ASX 200 closed down a modest 7 points at 5747 after testing 5700 again in early trade. Banks turned around early losses to ‘save’ the market again. Solly Lew buys 10% of Myer (MYR)? Asian markets eased with Japan down 1.42% and China down 0.02%. AUD 76.28c and US futures down 115 points.

STOCKS AND SECTORS

- Miners back in sell off mode today with BHP -2.93%, RIO – 1.81% and Fortescue Metals (FMG) -3.04%. The buy back from South 32 (S32) -1.84% did nothing for the share price and other base metal stocks also saw selling with leaders Independence Group (IGO) -2.72% and Western Areas (WSA) -4.58%.

- Gold stocks back in favour with Evolution Mining (EVN) +5.37% recovering from the sell down last week with Northern Star (NST) +1.96% and Oceanagold Corp (OGC) +3.85%.

- Energy stocks put in a better day led by Woodside (WPL) +0.68% and Origin Energy (ORG) +2.24% on an update on Silver Star – 1. Both Karoon (KAR) +2.45% and FAR +4.00% both outperformers after a find off Senegal for FAR.

- Industrials mixed with A2Milk (A2M) +3.07% at another all-time high as other Chinese facing consumer stocks took a breather. Australian Agriculture (AAC) -1.20%, Bega Cheese (BGA) -1.41%, Blackmores (BKL) +0.14% and Bellamy’s (BAL) -0.65% mixed. Downer EDI (DOW) +3.06% stage a slight rally despite the disappointing capital raising last week, a large seller has cut its losses with a sale of 23.5m at 555c. Clean Teq Holdings (CLQ) +4.44% also had a positive day.

- Consumer stocks eased too Domino’s Pizza (DMP) -0.09%, Harvey Norman (HVN) -1.60% and JB Hi-Fi (JBH) -1.74%. Fairfax Media (FXJ) +2.94% on media reports private equity is about to pounce.

- Healthcare mildly better although Mesoblast (MSB) -6.69% after raising US$40m at 200c to further phase 3 trials.

- IT and Telcos weaker Nextdc (NXT) -1.79%, Redbubble (RBL) -10.67% continuing the slide into oblivion and Telstra (TLS) -0.44%

- Banks and financials turned the market around today from a drab down 50 start to a more modest down 10 points. The Big Bank Basket pushed up to $181.06. Pepper Group (PEP) +6.06% had a positive day on media reports this morning it was set to step into the breach on investor loans as APRA curbs banks influence. REITs too did well with Stockland (SGP) +1.98% the standout on an Asian Investor roadshow presentation.

- Speculative stock of the day: Zelda Therapeutics (ZLD) +18.07% after announcing the company had entered a strategic partnership with Animal Health Company CannPal to use cannabinol-based treatments. Seems there is more gas in the medicinal cannabis tank and story. MMJ Phylotech (MMJ) +4.55% were suspended this afternoon pending an announcement on the proposed importation of CBD capsules into Australia. This one will do well on the announcement.

CORPORATE NEWS

- Suncorp (SUN)-0.84% is seeking to raise $250m through a capital notes offer. The company also issued an update on the impending Cyclone ‘Debbie’.

- South32 (S32) -1.84% will take advantage of its bulging bank balance to launch a $US500m share buyback. The diversified miner has operations in Australia, South Africa and South America, had net cash (that is, cash minus debt) of $US859m at December 31. The buyback is expected to be completed over the next 12 months and would represent 4.5% of the group’s current market capitalisationof $14.5bn.

- BHP Billiton (BHP) -2.93% is suspending operations at its South Walker Creek coal mine in Queensland with Cyclone Debbie expected to cross the coast on Tuesday close to the site.

- Myer (MYR) +18.31% up strongly after a block trade of nearly 10% of the company at 115c. 80m shares were traded as the company may well be in ‘play’. Rumours are Solly Lew has bought 10% of the company.

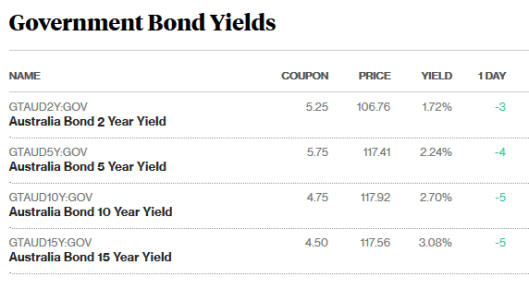

BOND CORNER

ECONOMIC NEWS

- Almost one in five young people have fewer hours of work than they want, with underemployment in the youth labour force at its highest level in 40 years.

ASIAN NEWS

- Chinese steel and iron ore futures have plunged to their lowest in more than six weeks, extending a five-day losing streak. The most-active rebar contract on the Shanghai Futures Exchange was down 4% at 3026 yuan ($US440.31) a tonne. Iron ore on the Dalian Commodity Exchange plunged 6%to 545.5 yuan ($US79.37) per tonne, having touched 541 yuan earlier.

- Iron ore stockpiles at major ports in China, the world’s top steelmaker, rose for a second week, topping 132m tonnes last week, the highest since at least 2004

- Investments giant Old Mutual is selling a US$446m (£358m) stake in its asset management arm in the latest stage of its plan to split into four separate companies. HNA Capital US, part of the Chinese finance group HNA will buy 24.9% in the asset management business adding to its US$30bn spending spree on financial services broadening its appeal from tourism and aviation.

EUROPE AND US

- ‘Twas the week before Article 50 when all around the house Not a politician was stirring, not even in the House.

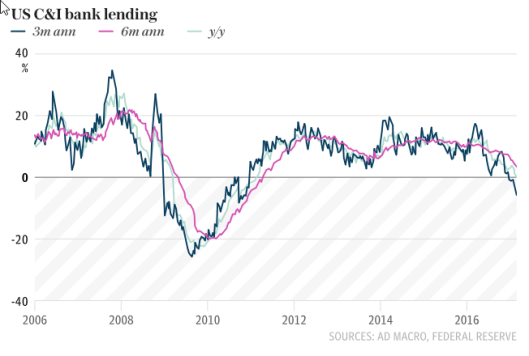

- Some credit strategists are a little concerned. US Bank lending is contracting is falling fastest than any time since Lehman. Data from the US Federal Reserve shows that the $2 trillion market for commercial and industrial loans peaked in December. The sector has weakened abruptly as lenders tighten credit, especially for non-residential property. Over the last three months it has dropped at a rate of 5.4% on annual basis, a pace of decline not seen since December 2008.

- The Atlanta Fed’s instant gauge of GDP growth for the first quarter has dropped from 3% at the start of the year to just 1%.

And finally……………

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com