End of Day

ASX 200 falls 44 points to 5400 in low volume sell off as Italian PM resigns. Banks, healthcare and consumer stocks in the sellers’ sights. Miners a small bright spot. Asian markets sold off aggressively with Japan down 0.83% and China down 1.76%. AUD 74.52c and US futures down 34.

STOCKS AND SECTORS

- Bank and financials showed signs of fatigue and slipped around 1.4% in the big four with the Big Bank Basket back to $165.60. Wealth managers also sold off with Macquarie Group (MQG) -1.90%, BT Investment (BTT) -2.10%, Magellan Funds (MFG) -1.58% after reporting FUM of $44.865bn up from $42.237bn.

- Resources held relatively firm with South32 (S32) +2.47%, Rio Tinto (RIO) +0.98%, BHP +0.64% and Alumina (AWC) +5.92%. Lithium weakened with Orocobre (ORE) -5.79%, Galaxy Resources (GXY) -7.37% and Pilbara Minerals (PLS) -5.83%.

- Energy stocks weaker although Santos (STO) +0.69% tried hard to rally whilst Woodside (WPL) -1.91% and Oil Search (OSH) -1.56%

- Gold miners missed out on the enthusiasm with Resolute Mining (RSG) -3.33% and Gold Road (GOR) -3.88%.

- Industrials weaker across the board with Healthcare seeing losses, CSL -2.49%, Ramsay Heath (RHC) -2.13% and Nanosonics (NAN) -5.85% and Impedimed (IPD) -8.23% in big trouble. IT struggling to find any support with Praemium (PPS) -4.88%. Data#3(DTL) -8.28%, Wisetech Global (WTC) -0.89% and Nextdc (NXT) -3.11%. Telcos down too with Telstra (TLS) -0.81%, Vocus (VOC) -3.56% and Chorus (CNU) -3.18%

- Utilities were one small bright spot following the Duet (DUE) +16.60% bid with APA Group (APA) +1.28%, Spark Infrastructure (SKI) +2.28% and Ausnet Sevices (AST) +1.73%

- Consumer stocks feeling the pain with rising interest rates and rising fuel prices Webjet (WEB) -5.58%, Harvey Norman (HVN) -3.70%, Domino’s Pizza (DMP) -4.08%, Baby Bunting (BBN) -2.92% and Breville Group (BRG) -4.19%

- Speculative stock of the day: Athena Resources (AHN) +140.00% after entering a binding term sheet with Brilliant Glory for the sale of the Byro Project.

CORPORATE NEWS

- Bellamy’s Australia (BAL) -4.23% back in the spotlight today as the analysts have now started to downgrade their numbers. Horse? Bolted? Anyway analysts seem to think that the problems at BAL are not spilling over to A2Milk (A2M) -%. No use crying really. Morgan’s has drastically re-rated their target share price to 755c from 1665c previously.

- DUET (DUE) +16.60% shares hit all-time highs after an unsolicited, highly conditional non-binding approach from Li Ka-Ching’s Cheung Kong Infrastructure at 300c a share worth around $7.3bn.

- Bapcor (BAP) +1.84% has lifted its takeover bid for New Zealand’s Hellaby Holdings by 9% to NZ360c, to try and bring a quick resolution to a takeover battle running since September,

ECONOMIC NEWS

- NZ PM John Key has followed Italian PM Renzi and announced his resignation. By a live Facebook feed. Times have changed.

- Westpac and National Australia Bank have both raised interest rates. NAB will raise its standard variable rate for housing investors by 0.15% to 5.55%. Westpac will raise interest rates for all its customers with interest-only home loans by 0.08%.

- The 0.8% increase in inventories was more than double the expected consensus gain and will mechanically add 0.2% to Q3 GDP growth. Mining profits rose 5.8% over the quarter, while profits of ex-mining firms were down 0.7%. Estimated growth in wages and salaries was 1.2 per cent for the quarter and 2.9% for the year, the ABS said.

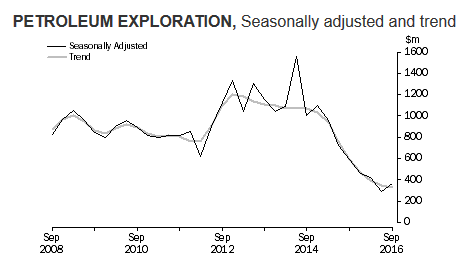

- Looks like the weak oil price has taken its toll on our oil and gas sector in terms of exploration. The trend estimate for total petroleum exploration expenditure fell 6.9% (-$23.9m) to $324.5m in the September quarter 2016. Exploration expenditure on production leases fell 35.7% (-$18.3m)

BOND CORNER

- Australian 10-year yields have risen 2bps to yield 2.80%

- 5-year yields around 2.31%.

- Father of ‘Irrational Exuberance’, Alan Greenspan, is now more worried about debt than equity despite valuation of both looking stretched.,

ASIAN NEWS

- China’s top securities regulator has denounced leveraged acquirers of listed companies as ‘robbers’.

- On the Dalian Commodities Exchange, iron ore futures in Dalian are trading up 4.5% at Rmb606.5 per metric tonne. Coking coal is up 2.2 per cent at Rmb1,292 per tonne, having risen as much as 2.7%.

EUROPE AND THE US

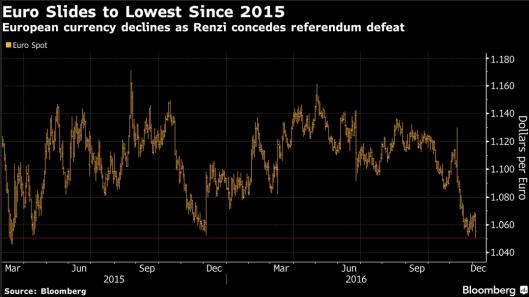

- That holiday in Europe just got cheaper with the euro falling to a near two-year low.

- The ‘no’ vote in Italy has spooked markets. PM Renzi has fallen on his spada as expected now we wait to see how it falls from here but the EU has been weakened by this result and with elections in France, Holland and Germany next year we are going to hear a lot more about the euro project. The problem is the EU is split between south and north and one currency makes one region rich but the other poor. It also throws into doubt any rescue of Monte dei Paschi.

Southern Europe’s Zombie banks

- In the UK the government published its infrastructure–investment pipeline, detailing a record GBP500bn of projects scheduled to be undertaken in the coming years. Private finance makes up more than half of the pipeline to 2020-21, helping to deliver projects ranging from transport and broadband to flood defences and housing, Macquarie Group should be a beneficiary here.

- PEOTUS Trumptold his 16.6m Twitter followers that he wouldn’t be told by China who he should or shouldn’t talk to. Things get real on January 20th.

And finally……………

Hung Chow calls in to work and says, “Hey, boss I not come work today, I really sick. I got headache, stomach ache and my legs hurt. I not come work.” The boss says, “You know Hung Chow, I really need you today. When I feel like this I go to my wife and tell her give me sex. Makes everything better and I can go to work. You try.”

Two hours later Hung Chow calls again: “Boss, I do what you say and I feel great. I be at work soon. You got nice house.”

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com