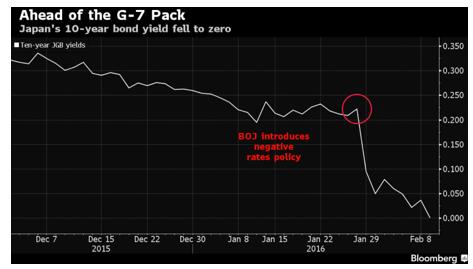

ASX 200 down 143.3 points to 4832.1 on heavy selling as banks and other financials collapse on credit concerns. Japan falls 5.54% on ten year bonds hitting zero whilst other Asian markets remain closed. Dow futures down 121 with AUD 70.37. Big volumes in equities and futures.

Overnight woes in European banks and the US markets weighed heavily today as the ASX 200 fell through the crucial 4900 level and then some. Banks were particularly badly mauled after Bank of Queensland (BOQ) -8.12% updated the market with a quasi-profit warning based on a margin squeeze and higher costs. Credit concerns on the back of lower energy prices and central bank rates have smashed investors’ confidence in banks globally.

Rumours of a large Middle Eastern seller using Australian banks as a proxy for Asian banks and a banking crisis were not helpful. There were few places to hide with only the gold sector showing strength.

Yesterday’s ‘drop and bounce’ was forgotten, today it looked like a big dose of catch up and sheer panic. Seemed that even the pretty girls got hurt in the bus crash today.

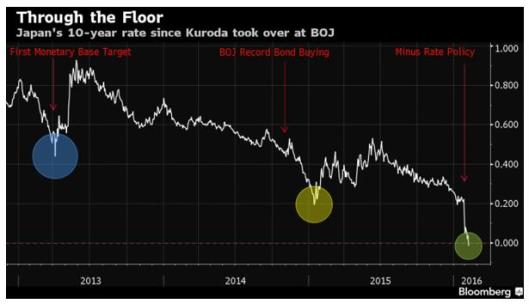

Despite many Asians markets still closed, Japan was open, although probably wished they weren’t given a 5.6% fall as the market came on line. News that the Japanese ten year bonds had hit zero did nothing to instill confidence with it sliding into negative territory. Janet Yellen’s job has got a whole lot harder in the last two months.

It seems that banks are now worried about profitability in a near zero rate environment. Investors though are worrying about defaults and credit conditions.

Tomorrow’s Commonwealth Bank (CBA) -4.6% results are shaping up as a ‘manning the barricades’ moment. Hopefully it will be enough to stem the tide. Bad and doubtful debts the key number.

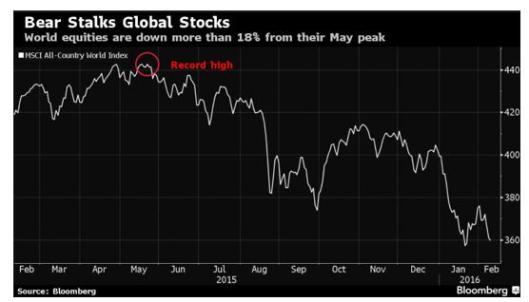

European banks have fallen around 20% since the beginning of the year on concerns of bad debts, falling energy prices and market jitters.

One unintended consequence of the lower oil price is sovereign wealth funds selling share portfolios to fund their economies. Unfortunately, they are also large holders of European banking shares, especially Deutsche Bank Italy’s Intesa Sanpaolu. There are estimates they have sold around US$150bn last year and have another US$200bn to go.

It may well be the ‘Year of the Monkey’ but just at the moment it feels like ‘Year of the Bear’.

Stocks and Sectors

- Gold stocks were the only bright spot as safe haven buyers continue to flock to bullion and the AUD price taps on the door of $1700. The big golds naturally have led the rally with Newcrest (NCM) +8.25%,OceanaGold Corp (OGC) +11.53% and Evolution Mining (EVN) +6.41%. Even Kingsgate (KCN) +16% rallied hard albeit from a very low base.

- Resources joined in the rout though with some of the recent rallies starting to unravel. BHP -1.95%, RIO -1.25% and Fortescue Mining (FMG) -1.64%. Other resources held up better than the general market and the banks in particular, South32 (S32) -4.22% though gave back some of its recent gains.

- Energy stocks were once again sold down aggressively, Santos (STO) -4.97%, Woodside (WPL) -2.48% and Origin Energy (ORG) -3.78%. AWE -7.14% one of the worst stocks in the sector followed by Whitehaven Coal (WHC) -5.95%.

- Financials were a tough game today. Banks were mauled with Westpac (WBC) -5.16%, Bank of Queensland (BOQ) -8.12% and Bendigo and Adelaide (BEN) -5.54% suffering in the regionals. Wealth managers were also aggressively sold down led by Henderson Group (HGG) -5.89%, BT Investment (BTT) -6.26% and Magellan Financial (MFG) -4.3%. Insurers were hurt with AMP -4.53% the most badly affected. Challenger (CGF) -6.37%.

- Industrials were understandably weaker with defensive healthcare stocks unable to drag any buyers off the sidelines. Ramsay Health (RHC) -2.99%, Sonic Healthcare (SHL) -4.58%, Capitol Health (CAJ) -12.9% and Primary Healthcare (PRY) -1.68%.

- Telcos and IT were in the bears’ sights with Technology One (TNE) -6.47%, Computershare (CPU) -2.25% Aconex Limited (ACX) -6.01% and Carsales.com.au (CAR) -1.77%.

- Consumer stocks fell except for Nick Scali (NCK) +6.8% on results and Godfrey’s (GFY) +15.05%

- Speculative stock of the day: Wingara (WNR) +150.0% following a reverse back door listing and name change from Biron Apparel. As part of the relisting it raised $4.8m and pushed into the agricultural business with land purchases to come..

Corporate News

- Telstra (TLS) -1.06% suffered consumer backlash following a mobile outage in capital cities.

- Newcrest (NCM) +8.25% reported a geotechnical event today at its Kencana underground mine at the Gosowong project in Indonesia. One worker has been trapped 300m underground.

- Nick Scali (NCK) +6.8% continues to ride the housing boom as it expects profits to rise 40% in 2016 with same store sales up 11.6% in the six months to December.

- Bank of Queensland (BOQ) -8.12% announced they it would be investing $15m in a restructuring operation that should recover costs within 12 months, but more importantly it again stated that margins were under pressure due to cost increases. Unlike the big four the smaller banks do not have the pricing power of the near monopoly, with ANZ and recently NAB putting up their rates.

- Orocobre (ORE) +4.86% updated the market today on its Olaroz Lithium production facility. An increase in production in January of around 272 tonnes to 699 tonnes. De-bottlenecking program is completed and March quarter production forecast to be approximately 2,400 tonnes.

- Ferrovial is taking another look at Broadspectrum (BRS) -13.15% after saying that the recent delay in the detention contracts has reduced its value. The current bid is 135 cents and the Spanish suitor now has grounds to withdraw its bid if it wants according to the bid conditions.

Economic News

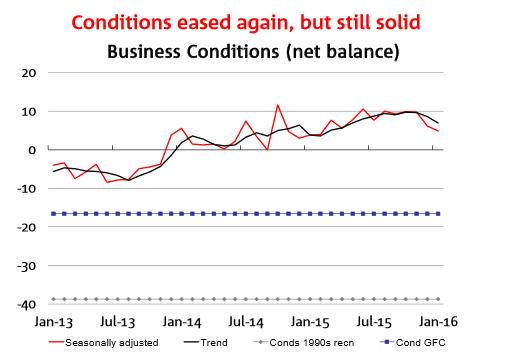

- Business confidence held steady as non-mining confidence remained healthy.

- Australian government bonds had a massive day, with the yield down 20 basis points to 2.40%. That’s not far away from the record low of 2.28% hit in February of 2015.

In Asia

- Japan had an absolute horror day falling over 5.4% or nearly 1000 points as bond yields collapsed with Ten years turning negative. Since the now tragic NIRP (Negative Interest Rate Policy) was announced the Japanese banks have fallen 25% and 32% since the start of the year.

Europe and US

- Remember Greece? Seems to have been off the radar as the country passes its refugees onto Germany but the equity market in Athens is once again showing extreme signs of strain. The banks in Greece (an oxymoron if ever there was one) were down to their lowest level in 25 years. The shares of the National Bank of Greece fell 28.6%

- 21st Century Fox expects little growth in earnings this financial year as disappointing performances in its film business and an expected negative currency impact of $US350 million ($494.4 million) for the year are expected to hit earnings.

- Deutsche Bank has been forced, in an extraordinary move reminiscent of the GFC, to issue a statement defending its liquidity.

This may go some way to calm the markets in Europe tonight. They will need to.

And finally Nathan Tinkler has been declared bankrupt with an appeal set from his lawyers. A sign of the times?

Ahead in Europe

- FTSE -25.50 point.

- DAX -294 points.

- CAC -134 point.

MARKET STATS

- Volume was $6.80bn (Daily average $4.656bn FYTD)

- Dow Jones Futures down 121 points.

- Dow Jones was down 178 points overnight.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com