ASX 200 closes up 3 to 5535 after another narrow tight range today. CBA responsible for around 12 points of the loss after going ex-dividend. Energy and Materials the standouts. Results the focus. Asian markets higher, Japan up 0.90%, HK up 0.233 and China up 0.02%. AUD easier at 76.76c and US futures up 22.

Another day of duck paddling furiously whilst staying calm on the surface. Plenty to be concerned about underneath. Bearing in mind though that the CBA dividend knocked 12 points off the index, it wasn’t too bad a show. Plenty of volume too.

STOCKS AND SECTOR

- Banks were better with the Commonwealth Bank (CBA) -2.58% after going ex-dividend 222c. The other three improved slightly as a high profile fund manager suggested they were cheap.

- Materials were led by BHP +3.26% reacting positively after it chucked the kitchen sink into the write-downs yesterday. Base metal stocks were also better. South32 (S32) +2.97%, Magnis Resources (MNS) +7.2%, Sandfire Resources (SFR) +2.74% and Independence Group (IGO) +1.51%.

- Energy stocks pushed higher again as oil went through $46 in Asian trade. Oil Search (OSH) +2.44%, Woodside (WPL) +2.35% and Whitehaven Coal (WHC) +4.08%.

- Gold stocks eased back across the board. Newcrest (NCM) -5.47% collapsed as did Evolution (EVN) -6.42% following results and Resolute Mining (RSG) -8.62%.

- Industrials were mixed and concentrated on results and reactions. A super supreme effort from Domino’s Pizza (DMP) +8.08% bouncing hard to a record price, Fletcher Building (FBU) +4.93% led builders higher with Boral (BLD) +1.00% slightly better too.

- In the IT space profit taking reigned Aconex (ACX) -2.48%, Freelancer (FLN) -3.73% and Touchcorp (TCH) -6.28%.

- Speculative stock of the day: Aus Tin Mining (ANW) +100.00% after production of tin concentrate from the Granville project commenced in Tasmania. The company is only the second listed tin producer on the ASX. Tin is up 25% this year on declining global tin supply.

CORPORATE NEWS

- Evolution Mining (EVN) -6.42%. Profit up by a record 114% to $226.9m. AISC of $1014 with 2 cents dividend unfranked. Gold production increased 84% to a record 803,476 oz.

- Fletcher Building (FBU) +4.93%. Benefited from the record levels of residential building which helped fuel a 71% rise in NPAT to NZ$462m ($439m) for 2015-16.

- Aveo Group (AOG) is undertaking a $125m institutional placement to fund its acquisition of the remaining 27% stake in another operator, Retirement Villages Group. Results were also strong with underlying net profit up 63% to $89m. For 2017 and 2018, the company expects to boost earnings per security by 7.5%.

- CSL -5.06% reported a 10% fall in net profit to $US1.24bn, hurt by a $US205.5m loss from the Novartis influenza vaccines business and a $US115m hit from currency swings. The company is also considering another $500m share buyback and will raise capital next year through a private US placement.

- Some things in the market you can take to the bank. QBE Insurance (QBE) -8.33% surprising to the downside is one of those. The company reported a 46% drop in half-year profit to $US265m after falling interest rates and the fallout from Brexit meant it had to discount the value of its assets by $283 million. Cash profit after tax fell 39% to $US287m.

- Stockland(SGP) –1.42% has posted an 8.5% rise in annual profit to $660m with a final distribution of 12.3c for a total of 24.3c for the year.

- Crown Resorts (CWN) +4.51% posted a 22.7% fall in net profits to $406m from $525m, slightly below forecasts of $405m.

- Sonic Healthcare (SHL) +6.19%. FY16 net profit up 30% to $451, in line with guidance and higher than consensus of $432. Revenue up 20%, dividend up 7.3% yoy to 44c.

- Nanosonics (NAN) +0.00% reported its maiden full year net profit of $122,000, which included a 2H profit of $3.4bn. Sales for the full year rose 93% and it was the first full year of positive free cash flow.

- Spotless Group (SPO) -10.57% following news that the proposed sale of it laundry business is now off the agenda.

ECONOMIC NEWS

- Moody’s has reaffirmed Australia at Aaa with a stable outlook. Moody’s said it expected the economy would remain resilient in an uncertain global environment. The budget was also in better shape than that of other countries with AAA ratings.

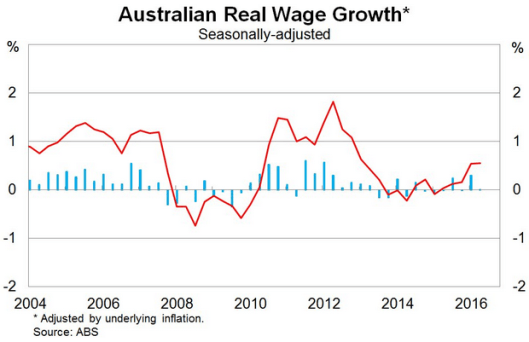

- Wages rose 0.5% over the second quarter to be up just 2.1% over the year, slightly above expectations of 2.0%. Economist have commented that it’s generally a good income – low enough to encourage employment growth but still higher than inflation.

- Industries with fastest annual wage growth: Electricity, gas, water and waste services (up 2.6%) and Education & training (up 2.5%).

- Industries with slowest annual wage growth: Mining (up 1.3%); Administrative & support services and Construction (both up 1.5%); Professional, scientific and technical services (up 1.7%).

ASIAN NEWS

- Japanese yen is about to go to parity with the USD- $1 equals Y100

- The government approved a scheme to link trading on China’s second exchange in Shenzhen with the Hong Kong market.

- Cathay Pacific, Asia’s biggest international airline, reported first-half profit that missed analyst estimates after posting losses from jet-fuel hedges and declining passenger yields due to competition with Chinese carriers.

EUROPE AND THE US

- Cisco Systems, the largest maker of networking equipment, will cut as many as 14,000 employees worldwide, or 20% of its workforce.

- Iceland plans to significantly ease capitol controls for individuals and companies 9 years after the GFC. Investment in foreign currency financial instruments will also be allowed and individuals will be authorised to buy one piece of property abroad each calendar year, irrespective of purchase price.

And finally………………

A wife send her husband an sms on a cold winter evening: “Windows frozen”. The husband send answer back: “Pour some warm water over them”. Some time later husband receives answer from his wife: “The computer is completely stuffed now”.

Where’s the best place to hide a body? Page two of Google.

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com