, the balance sheets of the three now total about US$13 trillion, equating to greater than either China’s or the euro region’s economy.

- The IMF raised its forecast for UK growth this year to 2%, from a prediction of 1.5% in January. The UK is expected to grow faster than France, Germany and all other G7 economies this year apart from the US.

And finally…..

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com