ASX 200 drops 12 points to 5430 as healthcare stocks take a hit, financials in the green. Quiet trading again dominated by AGM news and profit updates. Healthscope and Sky City wounded. Asian markets ease slightly with Japan down 0.02% and China 0.17%. AUD 76.32 whilst US futures down 29.

For the week we are down 3 points..says it all really.

Main issues for Australia seem to be some relaxation of gun controls and same sex marriage since Malcolm in the Middle won in July.

As my old buddy Bill, said marriage and shotguns- is why I am where I am now!! Thanks Bill.Great call.

STOCKS AND SECTORS

- Financials had some spring in their step today as the big four banks basket pushed up to $161.30 with Westpac (WBC) +0.90% the best on rumours of a sale of one of its funds businesses. Eclipx Group (ECX) +4.18% continued higher with Medibank Private (MPL) +2.73% also proving popular once more. REITS weaker again though Stockland (SGP) -1.53% and Mirvac (MGR) -1.86% although Lendlease (LLC) +1.03% recovered after clarification of a slide from the investor day yesterday suggesting a meagre margin of 6% on apartment sales. It is 19% in reality.

- Resources mainly positive with BHP +0.83% despite news from the boys in Brazil. South32 (S32) +1.16% Fortescue Metals (FMG) +1.39% and Sims Metal (SGM) +2.91%. Gold stocks back in profit taking mode after bullion falls. Newcrest (NCM) -2.34% and Saracen (SAR) -3.14% together with Evolution Mining (EVN) -3.80%.

- Energy stocks weaker though Karoon Gas (KAR) +7.32% continuing to show a clean pair of heels given its high cash position, corporate appeal and JV with Woodside (WPL) -0.91% potential.

- In the industrials, healthcare had a day in the casualty ward after Healthscope warned on lower hospital revenue. Primary Health Care (PRY) -2.23%, Ramsay Health (RHC) -5.88% and Cochlear (COH) -1.96%. Seems the demographic, defensive sector arguments are unravelling as governments look to rein in costs around the world.

- Bellamy’s (BAL) +4.60% had another strong day building on recent gains. With other consumer stocks also doing well. Woolworths(WOW) +1.53%, Blackmores (BKL) +1.16% and Treasury Wine (TWE) +0.97%. Crown Resorts (CWN) +1.58% recovered a little but have had a bad week to say the least, REA Group (REA) -2.41% still sliding as once again the end of the property market is splattered all over the papers every day.

- Speculative stock of the day: Greenpower Energy (GPP) +38.46% after announcing trials were completed with the OHD fertiliser significantly increasing crop yields. GPP has partnered with Thermaquatica to covert coal into liquid fertilisers with successful trials at Monash University.

CORPORATE NEWS

- Healthscope (HSO) -18.77% surprised the market today with a trading update coinciding with the AGM Not good news as hospital revenues have been flat and sub optimal. The company is now expecting a flat year on year result unless something changes. Ramsay Health Care (RHC) 5.88-% also caught the disease with its AGM to come.

- Qantas (QAN) -0.31% says it will keep a tight focus on costs and ensure capacity matches demand as intense competition on international routes means travellers are benefiting from cheaper fares. intense competition on international routes means we’re seeing air fares below where they were 12 months ago.

- Santos (STO) +0.52% has told shareholders that it has started to hedge its oil production to reduce the impact of volatile prices. A rise in LNG sales has helped Santos to more than offset the impact of softer prices in the three months to September, spending has again been down in line with the depressed commodity market. Santos lifted revenues in the last quarter to $US650m, 11% higher than a year earlier, boosted by a 31% jump in volumes.

- More woes for casino operators as Sky City Entertainment (SKC) -12.19% updated the market with lower revenue growth from Auckland. The company also said it did not have any employees in China. Revenues fell 0.3% in New Zealand, 8.2% in Australia, and 20.2% in the important International Business (VIP) gambling business.

- BHP +0.83% AGM today and news that 22 people have been charged in Brazil over the Samarco dam disaster. The company rejected the charges and also announced that long-time Chairman Jac Nasser will be stepping down in 2017.

- Coca-Cola Amatil is taking the knife to costs, adding another $100m to its original cost savings target of $100m. At today’s investor day CEO Watkins said CCA was targeting low single digit EBIT growth from developed markets of Australia and New Zealand, double-digit EBIT growth from developing markets Indonesia and Fiji, and double-digit EBIT growth from alcohol and coffee and food processor SPC.

ECONOMIC NEWS

- Seems that blocking the Chinese from buying Ausgrid has come at a cost. The sale yesterday to IFM and Australian Super for a value of $20.8bn is well below the $25.1bn that Hong Kong-based Cheung Kong Infrastructure Holdings offered in August. Sure NSW Treasurer will be sending Morrison the bill.

ASIAN NEWS

- Hong Kong suspended trading as Typhoon Haima bore down. It’s the second time this year the Hong Kong markets have closed because of weather disruption. Business was halted on 2, when Typhoon Nida hit the city.

- Nintendo has unveiled its new console in a three minute youtube clip, Switch and they have, with the stock sold down nearly 6%. It’s a hybrid machine that can be played at home and on the go. Release date March 2017.

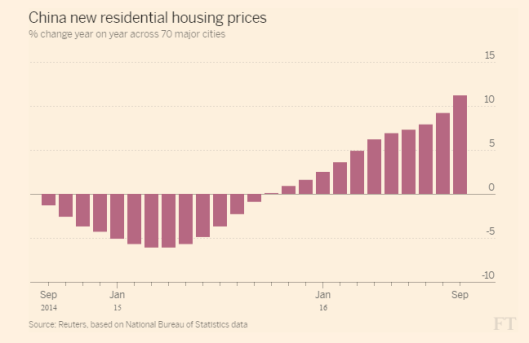

- New-home prices, excluding government-subsidised housing, gained last month in 63 of the 70 cities the government tracks, down from 64 in August, the National Bureau of Statistics said. New-home prices in Beijing fell 3.7% in the first half of October from September. Prices in the financial hub of Shanghai fell 2.5% in the first two weeks of October, after jumping 3.2% in September.

- Chinese sovereign bonds rallied with the 10-year yield edging close to a decade low. Property measures and moves to curb leverage seem to be weighing on the outlook.

EUROPE AND THE US

- Microsoft is back. The once daggy computing company is now the king of cool and has recaptured its mojo after shifting its focus to the cloud. The stock pushed through an all-time high on results after hours. The company’s shares have doubled since August 2013. Microsoft said its gross profit margin from its commercial cloud business was 49 per cent, much lower than its traditional software business, but still attractive and growing quickly.

- Global wine output is set to decrease by 5% compared with last year to 259.5m hectolitres (mhl), one of the three smallest volumes since 2000. Australia is forecast to produce 5% more or 12.4mhl and New Zealand output is poised to surge 34%to 3.1mhl. Italy is the world’s largest wine producer with an expected 48.8 mhl.

- Trade deals are dead according to EU President if the Canadian trade deal collapses. Seems it is hard to do a deal with the EU. Something that the UK will find in around 30 months.

- Merkel warns of ‘rough going’ ahead as Hollande points to ‘hard negotiation’. Phoney war is coming to an end.

- In shock news it appears many genuine Apple chargers and cables on Amazon are in fact counterfeit knock offs. Apple has filed a lawsuit against one seller on Amazon and has ‘zero tolerance’ for these products.

And finally……………with sincere apologies as its a bit lewd and un-pc…but clever and funny so there! Look away children!!!

Have a great weekend

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com