ASX 200 rose 25 points to 5435 as across the board buying propelled us closer to 5450 and a potential break. Telcos, Golds and merger mania gripped investors. Asian markets mildly positive on Chinese GDP data. Japan up 0.11% and China up 0.05%. AUD weakens to 76.66c and US futures up 23.

- The anniversary of Black Monday on 19th October 1987 passed with barely a mention today. Where were you?

STOCKS AND SECTORS

- Resources were generally better with Independence Group (IGO) +5.70%, Western Areas (WSA) +8.98%, RIO +0.26%, South32 (S32) +4.86% and gold stocks also doing a good job today. Newcrest (NCM) +3.27%, Evolution (EVN) +3.23% and Saracen Mineral (SAR) +6.52%. BHP -0.75% was the fly in the ointment following operational updates.

- Coal stocks continued to prove the critics wrong. Whitehaven (WHC) +6.73% seem to be on a mission as did New Hope (NHC) +5.85%. However, the huge run in Yancoal (YAL) -30.91% came to an abrupt halt today.

- Energy stocks mildly positive with Caltex (CTX) -1.95% bucking the trend on concerns on buying the Petrol station business from Woolworths (WOW) +1.64%

- Industrials mainly positive with the gaming and wagering sector doing well on the Tatts Tabcorp Casinos though threw snake eyes with Crown Resorts (CWN) -3.00%, Sky City (SKC) -2.92% and Star Group (SGR) -2.19%.

- Telcos were big winners today as Telstra (TLS) +1.19% bounced off the 500c level and Vocus (VOC) +4.58% and TPG Telecom (TPM) +1.33%.

- In the China facing food and health stocks we saw good gains for A2Milk (A2M) +4.35%, Costa Group (CGC) +2.74% and Select Harvest (SHV) +1.60%

- Financials mixed though despite positive leads from overseas in the banking sector. Macquarie Group (MQG) +0.76% rode the Goldman Sachs results wave though Challenger Financial (CGF) -2.26% coming in for some profit taking. The insurance sector perked up led by QBE +1.90% and Insurance Australia (IAG) +0.90%.

- Speculative stock of the day: Carnarvon Petroleum (CVN) +30.00% following a historic bedout sub-basin flow test at the ROC-2 well. Flow rates and pressure exceeded expectations. The ROC-2 project is in the North West Shelf off the coast of WA.

CORPORATE NEWS

- Tabcorp (TAH) +3.48% Tatts Group (TTS) +15.88% finally announced the long awaited merger which has now morphed into a quasi-takeover. TAH is paying 0.8 shares and 42.5c to TTS shareholders and the company will undergo a $500m share buy back when the dust settles. The ACCC may have something to say about the tie up given its dominant position locally but given this merger was on the cards for so long it beggars belief the two have not run the wedding plans past the vicar.

- Cimic (CIM) +2.56% promoted deputy chief executive Adolfo Valderas to CEO and reported an 11% rise in third quarter net profit to $148.5m. Third quarter results, included a 7% rise in cash flow from operating activities before interest, finance costs, taxes and dividends to $532.9m.

- Charter Hall (CHC) -1.21% has pulled the pin on the float of its new $1.12bn Long WALE REIT after failing to get sufficient investor interest.

- Origin Energy (ORG) -0.88% was in the spotlight with 16.5% of shareholders voting against the equity performance package of outgoing CEO Grant King. You have to feel a little sorry for a man who built ORG up from a $700m market cap to $10bn in his 16 years at the helm. The package at $1.35m wouldn’t even buy a modest home in Sydney.

- BHP -0.75% released its operational report with no mention of any record at all in the report for the first time in a long time. The company left its full year production guidance unchanged, with September quarter oil output down 15%, copper down 6% and steaming coal off 4% but with iron ore output steady and coking coal production edging ahead by 1%.

ECONOMIC NEWS

- Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from +0.15% in August to +0.58% in September.

ASIAN NEWS

China Data Dump

- The economy grew 8% quarter-on-quarter, the National Bureau of Statistics said, in line with market forecasts and compared with revised 1.9% quarterly growth in the second quarter. The annual rate is now 6.7% in line with the authority’s script.

- Real estate investment growth ticked up to 5.8 % in January to September, a slight increase from 5.4 % over the first eight months.

- Consumption contributed 71% of GDP growth in the first three quarters of the year.

- Industrial production, which expanded by 6.1% over the year to September, disappointing estimates of 6.%.

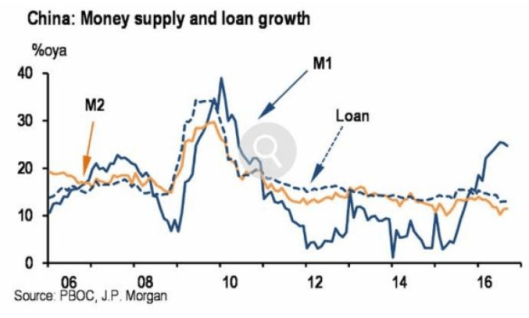

- Chinese banks extended 22 trillion yuan (U$240 billion) in new loans in September, well above expectations.

EUROPE AND THE US

- In Hollywood news Leonardo DiCaprio is cooperating with Malaysian authorities on the wealth fund scandal following question marks on funding sources for the Wolf of Wall Street.

- Advocates of Brexit will be pointing fingers at Brussels as the long awaited Free Trade agreement with Canada (CETA) seems to have hot a stumbling block over Belgian farmers concerns in a region known a Wallonia. The agreement has been in negotiation since 2009. Opponents fear that CETA will be used as a model to push through an even more controversial EU-US trade deal, called TTIP, much of which remains to be negotiated.

- The average person in Europe works 19% less than the average person in the U.S. That’s about 258 fewer hours per year, or about an hour less each weekday.

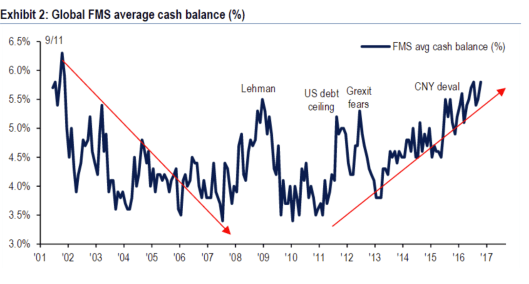

- Global fund managers have pushed their cash balances to 5.8% of their portfolios in October, up from 5.5% last month, matching levels not seen since the aftermath of the Brexit vote.

And finally…..we were all so young!!!!

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com