Tags

abbott, anz, asx, Asx 200, ASX200, aussie dollar, australia, Australian Sharemarket, bank of england, banks, ben, Ben Bernanke, Bernanke, BHP, BHP Billiton Limited, billabong, boe, BOJ, BRU, cba, Charlie aitken, china, commonwealth bank, Commonwealth Bank of Australia, copper, crash, cyprus, diggers and dealers, dollar, dow, draghi, ECB, economy, essex Lion, eu, euro, europe, eurozone, fairfax, fed, finance, fmg, fomc, Fortescue, Fortescue Metals Group Ltd, Fortescue mining, france, gold, greece, igr, insurance, Interest Rates, iron ore, iron ore falls, italy, Japan, Macquarie Group Limited, Mario Draghi, marmota, meu, Mo farrah, NAB, National Australia Bank Limited, National Bank, nev power, Newcrest Mining Limited, oroton.qbe, RasPutin, RBA, Reserve Bank, results preview, RIO, Russia, SGP, shares, silver, Sirius Resources, slr, stevens, stock, stocks, super mario, telstra, Telstra Corporation Limited, ten, tinkler, TLS, twiggy, uk, Ukraine, wbc, WHC, Whitehaven Tinkler coal bid cash, Woodside Petroleum Limited, woolworths, wow, yellen, zombieland

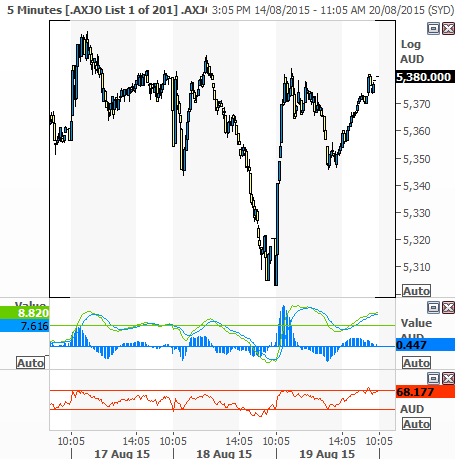

ASX 200 up 77.1 at 5380.2.Banks bounce. Woodside cheers and Penfolds kills it. Seek gets lost and China continues to shed. Dow futures down 60.

Yesterday never happened

- What a difference a day makes. After yesterday’s rout, especially in the financials, some sanity returned with broad based gains led by Westpac (WBC) +3.32%, National Australia Bank (NAB) +2.58% and Australia and New Zealand bank (ANZ) +3.0%, although Commonwealth Bank (CBA) +1.77% underperformed. The banks accounted for around 40% of the rise today.

- REITS performed very strongly following Stockland (SGP) +0.48% results. In other industrials, results dominated with another big day but the relief rally spread to consumer stocks like Wesfarmers (WES) +1.82% and Woolworths (WOW) +1.79%.

- Telstra (TLS) +1.47% led the Telcos higher as Spark New Zealand (SPK) +4.56% powered ahead. In other tech companies Computershare (CPU) +2.21% have started to claw back losses, whilst mid-caps in the space also doing well, Freelancer (FLN) +2.14% and iProperty (IPP) +1.01%.

- In resource land, iron ore miners were solid as BHP +0.72%, RIO +0.12% rallied but top performer Fortescue Mining (FMG) -2.02% after a huge run yesterday on asset sale talk. Energy stocks took their cue from Woodside Petroleum (WPL) +2.53% following the better than expected figures. However it may be short lived as the oil glut continues. Santos (STO) +3.42% results tomorrow will be really interesting given the market rumours of a capital raising. Origin Energy (ORG) +5.32% was the stand out in the sector but Whitehaven Coal (WHC) +12.67% continued its Phoenix like revival after the results the other day, this is despite coal being at a 12 year low around USD52.85 a tonne below its peak following the 2011 Fukishima nuclear disaster. In other resource stocks, both Sirius (SIR) +1.56% and Independence Group (IGO) +1.29% had better days, as did Sims Metals (SGM) +2.05% and Alumina (AWC) +3.09% on better results showing it returned to profit of USD122m. Cost cutting of $20 a tonne combined with higher prices of around $321 a tonne also helped.

- Retailers continued to surprise after the dismal performance of Dick Smith (DSH) +0.0% yesterday with The Reject Shop (TRS) +16.35% proving that not all retailers are the same.

- In tech stocks SEEK (SEK) -10.96% also announced its results today with a disappointing set of numbers. The profit lift of 6% to $189.9m was not enough with the PE of 25 proving hard to maintain given guidance for only a 5% increase next year. Hardly the stuff that growth stocks are made of. The SEEK learning business is still a problem child with earnings dropping 8% whilst international growth at 34% is encouraging. Consider that bank shares are trading on PEs around 12/13 and have 5% growth and its easy to see why SEK is sliding. The company sees material margin compression given its new product investments and cost of customer acquisition in international markets. SEEK will pay a final dividend of 17c per share, up from 16c last year, which will be payable on October 16.

- Pokey stocks came up all cherries following Ainsworth Game Technology (AGI) +14.23% showing net profit of $70.4m driven by a 46% increase in overseas earnings. Aristocrat (ALL) +1.06% joined in the fun and forecast now look a little conservative. In casino stocks Crown Resorts (CWN) -1.05% and Echo (EGP) -1.92% eased after Macau heavy weight Galaxy Entertainment earnings plunged 46%.

- Biotech stocks were a little under the weather today as CSL -0.39% slipped, along with Mesoblast (MSB) -2.79% and Sirtex (SRX) -2.58% finally! A better day though for radiology and pathology stocks Ramsey Healthcare (RHC) +1.03%, Sonic (SHL) +4.09% and Primary Healthcare (PRY) -0.94%.

- In economic news the Westpac-MI Leading indicator is losing momentum as economic activity is set to fall. This lacklustre performance may start to derail the forecast for a better 2016 for the economy.

Turning to results in more detail.

- Woodside (WPL) +2.53% announced results today and beat expectation slightly. A 39% drop in first half profits to USD679m was dragged down by a 9.7% reduction in production whilst the dividend was US66c. Importantly the production guidance for next year was unchanged at 86-94 m barrels of oil equivalent which soothed some nerves with talk of more cost cutting at the Browse floating LNG venture also helped as management continue to focus on the cost out story.

- The Reject Shop (TRS) +16.35% silenced the critics with a strong rebound in same-store sales and earnings in the second half of 2015 and positive guidance for more to come in 2016. After a 24% fall in net profit in the December half to $12.8m, full year net profit slipped 1.9% to $14.2m, beating market forecasts as the company returned to profit in the June half.

- Stockland (SGP) +0.48% has lifted underlying profit 9.4% to deliver $608m for the year to June 30. This was boosted by the housing boom and improving retail markets for shopping centres.

- In a great result from Treasury Wine Estates (TWE) +13.43%, the market raised its glass to the huge jump in Asian profits, up 53%, to $73.1m for the year. Margins were also very positive at 36% as the transformation continues. A big focus on the brand development and rationalisation of corporate costs especially Melbourne. The secret it seems to its success is tighter on-ground management and building relationships with retailers rather than running it long distance from Melbourne. The new CEO Michael Clarke thinks Asian profits will be the biggest earner in 18 months far surpassing the local and US markets.

- Meanwhile in Asia, we are seeing multi year lows as the MSCI’s emerging market index fell to its lowest level since October 2011. It has dropped more than 20% from the year’s peak it hit in April. China once again was a problem child as gamblers worried that the authorities had finished their market support. The 200 day MA has been rumoured to be the line in the sand. Let’s hope it is not the Maginot Line.

- Our market avoided the afternoon sell off and closed near its highs. However Shanghai was down 2.88% and Tokyo down 1.3%. It seems that rich sophisticated investors are selling China and letting the mums and dads hold the baby. The outflows from emerging markets is now over $1 trillion in the last 13 months and could accelerate as we run into a Fed rate rise.

- European markets look set to open down a little with FTSE down 15 points, DAX 38 points and CAC down 15. Greece is edging towards a debt deal with news that the Germans had bought all the Greek airports for a measly €1.23bn. One of the conditions of the bailout conditions.

- And spare a thought for Malaysian markets where the PM is having his bank accounts probed. The currency has lost 5.6%, the stock exchange is down 8.3% and sovereign bonds are at 4 year highs since the PM was accused of back pocketing US$637m. Even Vietnam devalued its dong for the third time this year. The fallout from the yuan devaluation and the impending US rate rise continues for emerging markets.

Clarence

XXX