ASX 200 closes up 7 points at 7393 (0.1%) in another tight-range day. Tiny late surge. Seems BoJ was not a catalyst after all. The song remains the same from the central bank. Good times and bad times from resources as Chinese authorities once again shake a waggly stick on iron ore prices. BHP down slightly, FMG up 0.8%, RIO up 1.1% and MIN up 0.3%. Lithium stocks remain dazed and confused. PLS down 1.5%, IGO off 2.8%. Not a whole lotta love for gold miners today either, as NCM fell 1.8% and NST off 1.7%. Coal stocks had a celebration day, with WHC up 2.9% and NHC better by 3.0%. Healthcare stocks were on a stairway to heaven as CSL rose 0.8%, RMD bucked up 2.3% on broker upgrades, with FPH also doing well. Industrials mixed as REITS fell a little, old skool stocks rambled on, REA up 0.1% and SEK better by 1.0% with bond proxies trampled under foot, TCL off 0.5% and ALX off 2.0%. Banks becalmed with the Big Bank Basket unchanged at $187.93. In corporate news, RBL fell 11.4% as the bubble burst, TLX did well on revenue numbers, and a good outlook, NIC in a trading halt as it said thank you with a big new capital raise and AKE underwhelmed a little on their quarterly update. On the economic front, we had building approvals down as the House of the Holy commitments fell 5.2%. In Asian markets readying for Lunar New Year, China up 0.1%, HK unchanged% but Japan leaping on a lower yen up 1.7%. 10-year yields 3.56%. Dow futures are down 5 points. Nasdaq futures up 14 points.

HEADLINES

- Winners: CDA, SYA, TLX, CTT, PNV, JRV, 360

- Losers: HUB, GOR, AGG, RED, ACL, SBM, CMM

- Positive sectors: Healthcare. Coal. Tech. Staples.

- Negative sectors: REITs. Lithium. Gold miners.

- High 7411 Low 7376 Narrow range waiting for anything!

- Big Bank Basket: Closed unchanged at $187.93

- All-Tech index: Up 1.4%

- Gold eases to $2715

- Bitcoin: Off highs at US$21269

- Aussie Dollar: Off highs to 69.79c

- 10-Year Yield: Steady at 3.56%

- Asian markets: Readying for Lunar New Year, China down 0.1%, HK unchanged, but Japan leaping on a lower yen up 1.7%.

- US Futures: Dow down 5 Nasdaq up 14

MAJOR MOVERS

- TLX +8.60% positive revenue update.

- SYA +8.89% finding support.

- AQZ +3.86% ACCC decision looms.

- PNV +4.96% back on buyers list.

- DRO +26.42% kicking higher.

- VHT +12.06% positive update.

- CYM +6.67% copper play still in demand.

- RED –4.00% gold stocks falling away.

- GOR –4.56% more yellow brick.

- KAR –3.13% broker downgrades.

- SBM –3.45% gold sell off.

- RBL –11.40% bursts on job cuts.

- BOC –7.35% tiny volume.

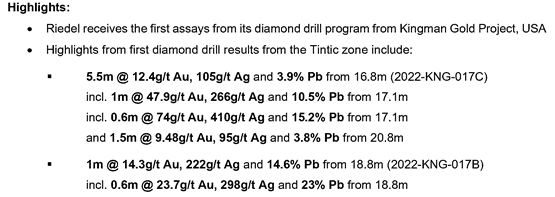

- Speculative Stock of the Day: Not many candidates. Riedel (RIE) +37.5%

- Above Average Volume: RIE, WAT, LGI, EQE, KIN, SGC

COMPANY NEWS

- Ampol (ALD) Announced the Lytton Refiner Margin for Q4 remained above historical averages at US$11.75 per barrel. Q4 EBIT is expected to be slightly higher than Q3 results with all areas of the business performing well.

- Telix Pharmaceuticals (TLX) reports revenue from the sale of Illuccix has increased 43% in the quarter compared to the pcp. Revenues for the company as a whole have increased 41% to $78.2m

- Nickel industries (NIC)reports record nickel production of 23,072 tonnes in the December quarter. They have also reported the death of two employees in the same period. In a trading halt as it is raising $264m in a placement at 102c as part of a larger capital ($673m) raising for an acquisition and strategic alliance with Chinese nickel and HPAL companies. SPP to raise $20m to come. Part of the conditional placement was to Newstride Development Limited, $US15m to Wanlu Investment Co and $US1.4m to Nickel Industries’s non-executive director Mark Lochtenberg

- Allkem (AKE) reports a record lithium production at the Olaroz Lithium Facility, which increase 17% from the previous quarter. AKE also had record quarterly revenue of US151m from the increased production. Mt Cattlin a little underwhelming.

ECONOMIC & OTHER NEWS

- China’s state planner on Wednesday issued its third warning this month against excessive speculation in iron ore, adding it will increase supervision of the country’s spot and futures markets.

Australian Building Approvals – Key Statistics

In seasonally adjusted terms:

- Total dwelling commencements fell 5.2% to 45,489 dwellings.

- New private sector house commencements fell 4.9% to 28,895 dwellings.

- New private sector other residential commencements fell 5.2% to 15,618 dwellings.

- The value of building work done rose 1.5% to $30.6b.

- UBS has upgraded its ASX outlook as the global outlook looks better than anticipated. He now forecasts year-end target for the ASX200 index to 7500, from 7250.

- Sam Bankman-Fried reiterated his view that the FTX US crypto exchange “was and is solvent.” And Santa Claus is real.

ASIAN MARKETS

- BoJ leaves short-term interest rates (-0.1%) and YCC policy unchanged as expected. BoJ keeps the YCC target for the 10-year yields in place with the vote unanimous. The broader policy guidance maintained its commitment to QQE and YCC with the aim to achieve a 2% inflation target. The statement expressed an easing bias that the BoJ will not hesitate to take additional easing measures if required and rates are seen tracking at current or lower levels. Reiterated inflation is expected to cool toward mid-FY23.

- “Japan’s economy is projected to continue growing at a pace above its potential growth rate,” the central bank said in a statement.

- Japan’s Tankan Sentiment Index for manufacturers fell to -6 in January 2023, turning negative for the first time in two years, reflecting a slow recovery following the pandemic amid ongoing inflation and economic uncertainties.

US AND EUROPEAN HEADLINES

- IMF signals upgrade to forecasts as optimism spreads at Davos.

- Musk’s Tesla ‘funding secured’ trial to begin after jury selected.

- ECB policymakers are reportedly considering a slower pace of rate rises, while a 50-bps increase in February remains likely, a smaller 0.25% lift in March is gaining support, Bloomberg reported.

- Microsoft to announce job cuts today.

Clarence

XXXX

IT issues …jokes will be back…send me some new material….henry@marcustoday.com.au