ASX 200 down 43 points to 5373 as support gives way ahead of NFP numbers and Labor day. Banks, telcos and healthcare stumble. Asian markets slightly weaker again with Japan down 0.01% and China down 0.13%. AUD 75.57c and US futures down 7.

A miserable post result week comes to an end with the market now going ex-dividend. For the week the ASX 200 lost 2.5%. Will we get Rod Stewart or Neil Young’s version of ‘Tonight’s the Night’?

Gloom or boom?

STOCKS AND SECTORS

- Banks particularly unloved after the Canberra shenanigans last night. Westpac Bank (WBC) -1.12% and ANZ -0.81% the worse of the four. REITs also suffered with Dexus Property (DXS) -2.06%, Scentre Group (SCG) -1.21%, Westfield (WFD) -0.88%. Insurers too folded with IAG -0.54% and QBE Insurance (QBE) -0.51%. Wealth managers too felt unloved with Platinum Asset Management (PTM) -1.69%.

- Industrials showed pockets of resistance against the sellers but it was hard to find. Monadelphous (MND) +4.19%, Downer EDI (DOW) +1.86% and SG Fleet Group (SGF) +1.11%. Infigen Energy (IFN) +6.04% was another to buck the carnage.

- IT stocks managed a few gains too with Hansen Technologies (HSN) +1.56% and Altium (ALU) +1.80%.

- In other industrials Slater and Godown (SGH) +15.07% showed signs of life not though Fantastic Holdings (FAN) -4.90% but Vita Group (VTG) +4.07% following broker upgrades.

- Healthcare horrors continue with Estia Health (EHE) -5.97% now down over 40% and the company founder exiting. Seems the pressure on healthcare costs is starting to take its toll. Generic maker Mayne Pharma (MYX) +3.92% doing better. Cheaper alternatives will come to the fore.

- Resources were a green island in a red sea today. Base metals and gold shone through. Regis Resources (RRL) +2.84%, Evolution Mining (EVN) +4.67% and OceanaGold Corp (OGC) +4.30% the stars. BHP +0.05% stood still but RIO +0.89% performed slightly better.

- Energy was not a good place to be as the crude oil price falls ahead of OPEC deliberations at the end of the month. Whitehaven Coal (WHC) +4.84% though continue to be in demand on the higher coking coal price. Stanmore Coal (SMR) -13.04 after a late sell off killed at 5% rally on their $1 purchase of Isaac Plains coking coal mine in Queensland last year.

- Speculative stock of the day: BBX Minerals (BBX) +95.65% after results from the Juma East drilling showed exceptional gold grades of 24.76g/t from the bottom 49m of hole JDE-006.

CORPORATE NEWS

- Macquarie Atlas Road (MQA) Macquarie Group (MQG) -0.84% announced that MQG would receive 12.645m shares as its performance fee. The bank has sold down 10% or 53m shares at 532c. They still hold 11%. MQA resumes trading Monday.

- TPG (TPM) -1.52% has just announced plans to buy spectrum in Singapore, the first step in becoming an international mobile network operator.

- Alumina (AWC) +5.77% has settled a dispute with joint venture partner US giant Alcoa. The two companies agreed to terminate a court fight that had threatened to delay Alcoa’s plan to spin off its plane and car parts business, which is now set to go ahead by the end of this year. The agreement removes a poison pill in the AWAC joint venture.

- Patties Foods (PFL) +0.60% after the court approved the scheme of arrangement.

ECONOMIC NEWS

- Guy Debellehas been appointed as the new deputy governor of the RBA. Debelle has run the RBA’s financial markets division since 2007.

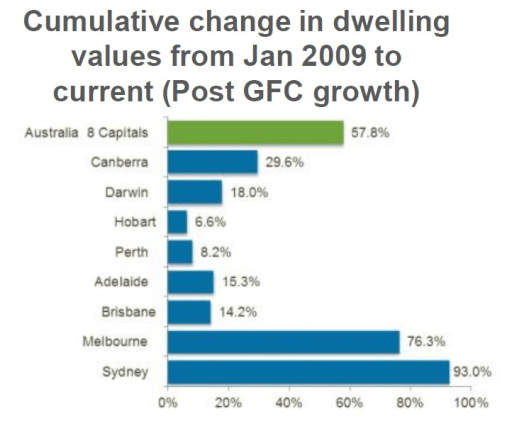

- CoreLogic’s Hedonic Home Value Index, released monthly, rose by a solid 1.1%, led once again by strong gains in Sydney and Melbourne.

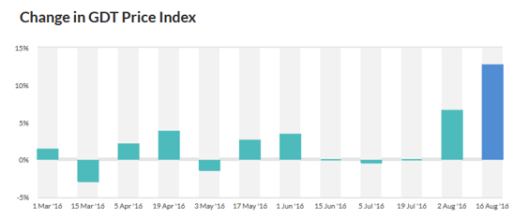

- Signs of life in the Dairy pricing at the last auction.

ASIAN NEWS

- Samsung Note 7 phones have been pulled from sale domestically due to a faulty battery which catches fire. Bad timing for the company only a few days before the Apple 7 launch on September 7th. Looks like the forecast of 11m Smartphone sales of Note 7 will be a huge ask given reputational damage and the delayed release now.

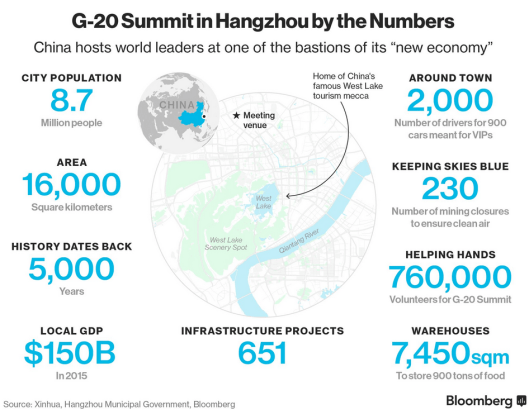

- G-20 meeting this weekend. Just as well the government does not have a vote then.

EUROPE AND THE US

Slightly positive opening in store for European markets after yesterdays falls.

- Apple is set to send money home next year as it faces higher tax bills around the world. Apple currently has US$215bn sitting in foreign bank accounts. Tim Cook has called the EU ruling ‘total political crap’. Seems the White House has now weighed in saying it could be unfair to American taxpayers because the company might be able to claim the cost as a tax deduction in the US. Starting to get surreal.

- The IMF has suggested that Brexit fears have been well and truly overdone. “In the United Kingdom, a range of recent monetary and other policy measures by the Bank of England will support the economy and thereby mitigate downside risks.”

- UK manufacturing activity recorded its biggest month-on-month increase in a quarter of a century in August.

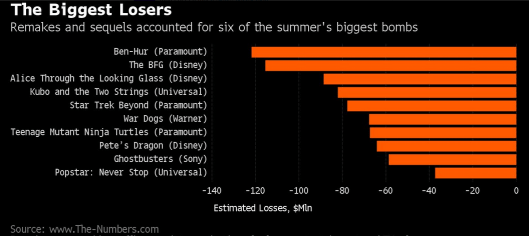

- Meanwhile in Hollywood, Disney is not having a great time with its current movie offerings.

And finally……………

Doctor: “I’m sorry but you suffer from a terminal illness and have only 10 to live.”

Patient: “What do you mean, 10? 10 what? Months? Weeks?!”

Doctor: “Nine.”

Clarence

XXXX

XXX

Get a Global take on things at http://www.ntmarkets.com