ASX 200 finally throws in the towel falling 18 points to 5741 as resources are routed and banks hold on to modest gains. Ex dividends hurting sentiment and 10-year bond yield rallying hard. Asian market mixed again as Japan rises 0.19% and China down 0.75%. AUD looking to test 75c falling to 75.12c. US Futures down 10.

STOCKS AND SECTORS

- Miners bore the brunt of it today with BHP -5.03% going ex-dividend and the oil weakness punishing them further. Iron ore fell in Asian markets sending Rio Tinto (RIO) -2.04% and Fortescue Metals (FMG) -3.85%. Base metals nasty too as Independence Group (IGO) -3.58% and Western Areas (WSA) -5.08% after big falls in nickel.

- Energy stocks down but not as bad as they could have been with losses more muted that the oil price fall would suggest. Origin Energy (ORG) -1.09%, Santos (STO) -3.28% and Whitehaven Coal (WHC) -3.99% on news from China that there will be no new limits on production.

- Golds mixed too with Evolution Mining (EVN) +0.52% managing gains although Silver Lake (SLR) -5.13%. Maybe the Aussie gold price holding up is helping the sector a little.

- Banks the big winners today as bond yields continue to rise helping the sector. The Big Bank Basket rose to $183.07 although insurers didn’t catch the bond yield bump. QBE Insurance (QBE) -2.18% ex dividend.

- Industrials found a few buyers in places Domino’s Pizza (DMP) +2.47% rallied after yesterdays’ presentation from CEO and news of a full audit of Australian stores. Ardent Leisure (AAD) +4.22% continued its renaissance after February Dreamworld numbers. We highlighted the rally potential on Tuesday with 180c a target.

- Healthcare mixed Mesobalst (MSB) -2.93% couldn’t hold 200c but maybe tomorrow.

- Telcos slid again as Telstra (TLS) -0.86% gave up the recent dead cat bounce. TPG Telecom (TPM) -0.78% and Vocus Group (VOC) -1.12%. IT and tech stock dogs continue to bark as Netcomm Wireless (NTC) -6.93%, Dicker Data (DDR) -4.92% and Codan Limited (CDA) -3.02%. Nextdc (NXT) +2.56% announced a new director and seemed to impress. Sharon Warburton was appointed non-executive and is currently a non-exec at Fortescue Metals. Isentia (ISD) +2.46% continue the bounce from oversold levels.

- Speculative stock of the day: Zelda Therapeutics (ZLD) +21.57% as medicinal cannabis stocks continue to do really well. Creso Pharma (CPH) +16.13% pushing further ahead as investors warm to the cannabis story. MMJ Phylotech (MMJ) +2.63%. See our QOD back on 24th February for rationale and some further stock ideas.

CORPORATE NEWS

- Tatts Group (TTS) +2.45% Tabcorp (TAH) +2.76% today announced the ACCC had some concerns on the proposed merger but the regulator seems happy that punters have a good choice of where to lose their money. The ACCC still has concerns on the telecasting side of the business and has postponed the decision until early May. TAH has proposed selling the Queensland electronic gaming monitoring business Odyssey Gaming Services, which generated A$12.6m in revenue in 2016

- DP World is introducing a new infrastructure surcharge in its container operations in Sydney and Melbourne. $21.16 per container in Sydney and $32.50 in Melbourne. The market is assuming that Patricks (Qube) +4.66% also moves in a similar fashion. Yet another inflationary pressure to be passed on to customers. Citi has a buy on the stocks with a 301c price target.

- Rio Tinto (RIO) -2.04% Chair Jan du Pleiss is set to announce his retirement after 8 years at the top. Maybe the Simandou issue is worrying him too.

- The Hunter Hall (HHL) saga continues with the International shares in a trading halt pending an announcement on the final stages of a transaction, possibly to merge Pengana Capital and HH with Soul Pattinson (SOL) -1.61% driving the deal. Looks like Peter Hall has done a deal to sell the balance of his shares to Soul Patts.

BOND CORNER

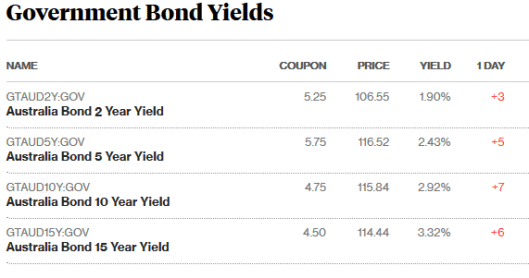

- Aussie 10-year yields hit their highest since late 2015 at around 2.92% US ten years are now yielding 2.56%. US Ten-year yields have nearly doubled since touching a record low 1.32% in July 2016.

ECONOMIC NEWS

- Moody’s expects no change to Australia’s coveted triple-A credit ratings and stable outlook due to the country’s robust institutional framework and stronger fiscal metrics.

- Goldman Sachs is now predicting a rate RISE in November.

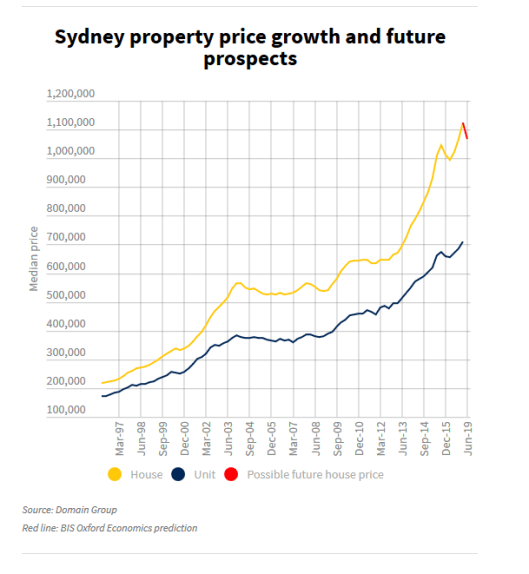

- BIS Oxford Economics is predicting a 5% drop in Sydney house prices in the next two years. A rounding error really. Steeper falls are expected in the apartment market.

ASIAN NEWS

Dalian iron ore futures slide another 2% to 652 yuan ($US94.26), after earlier in the session dropping to 666.5 yuan, their lowest in a month. BHP chief financial officer Peter Beaven told the AFR Business Summit this morning that fading stimulus measures in China could bring “much lower” iron ore prices.

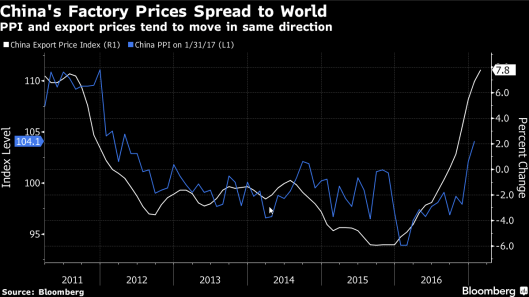

- Producer price index rose 7.8% last month from a year earlier, compared with median estimate of 7.7% and a 6.9% in January

- Consumer price index rose 0.8% versus 1.7% increase forecast by analysts, as timing of Lunar New Year holidays skewed the reading.

- Consumer prices of food fell 4.3% from a year earlier

EUROPE AND US

- Another big deal in the making with a rumoured tie up between US based PPG Industries and Dutch Akzo Nobel in a US$42bn tie up. A deal was most likely to be a friendly merger.

UK Budget key points

- The economy shown “robust growth” as the UK begins its exit from the European Union.

- Last year the UK economy grew faster than all the major economies expect Germany.

- Growth will be up this year (from 1.4% to 2.0%), but down for the next three (compared to previous projections).

- Chancellor says that £140bn has been raised since 2010 by tackling tax avoidance evasion and non-compliance.

- Top 1% now pay 29% of all income tax, Chancellor Hammond says.

- Sugar tax set at 18p and 24p as expected – but will raise less cash than expected.

And finally……………..

Paddy, the Irish boyfriend of the woman whose head was found on Galway beach was asked to identify her.

A detective held up the head to which point Paddy said “I don’t think that’s her, she was taller than that!”

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com