ASX 200 gives up yesterday’s gains to close on its low at 4765.3 down 55.8 points as banks and financials continue to be plagued by credit concern. Resources and gold shone as Bluescope Steel upgraded its numbers and Santos (STO)+3.61% despite oil volatility. Asian markets weaker again, Japan down 3.15%. US futures +42 points with AUD steady at 71.02

The market had another weak but slightly less chaotic day today as an early bounce was snuffed out by regional market falls. Once again banks bore the brunt of investor selling as Euro woes continued last night with SocGen now Ground Zero.

Good numbers from Bluescope Steel (BSL)+14.16% helped the resource sector and gold was a good place to be today, following the flight to safety. The RIO results were taken relatively well as the company looks to be battening down the hatches to improve the balance sheet, cut debt and capex.

- For the week the index has fallen from 4976 to 4765 a fall of 4.2% as we enter an ‘official’ bear market. Not that it may affect the underlying economy, with only seven of the last thirteen bear markets feeding through into the real economy.

Stocks and Sectors

- Financials were once again the target as the big four slipped. We have trading updates from Australia and New Zealand Bank (ANZ) -2.33% and National Bank (NAB) -1.87% next week but with the market in the mood it is currently in, we will need something special to turn things around. Wealth managers were particularly weak on fears of a continued slump in equities. BT Investment (BTT) -5.9% and Henderson Group (HGG) -7.83% the two biggest losers. Suncorp (SUN) +3.36% was a bright spot following the results yesterday and have reacted well to further examination. Insurers generally were a happier bunch than other financials with AMP -0.39% only slightly off.

- In the industrials most sectors were down. Healthcare gave up the Cochlear (COH) -0.82% inspired gains of yesterday, media was especially weak with Prime Media (PRT) -3.45%, APN News (APN) -2.11%,Ooh! Media (OML) -3.47% and Seven West Media (SWM) -1.88%.

- In resources all eyes naturally on gold stocks as the gold price popped last night. In the winners’ enclosure were Evolution Mining (EVN) +5.05%, Kingsgate (KCN) +43.75%, St Barbara (SBM) +4.41% and Northern Star (NST) +5.31%. Material stocks held relatively steady, BHP -0.98%, RIO -1.27% except for Fortescue Metals (FMG) -4.71%.

- Strange day in the energy sector with the whipsaw on the now infamous UAE ‘tweet’ putting oil back above US$27.50. Santos (STO) +3.61% was the big surprise with maybe some news in the ether driving the stock higher.

- Consumer stocks and high fliers suffered today. Bellamy’s (BAL) -5.0%, Australian Agriculture (AAC)-5.04% and Elders (ELD) -9.09% with Woolworths (WOW) -1.86% and Wesfarmers (WES) -0.75%. In telcos, Telstra (TLS) +0.72% bucked the trend following the outage this week.

- Speculative stocks of the Day: Remember Kingsgate (KCN) +43.75% as it starts to stir in this exuberant bullion market. You know you are in a bull market when Kingsgate goes up.

Corporate News

- Bluescope Steel (BSL) +14.16% a big winner today following an earnings upgrade and a write-up rather than a write-down of assets. The company which officially reports on February 22 has upgraded its earnings by around $50m to $230m. The carrying value of the North Star BlueScope business they acquired from Cargill in October has been raised by $700m.

- Origin Energy (ORG) -1.09% has sold its Mortlake Terminal station for $110m. The agreement is with Ausnet and involves access to Victoria’s electricity transmission network between the Mortlake power plant and the grid.

- RIO -1.27% announced last night that underlying earnings halved to $US4.5 billion last year and it would scrap its ’progressive’ dividend policy after it slumped to a net loss in 2015. It will replace it with a more flexible approach but restated that dividends will not be less than US$1.10 in 2016. Full year dividend for the current period will be US$2.15. So at least they are moving the goalposts slowly. BHP to follow? Capital expenditure budgets have also been cut, from $US5 billion to $US4 billion in 2016, and from $US7 billion to $US5 billion in 2017.

- Baby Bunting (BBN) +0.8% raced out of the pram this morning following a 55% higher profit at $4.3m however a dummy spit quickly took its rattle away and the stock slipped into negative territory before a late rally on the close.

Economic News

Glenn Stevens out today in front of a Senate finance committee. His comments on financial markets ‘dropping their bundle’ were widely reported.

His main points in a long and considered question time were:

- Upbeat on economy.

- Next rate move likely to be a cut.

- Oil decline not only negative but good for consumer spending.

- Markets over-reacting and puzzled as to why.

- China uncertainty continues.

“At least for our banks, to date, there’s no evidence that funding markets are impaired though a little bit of pressure on the cost,” RBA’s Stevens says. “We are travelling fine.”

In Asia

- The South Korean junior market was suspended from trading today for 20 minutes following an 8.2% fall at one stage.

- China will come back online next week after the lunar new year holiday and will have some catching up to do together with a look at new yuan loan numbers and money supply with trade data due Monday.

- Japan’s Topix Index is now down 21% for the year against Shanghai down 22%. Of course China has been closed this week so expect that gap to widen next week.

- Today the Japanese finance minister has raised the prospect of intervention in the currency markets as the yen hit its highest level in 15 months. Looks like he is on the job, “Recent foreign exchange moves have been very rough. I am very nervously watching these moves and will take appropriate steps as necessary.”

- Happy that someone is as the move from BOJ chief Kuroda has seen the yen up 9% since he moved to negative interest rates.

He’s gonna need a bigger boat at this rate.

Europe and US

- All eyes will be on the European banking sector again tonight.

- JP Morgan chief Jamie Dimon has put his money where his mouth is and bought 500,000 shares in the company. He has taken advantage of the 20% fall to spend around US$25m. He did earn US$26m last year and already owns 6m shares.

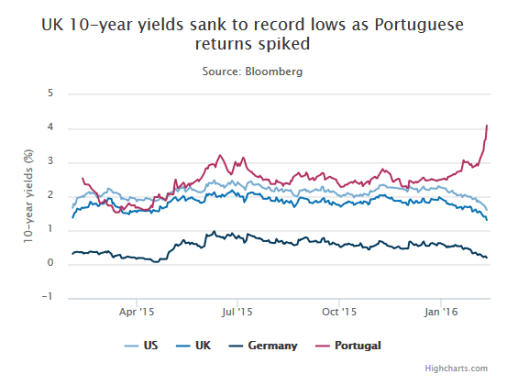

The flight to quality in Euro sovereign debt continues as Portugal starts to blow out.

- Morgan Stanley will pay $3.2bn (£2.2bn) to US authorities to settle claims that it misled investors about risky mortgage bonds sold before the financial crisis.

US markets closed for President’s day Monday.

This from the former chief economist at the IMF.

Enjoy the weekend, the chocolate wheel starts again on Monday.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com