ASX 200 fell another 41 points to 5621 as Trump and profit warnings upset the bulls. Could have been worse after touching 5606. Big miners, banks and telcos suffer. Asian markets subdued with Japan still open and down 0.8%. AUD rising slightly to 75.64c and US futures unsettled again down 47.

Manic Monday has given way to terrible Trump Tuesday.

STOCKS AND SECTORS

- Banks and financials dropped again today with QBE Insurance (QBE) +1.21% the only bright spot on takeover speculation. Wealth managers slid with K2Asset Management (KAM) -6.25%, Henderson Group (HGG) -2.45% and Macquarie Group (MQG) +0.13% rose slightly though. The Big Bank Basket fell to $173.80 as Westpac Bank (WBC) -0.88% the worst of the bunch. The big four banks will face a fresh round of parliamentary questioning in March, with a banking inquiry announcing another round of hearings. Expect more bank bashing to kick off.

- REITs mildly positive led by a recovery of Servcorp (SRV) +4.13%, Lendlease Corp (LLC) +1.37% and Mirvac Group (MGR) +1.00%.

- Industrials remain on the nose. Domino’s Pizza (DMP) -1.93%, Flight Centre (FLT) -1.19% and WPP AUNZ (WPP) -4.50%. Both Wesfarmers (WES) -1.20% and Woolworths (WOW) -1.24% fell too. Tassal Group (TGR) -3.35% also took to profit taking after the great run last week. Select Harvest (SHV) -3.12%.

- Miners fell hard across the board. BHP -2.63%, RIO -1.70%, Iluka Resources (ILU) -3.08% and Independence Group (IGO) -3.83%. Base metal stocks in the dog house, Syrah Resources (SYR) -6.10%, Orocobre (ORE) -4.95% and Western Areas (WSA) -3.92% and Alumina (AWC) -1.27%

- Gold stocks a little mixed Newcrest (NCM) +0.37%, Oceanagold Corp (OGC) +4.67% with Dacian Gold (DCN) -3.32% and Perseus Mining (PRU) -2.90%.

- Energy stocks took a beating with Santos (STO) -0.25% but others fared badly. Woodside (WPL) -2.14%, Origin Energy (ORG) -2.21% and Paladin Energy (PDN) -3.85%. WorleyParsons (WOR) -3.61% and Liquefied Natural Gas (LNG) -1.72%

- Healthcare dominated by the IVF stocks with Virtus Health (VRT) -17.71%, Monash IVF (MVF) -10.03% and Amadeus Ltd (AHZ) -8.00%. Pathology and others also came in for selling pressure. Sonic Healthcare (SHL) -1.75% and Ramsay Health Care (RHC) -0.39%

- IT sector once again under serious pressure with Wisetech Global (WTC) -3.23%, Nextdc (NXT) -3.14 %and Aconex (ACX) -2.58%. Telecom stocks also continued to fall Telstra (TLS) -1.19%, Hutchinson Telecom (HTA) -8.75% and Vocus Group (VOC) -2.18%.

- Speculative stock of the day: Innate Immunotherapies (IIL) +58.97% continuing to ride high on big volumes as US investors warm to the company and its MS treatment. The company lead drug will complete a double blinded placebo phase 2B trial in April. Potential market is US$7bn. The company has a market cap of $280m.

CORPORATE NEWS

- Virtus Health (VRT) -17.71% issued a profit warning today as cut price IVF clinics affected margins and volumes. Volumes fell 7.2% in the December half especially in NSW where volumes fell 19%.

- Iluka Resources (ILU) -3.08% said it expects a net loss of between $220m and $230m for 2016. The outlook for its markets was positive, with the company expecting an improvement in the titanium dioxide feedstock segment as well as moderate growth for zircon.

- Graincorp (GNC) +0.11% has sold its 60% stake in Allied Mills to Pacific Equity Partners for $190m.

- Sirtex (SRX) in a trading halt today as news emerged of a class action against the company based on breaches of its ‘continuous disclosure obligations’. Not a good look when CEO Gilman Wong sold more than 25% of his holdings in October.

- Fortescue Metals (FMG) +2.78% once again confirmed it is a class act with export guidance repeated and even a possible upgrade. The company shipped 42.2m tonnes in the December quarter 4% down on the previous quarter. The company also updated its unit costs to US$13 a tonne with an average C1 cost of US$12.54 WMT.

- Credit Corp (CCP) -3.04% reported a net profit of $25.2m on revenues of $129.1m with earnings per share (EPS) coming in at 53.2c. The profit and revenue were up 19% and 15% over the prior corresponding period, with the group reconfirming guidance for full year profit between $53-$55m, up around 15% to 20% on the prior year. At 16 times earnings the stock is not cheap.

- Clydesdale Bank (CYB) -1.05% in Australia to announce its UK results with an 80% local shareholder base. Reaffirming guidance was not enough it seems. The bank reported a first quarter trading update that it increased the size of its mortgage book at an annualised 4.4% in the three months to December 31. Deposits had grown almost 5% in the quarter, the bank said. Net interest margin (NIM) was stable at 222bps in the quarter. The bank also said it had yet to see any negative impact from Brexit.

- Navitas (NVT) -6.14% reported underlying EBITDA growth of 8%. Unfortunately, the company flagged flat 2017 earnings and hit a one year low in the process. Net profit totalled $53.3m in the six months through December, up on $45.1m a year ago. An interim dividend of 9.4c a share, slightly below a payout of 9.6c a year ago.

ECONOMIC NEWS

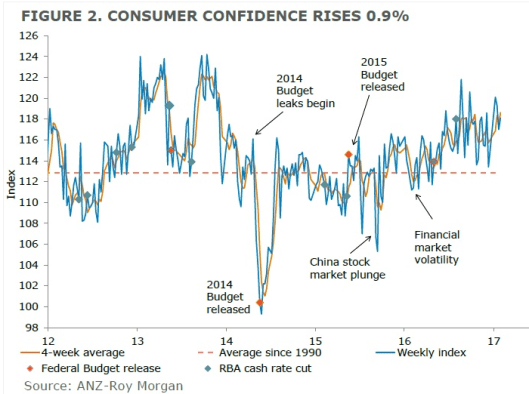

- After posting a 1.9% fall last week, ANZ-Roy Morgan Consumer Confidence rose 0.9% to 118.1 this week. The rise was primarily driven by a bounce in confidence in current financial and economic conditions.

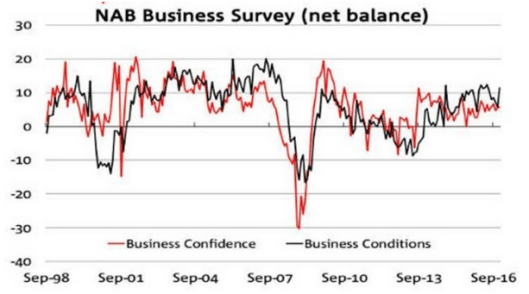

Business confidence rose to near pre GFC levels according to the NAB Business survey. The survey pointed to a surge to 11 points to December from 6 in November. Well above the long-term average.

- Private credit rose a stronger than expected 0.7% in December, or 5.6% over the year.

- NZ head bean counter Graeme Wheeler has said he will make an announcement about his future ‘fairly soon’.

- The Future Fund beat its target in 2016 with a return of 7.8% after shifting cash to infrastructure and private equity. The fund cut its cash allocation to 19.7 per cent, from 22.1 in the last quarter, due to a falling Australian dollar.

- About 7%of Australian mortgage holders have little or no real equity in their homes, a report by Roy Morgan Research says.

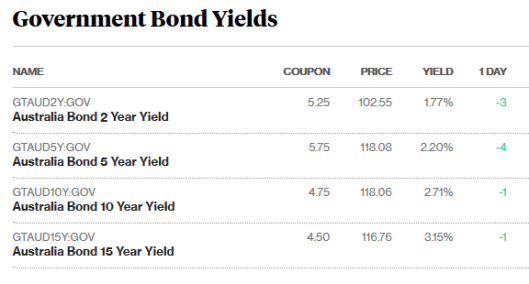

BOND CORNER

ASIAN NEWS

- The Bank of Japan(BOJ) has kept monetary policy steady and roughly maintained its upbeat price forecasts, signalling a steady economic recovery will help accelerate inflation towards its 2 per cent target without additional stimulus.

- The BOJ raised its economic growth outlook for financial year 2017 to 1.5% (from 1.3%) and maintained the 0.1% interest it charges on a portion of the excess reserves that financial institutions park with the central bank.

EUROPE AND US

- Troubling signs again from the US as Trump has fired his Attorney General who had defied the recent bans. Sally Yates an Obama administration holdover, was ousted hours after she told Justice Department staff that Trump’s directive was inconsistent with the agency’s “solemn obligation to always seek justice and stand for what is right.”

- The City of London lobby group which vehemently opposed Brexdit has now done a reverse pike with a twist and said it is “unprecedented opportunity” for the UK to develop a powerful new set of trade and investment policies. “The CityUK is a strong believer in the potential opportunities that the UK’s departure from the European Union will offer.”

- Fitbit will cut more than 100 jobs as its financial woes continue, reflecting an ongoing pessimism in the wearables market. The company will cut 6% of its workforce, 110 jobs globally, as part of a bid to save US$200m.

And finally…..

Anyone seen this guy…used to have some opinions and courage but sadly gone missing in action.

Seems we are just saddled with this bloke!

Seems such a shame!

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com