ASX 200 holds the 5600 level closing at 5622 up 6 points as resources rally and banks ease. RBA Left rates on hold and some encouraging data from China helped stem the early losses. Asian markets slightly weaker with Japan down 0.06% and China down 0.38% AUD slightly higher at 76.75c with US Futures down 3.

Back in Black as big miners ride to the rescue. Big range today of 5622 to 5582. Volume not great though.

STOCKS AND SECTORS

- Banks and financials took their cue from Macquarie Group (MQG) -1.42% backing up the lacklustre National Australia Bank (NAB) -0.62% results with a fairly anaemic set of numbers themselves. The Big Bank Basket fell to $172.00 today as insurers slid, IAG -% and Suncorp (SUN) -1.37%with red hot takeover favourite QBE Insurance (QBE) -1.36%.

- Industrials dominated by the good news from Transurban (TCL) +6.36%. Who would have guessed that building and tolling roads in Australia and the US would be so profitable. Other infrastructure stocks rallied in sympathy, Sydney Airport (SYD) +2.56%, Auckland International (AIA) +1.23% and even QANTAS (QAN) +1.52%. Consumer stocks though not so much fun. Tabcorp (TAH) -4.28% went ex-dividend but the news of Crown entering the online market through Clubs NSW will not be taken well.

- Media stocks also off the boil as Fairfax (FXJ) -1.12%, Seven West Media (SWM) -1.92%,ICAR Asia (ICQ) -6.25% and REA Group (REA) -0.65%. Bellamy’s (BAL) +6.52% though stunned for the second day as takeover fever hit the share price. Graincorp (GNC) +3.17% had some fun too as did Yowie Group (YOW) +4.67%

- Miners reversed early losses as Fortescue Metals (FMG) +2.48% led the big caps back to the promised land. BHP +0.19%, RIO +0.42% and South32 (S32) +0.77%. No joy though for Orocobre (ORE) -3.21% as sellers made way for the Galaxy Resources (GXY) capital raising.

- Energy stocks a mixed bag. Santos (STO) 1.28-% slipped yet again, with Oil Search (OSH) +1.16% and Paladin Energy (PDN) +4.17% showing gains with Yancoal (YAL) -2.06% and Whitehaven Coal (WHC) -2.21%

- Gold stocks once again the superstars. Westgold (WGX) +12.50% a shining light having been set free from Metals Ex (MLX) -3.82%. Large cap golds also performed well with Newcrest (NCM) +3.31%, Resolute Mining (RSG) +5.44% and Evolution Mining (EVN) +4.35%.

- Healthcare more green than red. Cochlear (COH) +1.,55%, Resmed (RMD) +1.02% and CSL +0.70% better whilst Ramsay Health Care (RHC) -1.23%, Sonic Healthcare (SHL) -1.03% and Pacific Frowns (PSQ) -3.47%.

- IT and telcos still out of favour with Senetas (SEN) -8.00%, Wisetech Global (WTC) -3.28%, Altium (ALU) -1.83% and Telstra (TLS) 1.37-%. Both Vocus (VOC) -1.96% and TPG Telecom (TPM) -1.13% continue their slide as did Superloop (SLC) -2.18%.

- Speculative stock of the day: Ram Resources (RMR) +100% after it announced plans to acquire a majority interest in an advanced Irish zinc project. The historic Keel project includes two main mineralised horizons over 1km in length.

- Chien du jour: Mobile Embrace (MBE) -46.67% after meeting market expectations for earnings in 1H 2017 but full year guidance was lowered. A review has been out in place and cash conservation is being prioritised as the group looks to 2018. Not a good look and over 120m shares traded.

CORPORATE NEWS

- Macquarie Group (MQG) -1.42% slightly underwhelming operational update with forecasts for FY17 broadly in line with last year. $2.1bn in sights according to consensus. Group capital surplus stood at $3.7bn. Nothing exciting here for the market hence the disappointment.

- Transurban (TCL) +6.36% raised its full-year dividend guidance after higher earnings from its Australian and US roads boosted interim net profits by 42% to $88m. The company said it now expected to pay out a dividend of 5cTransurban will pay a first-half dividend of 25c.

- Invocare (IVC) -1.14% will shut down its funerals business in California after two years, concluding the operations won’t hit break-even by a target of mid-2018. The funeral company with 33% of the Australian market will keep its crematorium open in eth US despite the move toc lose California. It acquired the business in 2014 for US$2m. Hardly a huge outlay.

- Western Areas (WSA) +1.16% after intersecting nickel at its first drilling prospect at Cosmos Complex. Results included an upper zone of 17m@1.33% Ni from 100m

- Kathmandu (KMD) +0.55% expects to report a profit of $NZ9.9 million ($A9.5 million) for the six months to January 31, topping its previous guidance that profit would be in line with the $NZ9.4 million ($A9.0 million) achieved in the first half of 2015/16. Healthy same store sales growth in their largest market, rigorous cost control and working capital efficiency are apparently the key.

ECONOMIC NEWS

RBA decision: No change to rates. As expected.

Commentary:

- The improvement in the global economy has contributed to higher commodity prices, which are providing a boost to Australia’s national income.

- Headline inflation rates have moved higher in most countries.

- The economy is continuing its transition

- The outlook continues to be supported by the low level of interest rates.

- The Bank’s inflation forecasts are largely unchanged.

- Borrowing for housing has picked up a little, with stronger demand by investors.

- Sustainable growth in the economy and achieving the inflation target over time.

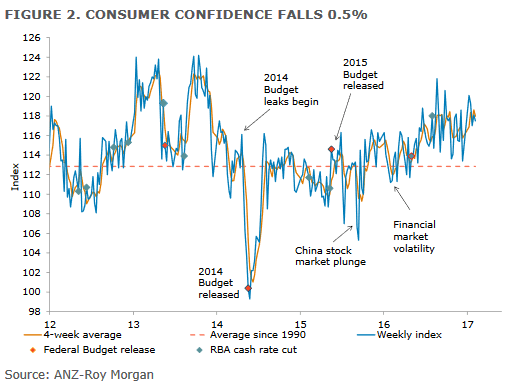

- Consumer confidence fell slightly by 0.5% to 117.5 in the week ending 5th February, partially unwinding last week’s 0.9% rise.

- Wages growth accelerated in the construction industry in January, even as new slowed further, the latest Performance of Construction Index shows.

- Across the ditch, New Zealand central bank governor Graeme Wheeler said he won’t seek a second term and will step down when his first ends in September.

BOND CORNER

Thought I’d park the new motor outside the office this afternoon.

ASIAN NEWS

- The most-active rebar on the Shanghai Futures Exchange climbed 2.2% to 3165 yuan ($US461) a tonne, having closed down 6.8%on Monday when it slipped to the weakest since January 10 at 3062 yuan a tonne. Iron ore on the Dalian Commodity Exchange was trading up 2.4% at 620.5 yuan ($US90).

- All State-owned enterprises will complete “corporatisation reform” within this year, the Economic Information Daily said. China is pushing to overhaul its 131.7 trillion yuan ($19 trillion) state sector, the government is prompting its firms to set up boards and corporate structures to open them up to private capital.

EUROPE AND US

- Amazon is contemplating a robot run store with only three staff members. Sounds a little like Bunnings mid-week.

- Paris is trying to woo the City of London to the City of Romance. The French authorities however do not anticipate being able to displace London as the financial centre which serves the EU, and say they believe Britain will remain the global financial hub of the continent. “When was the last time you took your partner off for a weekend in Frankfurt?” asked Valérie Pécresse, President of Paris Region in London last night. Or maybe someone else peut-être?

And finally…………….

A man comes home to find his wife of 10 years packing her bags. “Where are you going?” demands the surprised husband. “To Las Vegas! I found out that there are men that will pay me $500 cash to do what I do for you for free!” The man pondered that thought for a moment, and then began packing his bags. “What do you think you are doing?” she screamed. “I’m going to Las Vegas with you… I want to see how you’re going to live on $1,000 a year!”

A little boy says, ‘Dad, I’ve heard that in some parts of Africa a man doesn’t know his wife until he marries her.’ ‘Son,’ says the dad. ‘That happens everywhere.’

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com