ASX 200 picks itself up after an uncertain open to close 32 points higher at 5653.2 Predictable. Miners and energy stocks doing well. Banks lag as did industrials. Asian markets still mostly closed for Lunar New Year with Japan up 0.55%. AUD 75.65c and US Futures up 10.

STOCKS AND SECTORS

- Miners were the driver today as USD fell on Trump comments with BHP +1.65%, RIO +0.54% and Fortescue Metals (FMG) +2.25%, a six-0.55%year high, after brokers played catch up with the upgrades on production numbers.

- Base metals stocks rose but the enthusiasm wasn’t there. Oz Minerals (OZL) +1.67%, Sandfire Resources (SFR) -0.46%, South32 (S32) +1.09% and Western Areas (WSA) +1.22%

- Gold stocks back in fashion as Trump trade unwinds. Evolution Mining (EVN) +1.88%, Newcrest Mining (NCM) +0.70% and Saracen Minerals (SAR) +2.83%

- Energy shares positive with Woodside (WPL) +1.39%, Origin Energy (ORG) +1.55% and Whitehaven Coal (WHC) +2.46%. Standout was Senex Energy (SXY) +7.14% bringing the SXY back with a new substantial shareholder EIG.

- Banks and financials in a turnaround day after initial losses with the Big Bank Basket well off its lows for the day at $173.90. Insurers moved ahead as QBE Insurance (QBE) unchanged Insurance Australia (IAG) +1.04% and Suncorp (SUN) +1.15% all did well. Home and car owners face a 4% hike in their insurance bills this year apparently, helping the sector today. Wealth managers continue to find few friends with Perpetual (PPT) -1.35%, Henderson Group (HGG) -1.96% and Magellan Financial Group (MFG) -0.38%

- Industrials once again dominated by confession season and profit results. Telstra (TLS) +1.4% had a rare day in the sun today as did Mantra Group (MTR)+5.17%. Consumer discretionary stocks seeing red led by pizza maker Domino’s (DMP) -4.05% as the tech story unwinds across the IT sector. IT Stocks struggled under the weight of expectation and sagged. Carsales (CAR) -1.82%, Technology One (TNE) -1.17%, Hansen Tech (HSN) -2.07% and Aconex (ACX) -0.66%. Staples better. Woolworths (WOW) +1.99% and Wesfarmers (WES)+1.49%. Fairfax Media (FXJ) +5.88% responded well to stories today in the media that a US fund is looking at the Australian assets.

- Healthcare stocks struggled with the exception of CSL +0.91%, whilst Bio techs on the nose on US FDA uncertainty. Clinuvel Pharma (CUV) -3.11%, Sirtex (SRX) -1.11%, Mesoblast (MSB) -0.62% and Viralytics (VRL) -0.51%. Ansell (ANN) -5.68% as rubber prices have screamed ahead recently weighing in margins.

- Speculative stock of the day: Interesting no standouts today. Some big movers like Adavale Resources (ADD) +72.73% but on very thin volume. Seems the punters are playing in the big end of town with Woolworths (WOW) +% proving popular.

CORPORATE NEWS

- OFX -23.95% A new CEO after barely six months in the job for Richard Kimber and a profit downgrade with EBTDA for the year ending June 30 “now expected to be between $27.5m and $28.5m with statutory net profit of at least $19 million

- GBST (GBT) -16.88% on a profit warning ahead of its results 14th Company said that EBITDA for the full year would now be in the region of $12m for the full year, compared to $17.2m in the prior corresponding period. GBST said its recurring licensing fee revenue in the UK had increased and Syn~ “has exciting prospects in Asia and North America

- GUD Holdings (GUD) +3.81% HY net profit from continuing operations up 412% to $22.5m. Reaffirms guidance provided at annual general meeting for a full year underlying EBIT of around $85m. Outlook remains positive.

- REA Group (REA) -0.38% has sold its European businesses to private equity investor Oakley Capital with the final profit yielding $161.6 million including completion adjustments.

- Senex Energy (SXY) +7.14% has confirmed it has a new best friend in EIG Global Energy Partners. EIG has taken the bulk of a $55m placement of shares by Senex, or about 12.6%, and already owns a 2.7% stake bought on the market earlier. EIG’s track record of $US23bn of investments includes major US names such as LNG player Cheniere Energy and Chesapeake Energy, and oil rig supplier Sete Brasil.

- Wisetech Global (WTC) +8.33% had a great bounce after announcing the purchase of a German customs solutions provider, znet group for EUR6.0m over 5 years.

ECONOMIC NEWS

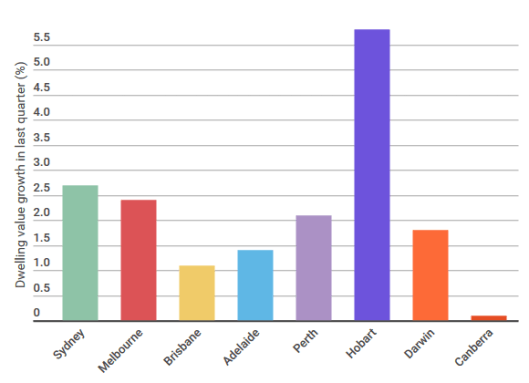

- House prices continued to climb fast in January with Sydney and Melbourne recording the strongest growth, Corelogic’s January Hedonic Home Value Index shows. Sydney posted a 1% rise in dwelling values while Melbourne rose 0.8%.

Go Hobart

- New Zealand has announced a general election for September 23rd. Seems it takes a long time to rustle up the voters.

New Zealand economic numbers today

- Jobless rate rose to 5.2% from 4.9%; estimate was drop to 4.8%

- Employment increased 0.8% q/q; expected 0.7% gain

- Participation rate rose to record 70.5%; forecast 70.2%

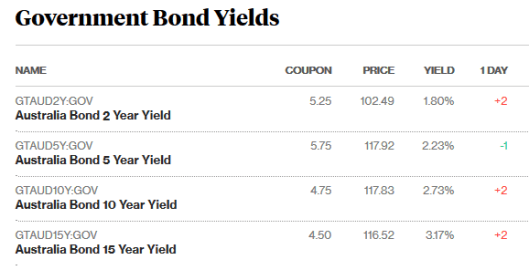

BOND CORNER

ASIAN NEWS

- The Chinese purchasing managers index was 51.3 in January, compared with a median estimate of 51.2 and 51.4 in December. The non–manufacturing PMI was at 54.6 versus 54.5 in December.

EUROPE AND US

- Apple has reported a bigger-than-expected rise in iPhone sales for the holiday quarter, driven by strong demand for the latest version of its iPhone7. Apple sold 78.29m iPhones in the first quarter ended December 31, up from 74.78 million last year, marking the first quarterly growth in iPhone sales in a year.

- Another night of Trump policy lotto ahead no doubt with eyes on the FOMC minutes. Drug companies are celebrating as moves to lower prices. Telecomms are also happy as mergers are back on the cards it seems as new regime may look kindly on consolidation.

- Shell has exited its North Sea assets in a GBP2.4bn sale. Would expect the stake in Woodside to be on the chopping block very soon. Shell results Thursday. Shell chief executive Ben van Beurden is preparing to withdraw completely from as many as 10 countries, selling off assets in a bid to rebalance its portfolio after the costly acquisition of gas giant BG Group last year.

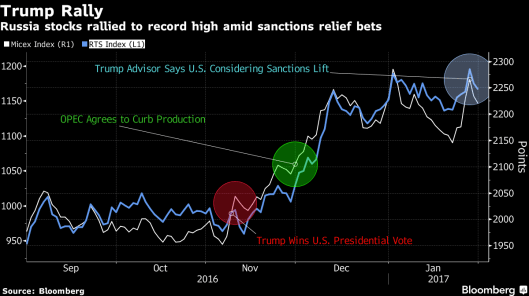

- So, if sanctions are eased on Russia who wins. Well the Russians But who could also be affected. Tasmanian Salmon perhaps? Norway’s salmon industry was a big casualty of the tit for tat sanctions with a EU ban in Russia. This may have given Tassal (TGR) a look in. Sanctions being lifted may also affect the dairy market too. More competition as EU companies and US allowed in.

And finally………..

Little boy gets home from school and says:

“Dad, I’ve got a part in the school play as a man who’s been married for 25 years.”

His Dad replies:

“Never mind Son. Maybe next time you’ll get a speaking part!!”

A dwarf goes to a very good but very busy doctor and asks:

“I know you are busy but do you treat dwarves?”

The doctor replies:

“Yes but you will have to be a little patient”.

A Yorkshireman’s dog dies and as it was a favourite pet he decides to have a gold statue made by a jeweller to remember the dog by.

Yorkshireman: “Can tha mek us a gold statue of yon dog?”

Jeweller: “Do you want it 18 carat?”

Yorkshireman: “No I want it chewin’ a bone yer daft bugger!”

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com