ASX 200 rose another 37 points today to 5489 as banks, healthcare, industrials and consumer stocks all did well at the expense of metals and miners. Asian markets were a little weaker with Japan -0.23% and China -0.06%. AUD steady around 75c and US futures up 17.

Stocks and Sectors

- Some good movers today in the industrial space with Aristocrat (ALL) +3.69%, CSL +2.08%, Ramsay Healthcare (RHC) +3.28%, Sydney Airport (SYD) +2.94% and XRO +6.53% the standouts.

- Financials also put in a solid day as sentiment around banks has changed a little. The big four were up around 0.5-1% with the big four basket at $158.,50. Wealth managers and insurers also doing well. QBE Insurance (QBE) +2.14% and Magellan Financial (MFG) +2.95%.

- Hedge funds had covered short positions on ANZ, NAB and Westpac following the May results season, according to Macquarie, while they had increased bets against CBA. ANZ, NAB and WBC saw reductions in their short interest of around 1 to 1.5% from the mid-May peaks.

- Big miners and golds suffered as profit taking continued and the rotation from resources to industrials continued. Independence Group (IGO) -6.37% Western Areas (WSA) -4.80% and Oz Minerals (OZL) -2.51% suffering badly in base metal stocks whilst both RIO -2.02% and BHP -2.92%. One broker has downgraded the sector as the currency tailwind unwinds.

- Energy stocks managed to hold in relatively well considering the falling oil price. Woodside (WPL) +0.51% and Caltex (CTX) +0.53%.

- Domino’s Pizza (DMP) +% showed good gains on the demise of Eagle Boys and the potential to acquire sites and business.

- Speculative stock of the day: Oventus (OVN) +35.71% after debuting yesterday on the ASX put in another spectacular rise.

- IPO watch: Bid Energy (BID) +1733.34% (not a typo) after a $7m capital raise and reverse takeover through Canaccord Genuity. The new company was acquired by Cove Resources and renamed. The company has a platform that it intends to roll out in the deregulated energy markets globally enabling businesses to control their energy spending.

CORPORATE NEWS

- Sydney Airport (SYD) +2.94% after releasing passenger numbers for June. First half numbers of 20m passing through the airport plus big growth numbers in Chinese and US arrivals with 6.7% growth overall and international at 9.3%

- BHP -2.92% following somewhat disappointing iron ore production number and in line oil and copper production. Analysts seem to be a little underwhelmed with the current BHP strategy and the oil business seems to be running down at a great pace than some thought. attributable profit in the June 2016 half year is expected to include additional charges of up to US$175 million.

- St Barbara (SBM) -3.5% after quarterly record gold production. Total gold production was 386,564 oz with June quarter production of 92,033 oz. for production of 245,000 to 250,000oz at an AISC of $850-$910oz. Simberi is forecast to produce between 95,000 to 105,000 oz at a AISC of between $1000-$1200oz.

- ResApp (RAP) +4.69% announced that the Massachusetts General Hospital was the first US hospital to sign up for their trail.

- Cimic (CIM) -19.01% fell the most in 12 years as analysts questioned the accounts of the 71% owned Spanish group. NPAT up 3.1% yoy for the half year and EPS up 5%, boosted by the share buy-back. There was a 31.4% fall in revenue. FY 2016 NPAT guidance was confirmed at $520-580m.

ECONOMIC NEWS

- The Household, Income and Labour Dynamics in Australia survey (known as HILDA) tracks the same 17,000 Australians each year to find out whether their particular living standards have improved.

- Beginning in 2001, the survey finds that the typical household was better off each year until 2009, with the typical real household disposable incomes climbing from $57,704 to $76,264 – a gain of 32%. However, that is where it has ended given the GFC and subsequent headwinds. We are now 0.7% worse off than we were in 2009. Household wealth has also been slipping, sliding 3.3 % since 2010.

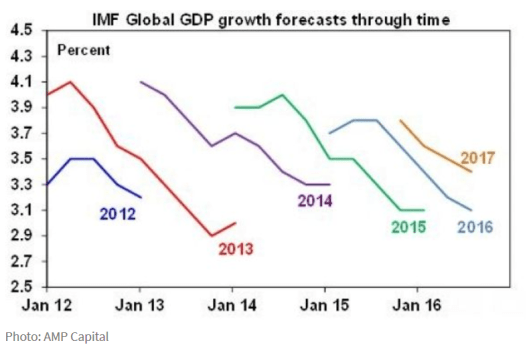

A good chart from Capital Economics showing the IMF forecasts for global growth have constantly been revised down and almost always are too bullish.

According to the Bank of America-Merrill Lynch monthly survey of Investment firms 40% are expecting ‘helicopter money’ as they view current monetary settings as too restrictive. Caution still prevails it seems with cash levels continuing to build in July, to average 5.8% of assets, which is the highest in around 15 years. The BoA strategists believe that the unwind of the short banks trade is dependent on a European bailout or in and more stimulus from Japan.

ASIAN NEWS

- Indian drugmakers Aurobindo Pharma and Glenmark Pharma said they received final regulatory approval to sell generic versions of AstraZeneca top-selling cholesterol pill, Crestor, in the U.S.

- Hong Kong Index is poised to enter an official bull market rising around 20% from its January low.

EUROPE AND THE US

‘All the way with Donald J’ as Trump is confirmed as the official Republican nominee for POTUS. Current betting

Clinton $1.40 (was $1.28) Trump $2.90 (was $4.00)

- German PPI for June: +0.4% (est. 0.20%) PPI YoY Jun: -2.2% (est. -2.40%)

- According to some reports VW knew about the emissions issues back in 2006.

- European Union’s top court backed EU guidelines designed to prevent taxpayers from footing the bill for bailing out stricken lenders. The overnight decision is a blow for the Italian banks that are in desperate need of recapitalisation.

- Boris Johnson continues to back down on pre Brexit vote promises as he signals that the aim to get immigration down below 100,000 is now off the table.

And finally………

A nun in the convent walked into the bathroom where mother superior was taking a shower. “There is a blind man to see you,” she says. “Well, if he is a blind man, than it does not matter if I’m in the shower. Send him in.” The blind man walks into the bathroom, and mother superior starts to tell him how much she appreciates him working at the convent for them. She goes on and on and 10 minutes later the man interrupts: “That’s nice and all, ma’am, but you can put your clothes on now. Where do you want me to put these blinds.”

Clarence

XX

Get a Global take on things at http://www.ntmarkets.com