ASX 200 slid 54 points to 5228 into the close as political uncertainty and banks once again the negative. Miners mixed on profit taking. RBA leaves rates on hold as AUD fell back to 75.06c after disappointing export numbers. Asian markets retreated as commodities fell. Japan down 0.67% and China up 0.14%. US Futures down 38.

A slow day with sellers gaining the upper hand as uncertainty on the election result continued. Banks were once again the target for the sellers as APRA warned on the need for more capital and the threat of a Royal Commission now hangs silently over their heads. Once again volumes were ion the light side as school holidays and US markets closed for Independence Day took their toll.

Mining stocks were once again the relative shining beacon of light in the markets today. Gold stocks slipped slightly on profit taking and we saw mixed results in base metal stocks after they were hit by falls in commodities in the Asian session.

STOCKS AND SECTORS

- Financials and banks once again sold off. The big four bank basket is now back testing the $148 level where it traditionally bounces from. UK facing Henderson Group (HGG) -2.41% and BT Investment (BTT) -4.48% continued to slide.

- Miners holding in just RIO -0.02% and Fortescue Metals (FMG) -1.54% with base metal stocks giving up recent gains on profit taking. Western Areas (WSA) +3.35% doing well on the 8- month high nickel price and some short covering.

- Lithium stocks took a breather today. Orocobre (ORE) -0.2%, Lithium Australia (LIT) -1.85% Galaxy (GXY) -3.81% and General Mining (GMM) -3.64%.

- Mantra Group (MTR) -7.65% a casualty today as a broker moved to downgrade to neutral.

- Healthcare stocks are in limbo land as we await a new government. CSL -1.02% with modest losses on pathology and radiology groups like Sonic Health (SHL) +0.14%, Ramsay Healthcare (RHC) -0.24% and Sigma Pharma (SIP) -2.54%.

- Consumer stocks suffering with Harvey Norman (HVN) -3.94% and Wesfarmers (WES) -1.29% and Woolworths (WOW) -0.96%.

- Speculative stock of the day: AusTin Mining (ANW) +57.14% reported high grade copper targets centred on historic high grade workings at Mt Cobalt. Rock chip samples of up to 1.66% Co.

CORPORATE NEWS

- Domino’s Pizza (DMP) -2.52% has rejected claims by one broking analyst that a rise in penalty rates would hit profits by up to 24%. DMP apparently pays a lower base rate than its rivals together with no weekend penalty rates. The current enterprise agreement expired three years ago and the company has been aware of the changes it needs to make and has been working on them with the SDA, the union involved.

- Jumbo International (JIN) +21.54% after announcing a significant increase in profits driven by growth in customer numbers and a good run of jackpots drawing fresh clients.

- Pilbara Minerals (PLS) -6.29% updated the market on their recent offtake agreement.

- Evolution Mining (EVN) +1.07% after results from their JV with Emmerson (ERM)+% showed Edna Beryl to be a high grade prospect in NT. 6m at 13.2g/tonne including 3m at 15.7g/tonne from 120m. Further results from the 3900m drill campaign will follow in the next few weeks.

- Metals Ex (MLX) -4.46% slid following excellent recovery from their 3rd processing campaign at the Cannon Mine as 2,095 oz Au were produced from transitional ore.

- Australian Vintage Group (AVG)-7.14% following a trading update and a $1m hit to the bottom line on currency moves in the UK on the Brexit vote.

ECONOMIC NEWS

RBA has left monetary settings on hold again. Surprisingly no major focus on Brexit in the minutes.

From the minutes:

“Taking account of the available information, the Board judged that holding monetary policy steady would be prudent at this meeting. Over the period ahead, further information should allow the Board to refine its assessment of the outlook for growth and inflation and to make any adjustment to the stance of policy that may be appropriate”.

For the whole media release of the minutes.

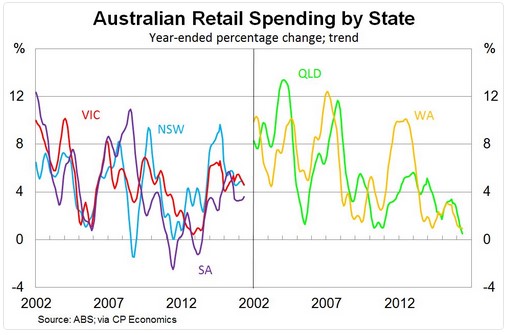

- Retail sales rose just 0.2 % in May, seasonally adjusted, despite the Reserve Bank of Australia’s rate cut that month. The growth rate was slightly better than April’s revised 0.1%, but fell short of economists’ forecasts of 0.3%. Some had predicted a sharper pick-up.

- The trade balance remains in the red with a deficit of $2.2 billion in May, following a deficit in April of $1.7 billion. Economists had expected a deficit of $1.5 billion in May. Exports rose 1.0% in the month, while imports were up 2.0%, the Australian Bureau of Statistics said.

- Earlier this morning ANZ-Roy Morgan consumer confidence index edged down 0.9 % last week, with levels slipping after reaching a two and a half year high.

APRA updated a study that showed the common equity tier 1 (CET1) capital ratio of Australia’s major banks were now in the top quartile of banks internationally – a key target set by the 2014 financial system inquiry.

IN ASIA

- The China Caixin services purchasing managers’ index (PMI) climbed to 52.7 from 51.2 in May, marking the fastest increase in 11 months.

- Silver slid 2.3%, ending a two-day jump of 8.6% that marked its steepest rally in five years. Traders taking profits as the market appears overbought short term.

- Palm oil dropped as much as 2.1% in Kuala Lumpur, snapping a three-day advance.

EUROPE AND THE US

- Bank of England governor Mark Carney will speak tonight. He is expected to use his speech to talk about the risks following the Brexit vote. Some analysts believe that Carney will try to get banks to lend more – possibly by reducing the new capital buffer introduced three months ago.

- Seems the UK will outsource its negotiations with Brussels over their Brexit, as calls for private consultants grow, who have experience in trade negotiations. That will not be cheap.

- RBS reprivatisation faces a 2-year delay potentially due to Brexit.

- US has now higher oil reserves than Saudi Arabia with 264bn of recoverable oil.

- Seems the Italian Banks are shaping up as the next ‘Not so Flash Point’ as fears grow on bad debts and the limited scope, within EU rules, that the government has to do anything about it.

And finally……………

Will we get our Tony back…or Pyne …or ScoMo ..or will Malcolm in the Middle hang on.

And finally finally…..

An army Major visiting sick soldiers, goes up to one private and asks “What’s your problem, Soldier?”

“Chronic syphilis, Sir.”

“What treatment are you getting?”

“Five minutes with the wire brush each day.”

“What’s your ambition?”

“To get back to the front, Sir.”

“Good man,” says the Major. He goes to the next bad. “What’s your problem, Soldier?”

“Chronic piles, Sir.”

“What treatment are you getting?”

“Five minutes with the wire brush each day.”

“What’s your ambition?”

“To get back to the front, Sir.”

“Good man,” says the Major. He goes to the next bed. “What’s your problem, Soldier?”

“Chronic gum disease, Sir.”

“What treatment are you getting?”

“Five minutes with the wire brush each day.”

“What’s your ambition?”

“To get the wire brush before them two, Sir.”

Have a lovely evening

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com