ASX 200 rose 28 to 5429 as resources well off their highs at the close. RBA stays chilled for the summer. Financials and resources still the power house as industrials try hard. Asian markets firm with Japan up modestly 0.44% and China up 0.07%. AUD barely moved the needle at 74.50c and US Futures down 13.

STOCKS AND SECTORS

- Resources all the rage again but well off their highs. BHP +1.19%, RIO +0.90% and Fortescue Metals (FMG) +0.80%. Metals Ex (MLX) +12.07% bounced back after the gold side of the company relisted Westgold (WGX) unchanged. Base metals generally better but not spectacular OZ Minerals (OZL) +0.99% and Sandfire (SFR) +1.00% enjoying the copper bounce.

- Energy stocks firm again buoyed by the Origin Energy (ORG) +2.49

- % on news of the divorce and Woodside (WPL) unchanged and Santos (STO) +0.91%

- Goldminers mixed to weaker Dacian Gold (DCN) -21.55% returned following the capital raising

- Industrials perked up as the day wore on. Consumer discretionary stocks rallied hard. Aristocrat (ALL) +1.40% Tatts Group (TTS) +1.45%, G8 Education (GEM) +5.36% and A2Milk (A2M) +1.83%. Battered and bruised again Bellamy’s (BAL) -2.29% Healthcare mixed with Regis Healthcare (REG) +13.15% Estia Health (EHE) +11.46% and Japara Healthcare (JHC) +11.90% all benefitting from a sector allocation. Reva Medical (RVA) -5.66% not quite so much fun along with Impedimed (IPD) -5.66%.

- Consumer staples on the nose with Woolworths (WOW) -1.28% and Wesfarmers (WES) -0.40%.

- IT still struggling as the high PEs unwind. Technology One (TNE) -2.13%, Hansen Technologies (HSN) -3.31% and Wistech Global (WTC) -0.18%. Telstra (TLS) +0.20% stuck with TPG (TPM) -1.17% easing and Spark NZ (SPK) +0.88% better.

- Financials posted good gains with the Big Bank Basket (BBB) +52c to $166.10. QBE Insurance (QBE) +2.43% continue the rally on lower bonds and higher USD. Other insurers also in demand with Suncorp (SUN) +1.03% and Clearview Wealth (CVW) +1.67%. Wealth managers better with the exception of Magellan Fund Management (MFG) -1.25%. BT Investment (BTT) +1.77% and Macquarie Group (MQG) -0.21%

- Speculative stock of the day: Triton Minerals (TON) +56.25% returned to trading with a new focus on a graphite project in Mozambique. The company has been recapitalised with cash at the bank of $8m bouncing back from administration.

CORPORATE NEWS

- Origin Energy (ORG) +2.49% has announced it plans to spin off its conventional oil and gas assets in a separate company valued at potentially $1.8bn to reduce debt. The new CEO Frank Calabria hopes that the deal will be done early in 2017. Better to be born lucky than clever sometimes. Since Calabria has taken the reins from Grant King the stocks has rallied 30%.

- Surfstitch (SRF) -3.03% co-founders Lex Pedersen and Justin Stone and two non-executive directors will step down from the board with new chair Sam Weiss appointing Harry Hodge from Quicksilver Europe as a non-executive

- Adani has promised not to use 457 visas at its $21.7bn Carmichael Mine in central Queensland.

- UGL +0.32% after substantial shareholder Allan Gray has accepted the bid from CIMIC (CIM) +0.49% of 315c a share. Gray’s acceptance will push CIMIC over 75%, allowing it to extend the bid a further two weeks beyond Friday’s deadline.

- BHP +1.19% has won a historic bid to partner with Mexican state oil company Pemex in a joint venture to develop a potentially lucrative deep water field in the country’s untapped Gulf waters.

- In some bad news potentially for Telstra (TLS) +0.20% the Productivity Commission has recommended scrapping the Universal Service Obligation Fund. This would give other telcos a boost at TLS expense if the $197m levy is scrapped. The review found the program outdated and opaque, and predicted it would become largely redundant once the national broadband network (NBN) was complete.

ECONOMIC NEWS

The Reserve Bank has kept its cash rate on hold. No big surprise and the board will not meet again until February. Chilling for summer.

Some key points from the statement:

- The global economy is continuing to grow, at a lower than average pace.

- Labour market conditions in the advanced economies have improved over the past year.

- Commodity prices have risen over the course of this year, reflecting both stronger demand and cut-backs in supply in some countries.

- Low interest rates have been supporting domestic demand and the lower exchange rate since 2013 has been helping the traded sector.

- The economy is continuing its transition

- Global headline inflation rates have increased recently.

- Conditions in the housing market have strengthened overall.

- Considerable supply of apartments is scheduled to come on stream over the next couple of years, particularly in the eastern capital cities.

- Growth in rents is the slowest for some decades.

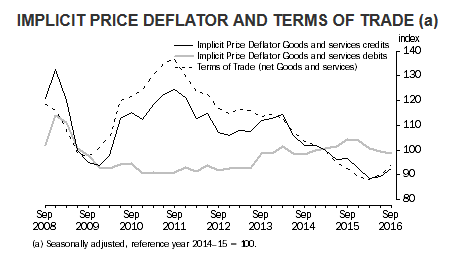

The current account deficit was $11.3bn in the September quarter, down sharply from $15.9bn in the previous quarter, but net exports will still subtract 0.2% from GDP or more than expected. Terms of trade on goods and services rose 4.5% in the quarter, fuelling nominal growth.

- Government spending for consumption dipped 0.2% in the third quarter to an inflation-adjusted $77.64bn.

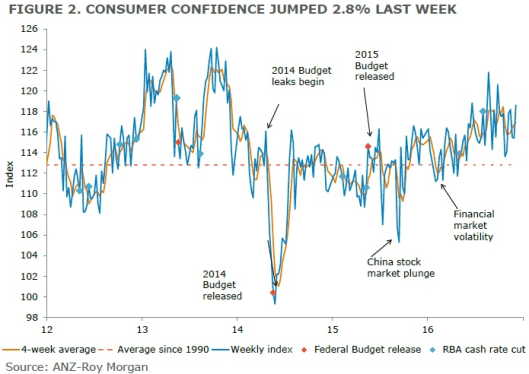

- ANZ Roy Morgan Consumer Confidence rebounds 3.2pts to 118.6.

BOND CORNER

- 5-Year bonds yielding 2.31% down 4 bps

- 10-year bonds down 5bos to 2.81% yield.

- The recent rout in global bond markets has shrank the world of negative yields by US$2.5 trillion.

ASIAN NEWS

- Dalian iron ore up another 3.5% at 657.5 yuan ($US88).

- Zinc futures in Shanghai have jumped more than 4%.

EUROPE AND THE US

- Despite the resignation of Italian PM Renzi, the Monet dei Paschi is being readied for a bailout. All eyes on the Italian banking sector and the possible bailouts in the wings. He warned: “Turning our backs on open markets would be a tragedy, but it is a possibility.”

- Bank of England chief Mark Carney has warned that the UK could suffer its first lost decade since 1860. Carney said it was “incredible” that real incomes had not risen in the past 10 years.

- UK Chancellor is promising the City a smooth Brexit.

- Xi Jinping to visit Davos for World Economic Forum as the first Chinese leader to attend elite gathering in sign of Beijing’s global ambition.

TODAY’S ANNOUNCEMENTS

And finally…………

The guys were on a bike tour. No one wanted to room with Mick, because

He snored so badly. They decided it wasn’t fair to make one of them

Stay with him the whole time, so they voted to take turns.

The first guy slept with Mick and comes to breakfast the next morning

With his hair a mess and his eyes all bloodshot.

They said, “Man, what happened to you? He said, “Mick snored so loudly,

I just sat up and watched him all night.”

The next night it was a different guy’s turn. In the morning, same

Thing, hair all standing up, eyes all bloodshot.

They said, “Man, what happened to you? You look awful! He said, ‘Man,

That Mick shakes the roof with his snoring. I watched him all night.”

The third night was Bill’s turn. He was a tanned, older biker, a man’s

Man… The next morning he came to breakfast bright-eyed and

Bushy-tailed.

“Good morning!” he said. They couldn’t believe it.

They said, “Man, what happened?” He said, “Well, we got ready for bed.

I went and tucked Mick into bed, patted him on the arse, and kissed him

Good night on the lips. Mick sat up and watched me all night.”

With age comes wisdom.

And just as a bonus..Clarence is a big Roilling Stones fan and loves teh new Blue and Lonesome album..and this clip is so cool…hope you enjoy it.

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com