ASX 200 pushed through 5600 but unable to hold rally. We closed off highs up 25 at 5587. Energy, materials and industrials stepped up to the plate. Asian markets mixed with Japan up 0.11% and China down 1.14%. AUD above 76c with US futures up 73 points.

- ASX Mid cap index is at an 8-year high

- Small Ords is at a 4-year high.

- REITs up 21% in the last six months.

STOCKS AND SECTORS

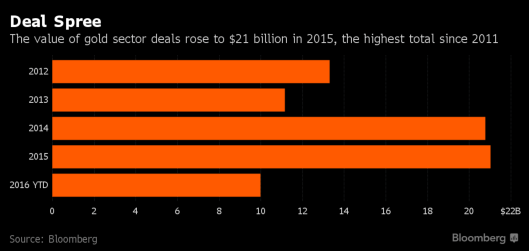

- Gold stocks once again the stars of the show on good results, Diggers and Dealers and an improving bullion price. Resolute Mining (RSG) +16.22%, St Barbara (SBM) +6.98% and Dacian Gold (DCN) +3.13%. Plenty of deals around in the sector too.

- Energy stocks back in the green today after recent weakness. Woodside (WPL) +1.92%, Oil Search (OSH) +2.82% and Caltex (CTX) +2.83%.

- Big four banks a little disappointing but Clydesdale Bank (CYB) +4.04% shooting the lights out. Australia and New Zealand (ANZ) -% with wealth managers positive. Wilson Group (WIG) +3.79% and Euroz (EZL) +2.94% together with Henderson Group (HGG) +1.47%.

- REITS firm with standouts Payce Consolidated (PAY) +18.75% and Lifestyle Communities (LIC) +2.68%

- Industrials were especially firm in mining services with Mineral Resources (MIN) +1.32% and ALS (ALQ) +2.35%. Monadelphous (MND) +4.56%, Decmill Group (DCG) +2.44% and Bradken (BKN) +12.12% continuing to attract heavy buying in the services sector.

- Couple of big movers in the healthcare sector with Mesoblast (MSB) +3.57% improving after a science award and Monash IVF (MVF) +3.7%.

- Some disappointment in consumer stocks, Myer (MYR) -3.37%, Audio Pixels (AKP) -3.83% and RCG Corp (RCG) -1.60%

- Speculative stock of the day: Cassini Resources (CZI) +41.18% has signed a deal with Oz Minerals to develop Australia’s largest copper nickel deposit. OZL will contribute $3m to find a detailed scoping study and can earn up to 70% of the West Musgrave project.

CORPORATE NEWS

- Tabcorp (TAH) -0.41% will acquire INTECQ (ITQ) +29.23 for $115 million in deal that will Tabcorp says will strengthen its gaming services division and add $20 million to underlying earnings. TAH will pay 715c a share for INTECQ (formerly known as EBet).

- Dominic Stevens has been appointed the new CEO of the ASX +0.24%.

- Capitol Health (CAJ) -18.75% Has suspended its dividend. Executive Director Peter Lewis is stepping down from his executive and board roles. Reported net loss expected to be $3.2m. Revenue up 42%. Core radiology EBITDA $23m up slightly on pcp.

- Fairfax (FXJ) -1.90% After a $989m write down. Australian Metro Media will record a $484.9m pre-tax impairment, Australian Community Media will book a $408.8m pre-tax impairment and the company’s New Zealand business will report a $95.3m pre-tax impairment. The company will also separate the Domain numbers when it next reports.

- Northern Star (NST) +0.76% after an agreement in principle to sell its Plutonic gold mine.

- Paladin Energy (PDN) -9.76% resumed trading after the clarification of its capital raising and divestment of 24% of the Langer Henrich mine.

- Gold Road (GOR) +3.68% is in talks with four parties over the potential sale of a stake in its Gruyere development project in Western Australia.

- BC Iron (BCI) -3.33% after results after hours with revenue of $151.3m and an EBITDA loss of $7.6m. No additional non-cash impairments to $40m already announced. Expects $13.5-14.5m cash at end of July and no dividend.

ECONOMIC NEWS

- BIS Shrapnel has released its ‘Building in Australia 2016-2031’ National dwelling commencements are estimated to have reached their peak over 2015/16 and will begin to decline from this level in the coming year.

- A survey by ME has found 10% of households expect they will not be able to meet their minimum debt repayments over the next six to twelve months.

- ME’s overall Household Financial Comfort Index, a measure of households’ perceptions of their financial comfort, dropped significantly by 4% to 5.37 out of 10 in the six months to June 2016.

ASIAN NEWS

In Japan

- Japanese manufacturing activity shrank in July at a slower pace than the previous month but new export orders contracted the fastest in more than 3-1/2 years. The IHS Markit/Nikkei Japan Final Manufacturing Purchasing Managers Index (PMI) rose to 49.3 in July, versus a preliminary 49.0 and a final reading of 48.1 in June.

- Pokémon Go fell to third place on Sunday among highest-grossing apps for Apple devices in Japan with the shares slipping today too down 1.7%. An update to the app that rolled out over the weekend wiped out in-game progress of some users.

In China

Uber will merge its China business with Didi the dominant ride-hailing service in the country, according to media reports. The valuation of the combined ride-hailing company is $35 billion.

- The official manufacturing PMI was 49.9 last month, compared with June’s reading of 50 in line with forecasts.

- Non-manufacturing PMI was at 53.9 compared with 53.7 in June.

- Manufacturing PMI from Caixin Media and Markit Economics jumped to 50.6 in July, from 48.6 in June.

- In Caixin PMI report, output rose to 52.1, highest reading since July 2014.

- July gross gaming revenue falls 4.5%, less than 5.5% estimated

- Casino industry’s slump in city extends to 26th-straight month

EUROPE AND THE US

Positive opening expected for European markets

- The Institute of Chartered Accountants in England and Wales believes UK growth will be “just positive” in the three months to September, at 0.1%, following growth of 0.6% between April and June. Business optimism has started to recover after the Brexit vote it says.

And finally………

I saw my mate Charlie this morning, he’s only got one arm bless him.

I shouted – Where you off to Charlie?

He said, I’m off to change a light bulb.

Well I just cracked up, couldn’t stop laughing, then said,

– That’s gonna be a bit awkward init?

– Not really. he said. I still have the receipt, you insensitive bastard.

“Jesus Loves You.”

Nice to hear in church but not in a Mexican prison.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com