Tags

abbott, anz, asx, Asx 200, ASX200, aussie dollar, australia, Australian Sharemarket, bank of england, banks, ben, Ben Bernanke, Bernanke, BHP, BHP Billiton Limited, billabong, boe, BOJ, BRU, cba, Charlie aitken, china, commonwealth bank, Commonwealth Bank of Australia, copper, CPU, crash, cyprus, diggers and dealers, dollar, dow, draghi, ECB, economy, essex Lion, eu, euro, europe, eurozone, fairfax, fed, finance, fmg, fomc, Fortescue, Fortescue Metals Group Ltd, Fortescue mining, france, greece, igr, insurance, Interest Rates, iron ore, iron ore falls, italy, Japan, Macquarie Group Limited, Mario Draghi, marmota, meu, Mo farrah, NAB, National Australia Bank Limited, National Bank, nev power, Newcrest Mining Limited, oroton.qbe, qbe, RasPutin, RBA, Reserve Bank, results preview, RIO, Russia, SGP, shares, silver, Sirius Resources, slr, stevens, stock, stocks, super mario, telstra, Telstra Corporation Limited, ten, tinkler, TLS, twiggy, uk, Ukraine, wbc, WHC, Whitehaven Tinkler coal bid cash, Woodside Petroleum Limited, woolworths, wow, yellen, zombieland

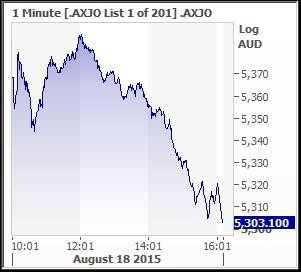

ASX 200 down 64.6 points to 5303.1 after a positive start. Gains evaporated as banks tanked. RBA turns positive. Market turned negative after lunch. 83 point range today. Dividends dominate with results flooding in. US futures down 32.

ASX200 Today

Someone had a bad lunch!!!

- A day of dividends and disappointment with results and RBA minutes dominating. A huge day today for company announcements with QBE +0.36% not disappointing for a change, a bid for Asciano (AIO) +7.15% from Canada’s Brookfield Infrastructure and Channel Nine (NEC) +2.17% selling its Willoughby site. However, all eyes were once again on the smashed banking sector as Commonwealth Bank (CBA) -5.36% traded ex-dividend and just kept falling all day, together with the trading update from ANZ -1.86%. Despite the banks starting on a positive note, gains evaporated as the day wore on. The big four were slammed, they accounted for 40 points of the 65 point fall. In other financials, Insurers slipped as did REITS. Not a good day and slightly worrying. Smacks of an overseas player selling.

- Resources remain the ugly sister of the industrials with energy being the ugliest of all. Seven year lows in the oil price are taking a toll on the sector and Santos (STO) -2.34% continues to suffer despite denying it needs to raise funds. Market darling Liquefied Natural Gas (LNG) – 5.43% has been hardest hit together with local small gas plays like Drillsearch (DLS) -5.13% and Buru (BRU) -2.5%. However iron ore plays were less affected with Fortescue Mining (FMG) +7.88% responding to media speculation that it was considering asset sales. It said it was open to talks but no agreement had been reached. There seems to be a chasm between the price it wants for assets and the price Chinese buyers are prepared to pay.

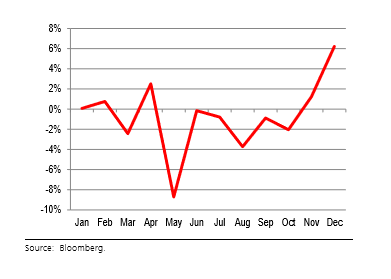

Interesting to see how iron ore prices tend to rise in the 3rd and 4th quarter

- Other base metal resource stocks fared particularly badly with Independence Group (IGO) -4.91% and Sirius (SIR) -4.46% in real trouble. Seems that the market reassessed the Newcrest (NCM) -5.07% result from yesterday with the stock offering nothing for the bulls.

- Industrials were weaker across the board but there were some bright spots despite the falls. Telstra (TLS) +0.49% bucked the trend as did Qantas (QAN) +0.8% after its deal with Sydney Airports (SYD) +1.23 % and Asciano (AIO) +7.15% helped the infrastructure stocks such as Aurizon (AZJ) -0.38%.

- RBA minutes out today and slightly more positive than normal. It is counting on a regulatory crackdown on bank lending to buy-to-let and buy-to-sell investors to put a lid on runaway property price inflation in Sydney and Melbourne, and head off any future distress for the country’s lenders. It said there was considerable uncertainty on unemployment and the sluggish non-mining sector but overall the tone was upbeat and suggests that interest rates are on hold for some time to come.

- Challenger Limited (CGF) +2.46% has posted an 18% rise in assets under management to $60bn for the year to June and double digit growth in its earnings. Challenger reported a 13% rise in normalised EBIT of $438m. It recorded a normalised net profit of $334m for the year to June – up 2% from 2015. The group’s statutory net profit hit $299m.

- Sonic Healthcare (SHL) -1.74% reported a 5.6% slump in full-year profit to $363.3m. The weaker profit came despite a 7.3% rise in revenue for the year ended 30 June to $4.2bn.

- Monadelphous (MND) + 0.97% suffered a slide in profits to $105.8m from $146.5m but remains upbeat on the future and concentrating on cost cutting with a focus on growth in maintenance and services for the oil and gas sector.

- Sydney Airports (SYD) -1.23% announced a deal with Qantas this morning giving it control of Terminal #3 retail operations and move domestic and international operations there over the longer term. It has paid Qantas $535m for the lease coupled with announcing a 6.4% rise in half year EBITDA and importantly raised its guidance.

- The second largest corporate deal was announced this morning with Canada’s Brookfield Infrastructure bidding around $12bn for Asciano (AIO) +7.15%. This follows hot on the heels of Japan Post’s deal to buy Toll Holdings, who used to own Asciano. It is the biggest takeover in the sector ever and is proving that the lower AUD is attracting overseas buyers to unique and undervalued infrastructure assets. The deal valued at a 40% premium to the pre bid share price has been recommended by the board. Results today of a net profit of $359.6m up from $254.4m. No final dividend but a special of 90c instead. It still needs some approvals so there is a way to go. Xmas perhaps?

- Dick Smith (DSH) closed -16.5% had a shocker day after announcing results that were a little disappointing. NZ especially so. Although online sales have doubled and total sales were up 7.5% to $1.3bn, EPS was only 6c against estimates of around 8c. The stock was punished accordingly but looks to have been overdone by the momentum traders.

- QBE Insurance Group (QBE) +2.46% has increased its dividend payout ratio in 2016, after reporting first-half net profit rose 24% to $661m. It currently pays up to 50% of annual cash profits in dividends to investors, but this will ratchet up to 65% in 2016. Investors will be paid a 20c dividend for the six months ended June 30, up from 15c in 2015. QBE continued off loading under-performing or loss making assets and looks to be turning the corner. The stock has been a huge outperformer this year, up around 30%.

- Australia and New Zealand Bank (ANZ) -1.86% announced a $5.58bn for the period up from $5.18bn. Impairment charges decreased by 3% whilst its provision charge increased by 13% to $877m. CEO Mike ‘007’ Smith has tried to calm investors saying that the bank’s loan book is in good shape. Not that it helped the share price today.

- General Property Trust (GPT) -0.86% results jumped 75% to $421.9 with EPS growth of 6.7%.

- InvoCare (IVO) -6.40%. Australia’s largest funeral home operator is doing well at home, however its recent foray into California is proving harder to bed down. They bought a San Diego crematorium for US$2m and have conducted 100 funerals since the takeover. However the US business incurred an US$1.5m loss and said that the loss could double as it tries to increase brand recognition. When the losses from InvoCare USA and the impact of acquisitions were included, InvoCare’s net profit after tax for the six months ended June 30, 2015 was 11.3% lower at $18.5m.

- Meanwhile in Asia, Shanghai has lost 3.07% while Japan was off 0.32%. Nothing terribly bad. Certainly no reason for our market to throw in the towel. Numbers out from China on new house sales were positive which may have helped the bear case for limited stimulus and intervention.

- In China, new home prices rose in 31 cities of the 70 the government monitors, from 27 the previous month. They dropped in 29 and were unchanged in 10. The average price has now risen for the last three months with the average price of the 70 cities rising 0.17% from June.

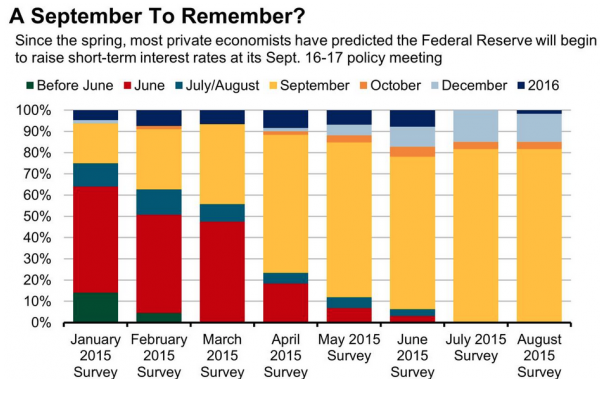

- And finally the odds for a September rate rise from the US have firmed considerably and as we head into the second half of reporting season, the Fed decision will soon become the main focus.

Clarence

XXXX