Sorry no report Friday..my dog did a runner in the Sydney storm and spent two hours driving around trying to find him…

ASX 200 eased through 5800 to close down 11 at 5795 on thin volume as industrial results underwhelmed and Brambles shocked. Banks slightly positive with results the focus. Asian markets positive with Japan up 0.19% and China up 1.07%.AUD clinging to 77c with US Futures up 15. US markets closed tonight for President’s Day

STOCKS AND SECTORS

- Miners slipped slightly today with BHP -0.64%, RIO -0.22% though Fortescue Metals (FMG) +1.45% and BlueScope (BSL) +4.02%. Base metal miners also slightly weaker with Iluka Resources (ILU) -1.12%, South32 (S32) -1.86% and Independence Group (IGO) -1.17%. Other base metals also faded with Syrah Resources (SYR) -3.44% and Western Areas (WSA) -2.29%.

- Energy stocks weaker again too with Santos (STO) -1.50%, Oil Search (OSH) -1.67% and Woodside (WPL) -0.98% in the oil space but coal stocks improved slightly as China moved to restrict North Korean coal exports. Soul Pattinson (SOL) +1.21% and New Hope (NHC) +4.29%

- Gold stocks eased again with Evolution Mining (EVN) -0.42%, Gold Road (GOR) -1.75% though Resolute Mining (RSG) +3.92% rallied slightly.

- Industrials were minefield again today with results dominating. Consumer stocks eased Thorn Group (TGA) -6.07%, Bapcor (BAP) -3.83%, JB Hi-Fi (JBH) -1.87%, Myer Holdings (MYR) -2.72% and Sealink Travel (SLK) -5.71%. Positive performance though from some healthcare stocks like Mayne Pharma (MYX) +2.20%, Sirtex (SRX) +3.11% and Mesoblast (MSB) +3.11%. Pathology and radiology down again though with Sonic Healthcare (SHL) +0.23% and Primary (PRY) -1.51% together with Ramsay Health Care (RHC) -1.06%.

- T. Stocks bashed again with Hansen Technologies (HSN) -8.72%, CSG Limited CSG) -9.38

- % and Class1 (CL1) -1.95%. Telstra (TLS) unchanged though no such luck for Superloop (SLC) -5.11%, Chorus (CNU) -3.32% though Vocus Comm (VOC) +1.23% and TPG Telecom (TPM) +1.10% managed small gains.

- Banks once again a bright point as ANZ +0.36% upgrades filter through. The Big Bank Basket rallied again to $182.61 but the rest of the financials not so well supported. Insurers eased in modest trade with QBE Insurance (QBE) -1.58% and Suncorp (SUN) -0.37% and Insurance Group (IAG) -0.34%.

- Speculative stock of the day: Cohiba Minerals (CHK) +50.00% after execution of binding terms to acquire 100% of CobaltX and a heavily oversubscribed placement to raise $1.443m and a proposed rights issue of 1:6 to raise another $515,000 at 1.3c.

CORPORATE NEWS

- Monadelphous (MND) +2.61% on news of a proposed five-year contract worth $50m a year in a JV with Jacobs Engineering, to provide services across Oil Search‘s (OSH) -% facilities in Papua New Guinea.

- oOh!Media (OML) +2.22% has lifted full-year net profit 17.4% to $21.6m, boosted by acquisitions and the continued rollout of its digital billboards. Revenue for the 12 months to December 31 rose 20.1%, with underlying earnings up 27% at $73.5m, at the upper end of guidance.

- NIB Holdings (NHF) +8.28% raised full-year earnings forecasts as profits rose 65% to $71.8m as net policy growth of 2.1% led to revenue growth of 7.3%. A very different story to Medibank Private (MPL) +2.96% with numbers going backwards.

- WorleyParsons (WOR) -12.78% disappointed the market with a $2.4m loss and planned cost cutting of $450m in 2016/17 after revenues slipped 35% to $2.7bn. No interim dividend declared as gearing has risen from 29.2% to 32.9%.

- Beach Energy (BPT)+1.44% announced a better than expected profit of $103.4m. Drilling activity will pick up this year, with up to 60 wells to be drilled, including 10 added for this June half. Beach, which is 21% owned by Seven Group (SVW)+1.38%, declared an interim dividend of 1c, up from zero a year earlier.

- Brambles (BXB) -9.90% reported disappointing results even by their standards especially given the recent update as the CEO transition is speeded up. it booked a 5% rise in constant-currency sales to $US2.74bn and a 3% improvement in underlying profit of $US468.9m after stripping out one off items. The bigger miss is likely to be in underlying profit, which is now tipped to be flat in fiscal 2017 compared to the prior year and clearly well short of original market expectations for around 10% growth.

- G8 Education (GEM) +3.65% after reporting FY underlying net profit after tax of $93.3m, up 7.1%. FY revenue $778.5m up 10.2%. Interestingly a Chines group CFCG Investment Partners has agreed to subscribe for 54.846m shares at 388c to raise $212.8m. Following the placement, the Chinese group will hold around 12.45%.

- GWA Group (GWA) unchanged reported an 8% rise in net profit for the first half to $26m on revenue of $223.4 million, up 2% on a year ago. Fully franked interim dividend of 7.5c, up 7% on the previous year.

- Nanosonics (NAN) Unchanged announced a net profit of $22m from a loss of $3.3m a year earlier. Revenue more than doubled to $36.1m and gross profit rose 109% to $26.3m.

- iSelect (ISU) -1.37% posted a profit of $2.6m after a loss of $4.2m last year. Revenue rose 18% to $78m, EBIT rose to $2.8m from a loss of $6.9 million and EBITDA went from a loss of $3.6m to a profit of $5.9m. The company will pay an interim dividend of 1.5c fully franked.

- Bubs Australia (BUB) +29.41% after securing shelf space in Chemists Warehouse for its range of organic cereal and baby infant formula.

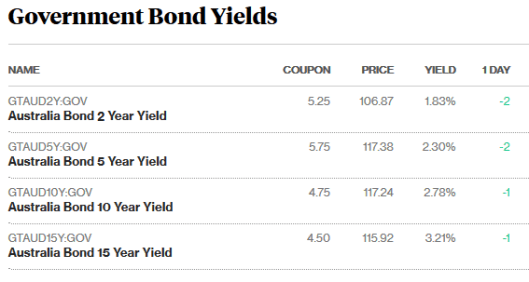

BOND CORNER

ASIAN NEWS

- China’s coke and coking coal futures are up after Beijing suspended imports of North Korean coal as part of its efforts to implement United Nations sanctions. The most-active May coke futures were up 1.3% at 1709.5 yuan ($US249.05) per tonne, while coking coal futures were also up 1.3% at 1250 yuan.

- Alibaba is teaming up with Shanghai Bailian one of China’s largest supermarket and department store chains, as Alibaba accelerates an effort to employ technology to shake up old-fashioned retail. Alibaba’s planning to help upgrade some of Bailian’s 4,700 stores across the country, integrating everything from customer relations to payment and logistics.

Japanese economic data today

- The value of exports rose 1.3% in January from a year earlier. Forecasts for a 5% increase.

- Imports rose 8.5% over the same period, versus an estimated 4.8% rise.

- The trade deficit for January was 1.1 trillion yen (US$9.6 billion).

- Exports to the U.S. fell 6.6% from a year earlier.

- Shipments to the EU decreased 5.6%.

- Those to China, Japan’s largest trading partner, climbed 3.1%.

EUROPE AND US

- After announcing a $143bn bid for Unilever on Friday, Kraft has pulled out as there was early opposition to the deal. Unilever said the deal fundamentally undervalued the company and Warren Buffett who owns a substantial shareholding in Kraft hates hostile takeovers.

- London house prices posted their largest annual drop in almost six years in February as high values deterred buyers. The average asking price in the capital fell 0.4% to GBP 641,116 (US$797,000) this month from a year earlier, the first annual decline since April 2011. For the U.K. as a whole, asking prices rose 2% to an average GBP 306,231, the biggest monthly increase in a year.

Sorry no report Friday..my dog did a runner in the Sydney storm and spent two hours driving around trying to find him…

And finally……

The wife’s back on the warpath again. She was up for making a sex movie last night, and all I did was suggest we should hold auditions for her part.

After both suffering from depression for a while,me and the wife were going to commit suicide yesterday. But strangely enough, once she killed herself, I started to feel a lot better. So I thought,“Screw it, soldier on!”

I’ve accidentally swallowed some Scrabble tiles.My next crap could spell disaster.

Bought my wife a hamster skin coat last week. Took her to Luna Park last night, and it took me 3 hours to get her off the Ferris wheel.

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com